Klaus Vedfelt/DigitalVision via Getty Images

One Liberty Properties (OLP) appears dormant from the outside, but the transformation under the surface should lead to higher growth and valuation. After years of being a diversified REIT with a scattered portfolio, OLP has become a pure-play industrial REIT focused on highly fungible logistics warehouses. This article will discuss OLP’s new portfolio and valuation in the context of the industrial sector.

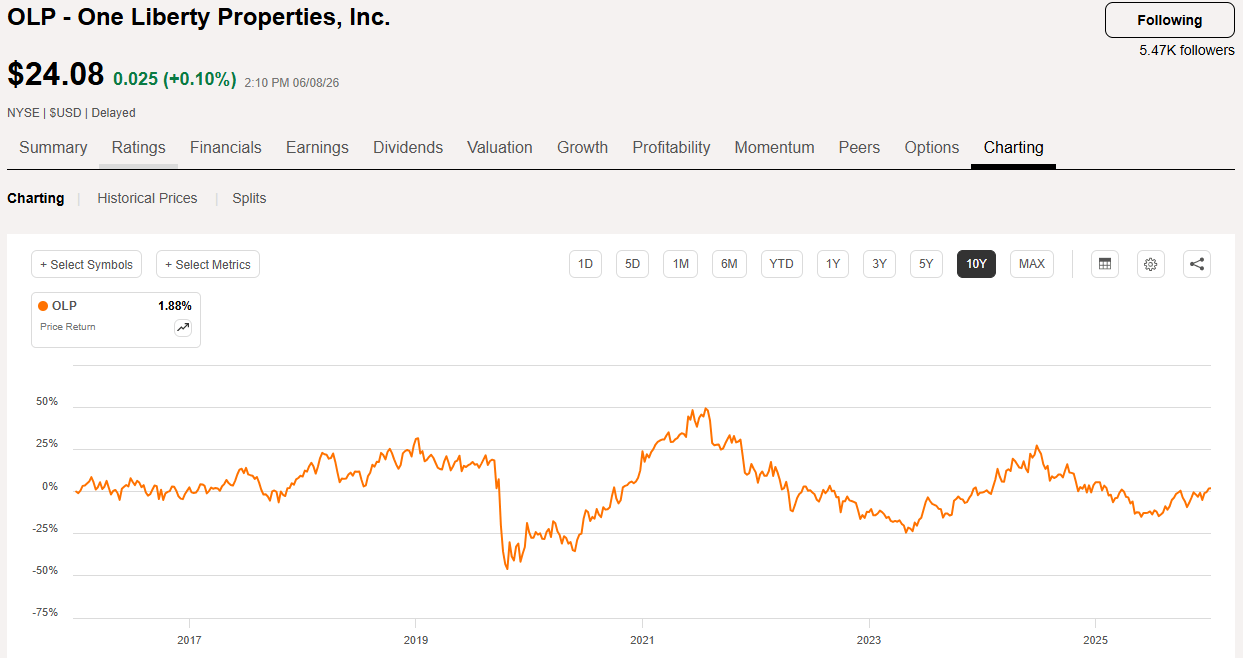

Price and earnings action give the impression that OLP has been inactive. It is trading at essentially the same price as 10 years ago.

