China’s record-breaking trade surplus of nearly $1.2 trillion last year has been a recurring theme in global economic discourse, and the trend is continuing this year, despite persistent headwinds to cross-border trade. At the same time, its latest Five-Year Plan placed further emphasis on technological innovation, industrial upgrading and strengthening its trading position, all of which is expected to further enhance its role in global supply chains. Understanding how China generates and sustains this trade performance is therefore of global significance.

Yet, discussions about China’s trade footprint often treat the country as if it were a single economic unit, overlooking the regional differences within a country comparable in size to the USA, with a workforce of over 800 million people, and vastly different industrial strengths across its geography.

A provincial perspective reveals a more nuanced picture: one of highly specialized regional economies that collectively power China’s position in global trade.

China’s trade landscape is far from uniform. In fact, 96% of the country’s nearly $1.2 trillion trade surplus last year originated from just four provinces: Zhejiang, Guangdong, Jiangsu and Shandong.

Located respectively at the mouths of the Qiantang, Pearl, Yangtze and Yellow rivers along China’s coastal economic corridors, these provinces have long served as gateways connecting China’s manufacturing base with international markets. China’s geography, and particularly the flows of its major rivers, has shaped its trade flows and economic landscape.

Meanwhile, neighbouring Zhejiang, named for the bends of the Qiantang river, has emerged as a centre for cross-border e-commerce and small-parcel exports, supported by manufacturing hubs like Yiwu, famous as the main source of Christmas goods. As cross-border e-commerce continues to grow, platform-driven trade has become an important component of China’s international commerce. Zhejiang’s prominence reflects the growing role of digital platforms in connecting Chinese producers with consumers worldwide.

Further North, Shandong’s export profile spans both industrial and agricultural products, accounting for more than half of China’s tyre exports, while also serving as the country’s largest exporter of vegetables. This combination of manufacturing and agricultural exports demonstrates the breadth of China’s export ecosystem beyond the technology sector.

While China’s trade surplus is concentrated in a handful of coastal provinces, the broader trade landscape is far more diverse. Eight of Mainland China’s 31 province-level divisions recorded trade deficits in 2025, reflecting their roles as centres for imports, finance, logistics and resource allocation rather than export production.

At the same time, a growing number of China’s regions are becoming increasingly important participants in global trade. In 2025, 15 provinces recorded total trade values exceeding $100 billion.

Liaoning and Anhui illustrate two different pathways through which provinces are integrating into global trade. First, anchored by the port city of Dalian, Liaoning serves as an important gateway connecting China with Northeast Asia, with strong exports of ships and marine equipment alongside imports of energy products.

Meanwhile, Anhui provides another example of China’s evolving trade landscape. Anhui, in particular its capital Hefei, has emerged as a key centre for the industries underpinning China’s industrial upgrading, particularly the country’s “New Three” products: electric vehicles, lithium-ion batteries and solar photovoltaic products. Anhui is also China’s second-largest exporter of passenger vehicles, supported by a rapidly expanding automotive cluster.

Taken together, these trade patterns shape the local communities around China, leading to differing demands for imported goods and services. Not every province has the perfect mix of talent, raw materials and connected infrastructure to become a world-leader in a new technology. Some provinces specialize in production and exports, others serve as centres for imports and processing of intermediate materials, while emerging hubs are helping anchor China’s continued efforts in industrial upgrading beyond its traditional coastal powerhouses.

These snapshot statistics of China’s regional trade picture reflect a broader transformation taking place across the economy. China has been steadily moving up the industrial value chain, progressing from manufacturing primarily labour-intensive goods towards increasingly technology- and innovation-driven production.

This transformation has been reinforced by close coordination between universities, research institutes, local governments and businesses, alongside targeted industrial policy tools and infrastructure investments, enabling these industries to scale rapidly. The scale is reflected in China’s growing investment in innovation: according to OECD estimates, China overtook the USA in gross domestic expenditure on research and development in 2024, underscoring the country’s increasing emphasis on technological advancement and industrial upgrading.

This is coordinated at the central government level: China’s latest Five-Year Plan continues to emphasize technological innovation, industrial upgrading and strategic emerging industries. Central coordination also seeks to reduce duplication across regions, focusing public resources where returns can be maximized.

Increasingly, China’s trade competitiveness is rooted not only in manufacturing capacity, but also in the strength of its innovation ecosystems, and its ability to commercialize new technologies at scale.

China’s economic story is increasingly shaped by two parallel trends. On the one hand, provincial ecosystems across the country are strengthening their positions in advanced manufacturing and technological innovation, helping drive record export performance. On the other, softer domestic demand and the ongoing adjustment in the property sector continue to weigh on broader economic activity, amid policy-makers’ efforts to boost domestic consumption and support a broader rebalancing of growth. Understanding China’s trade competitiveness therefore means not only looking at export performance, but also considering how industrial upgrading, external demand and domestic consumption interact to shape the country’s growth trajectory.

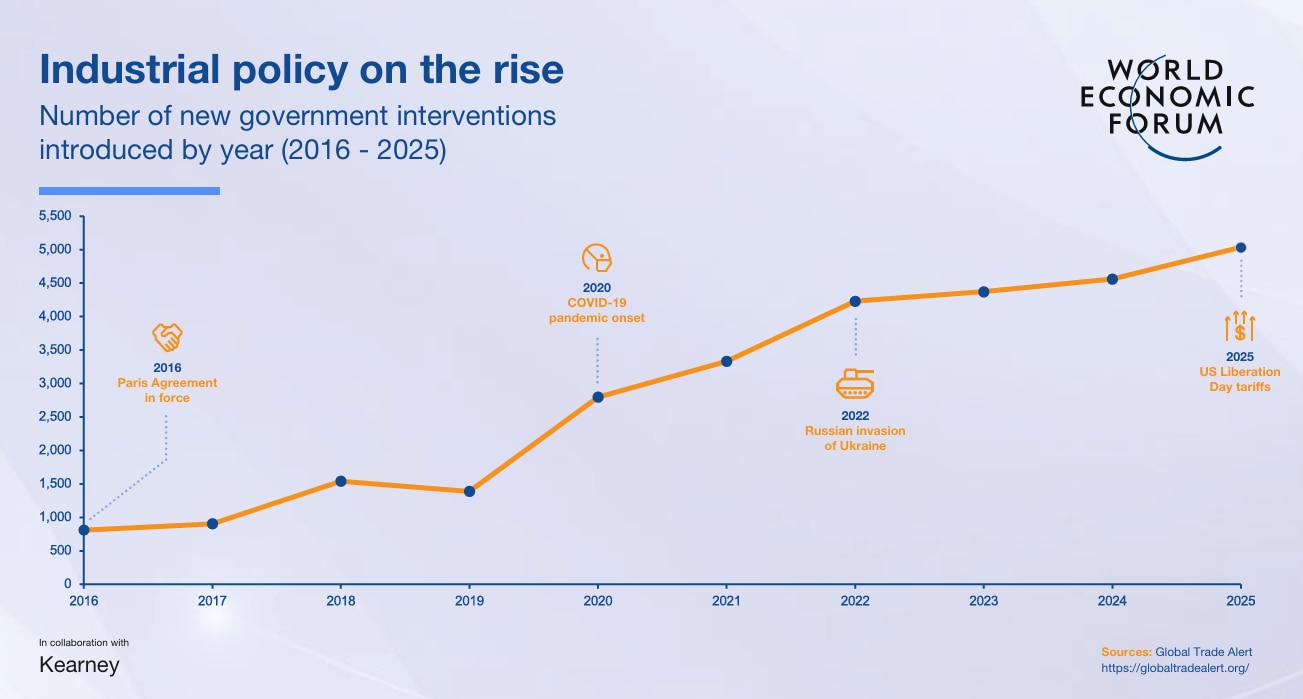

The result may not necessarily be less globalization, but a reconfiguration of it. Trade is increasingly being organized through regional blocs, mini-lateral arrangements and networks of trusted partners, creating a more complex and fragmented global trading landscape.

So, whilst China will undoubtedly continue to be a central actor in international trade in the coming years, it is important for international businesses and policy-makers to know the domestic makeup of its production and trade flows, to better understand and engage with its priorities.

As leaders gather in Dalian for the Annual Meeting of the New Champions 2026, understanding China’s provincial economies offers valuable insight into how global trade is evolving. Looking beyond national-level statistics reveals the regional specializations, industrial clusters and innovation ecosystems that continue to shape China’s role in the world economy, and increasingly, the future of global trade itself.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。