OLP

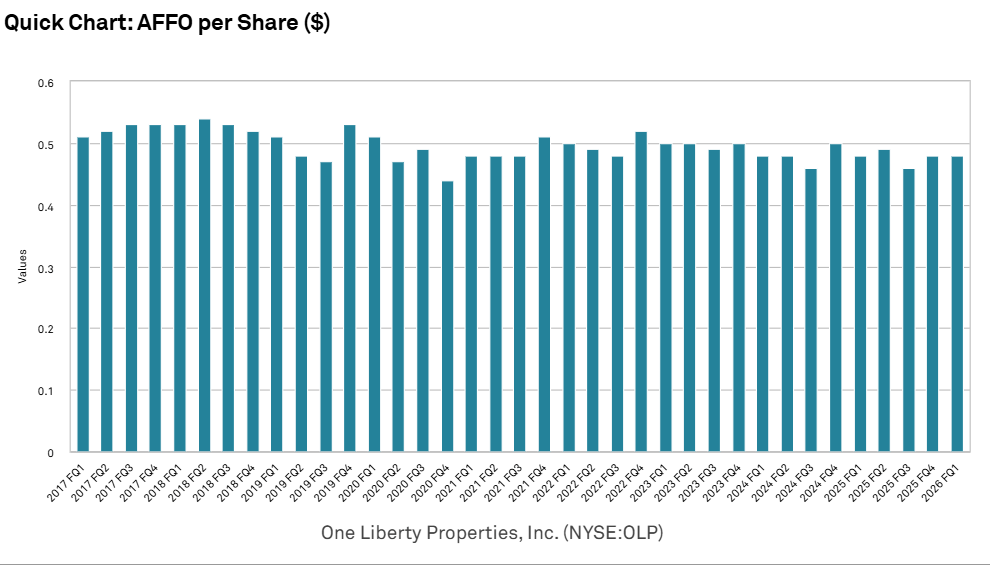

Its earnings (AFFO/share) are also flat for a decade.

S&P Global Market Intelligence

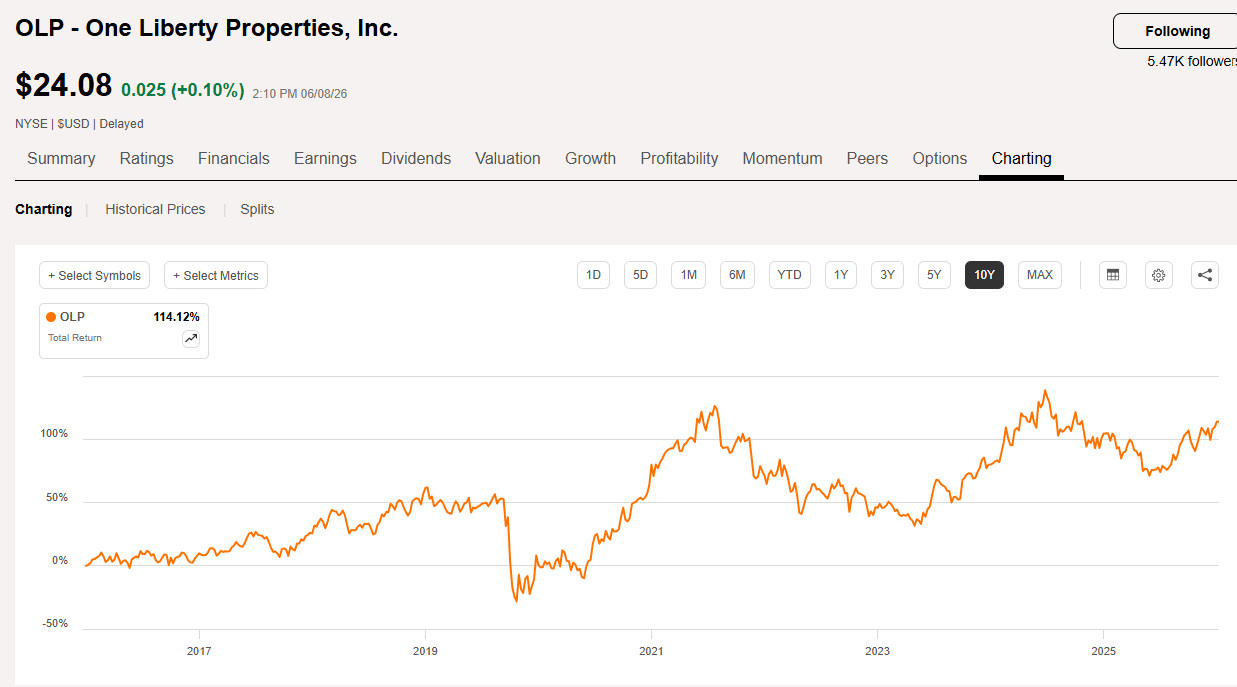

It has been an okay ride for shareholders as the very large dividend made the 10-year return 114%.

SA

So while it has done fine, a quick look at the company would make it seem as though they are simply paying out their profits as dividends and in a steady state.

Given that the company does not do public earnings calls and releases presentations less frequently than most, I think the market has not had the impetus to dig deeper. The price hasn’t moved, and earnings haven’t moved, so many might default to just thinking of it the same way they did 10 years ago.

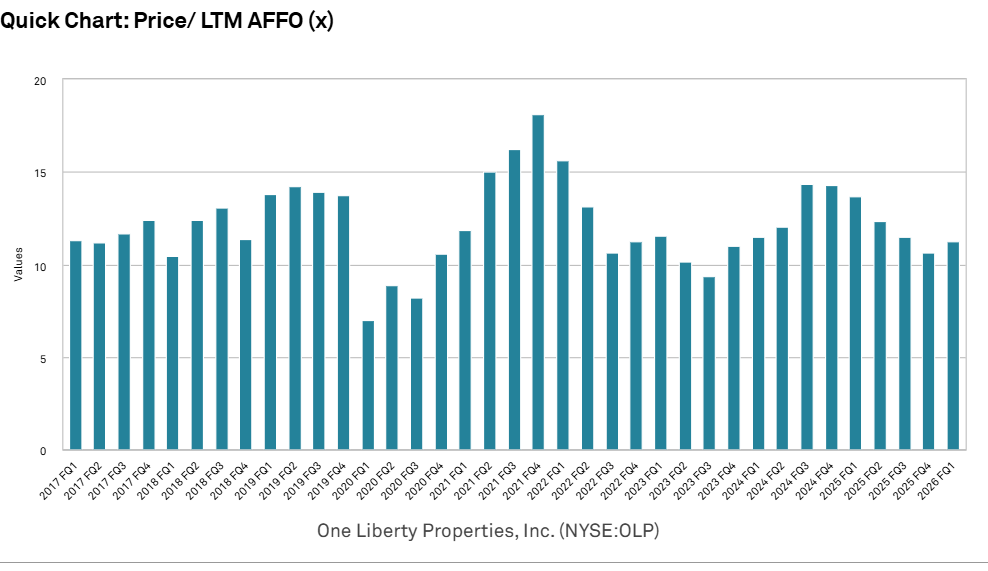

This is reflected in valuation with the AFFO multiple flat compared to 10 years ago.

S&P Global Market Intelligence

Multiples bumped up briefly in 2021 when the REIT market as a whole overheated in the zero-interest rate environment but swiftly returned to about 12X.

I believe this valuation is not properly accounting for the transition that happened under the surface. 12X AFFO was appropriate when OLP was a mashup of various property types, many of which were in need of substantial capex.

12X AFFO is too low of a multiple for a streamlined, logistics-focused industrial REIT with significant organic growth.

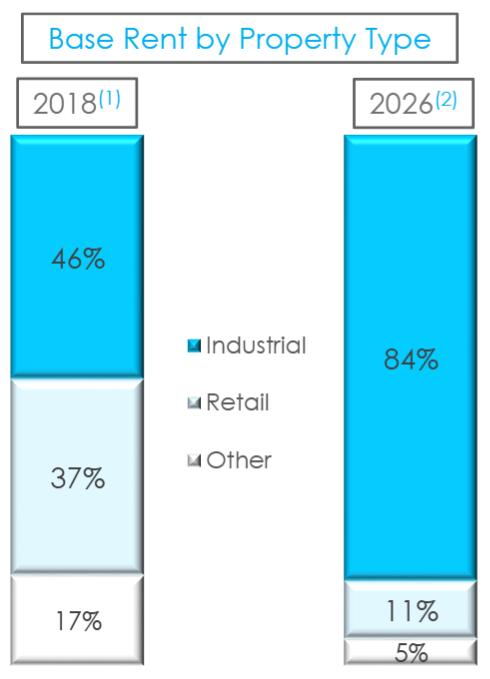

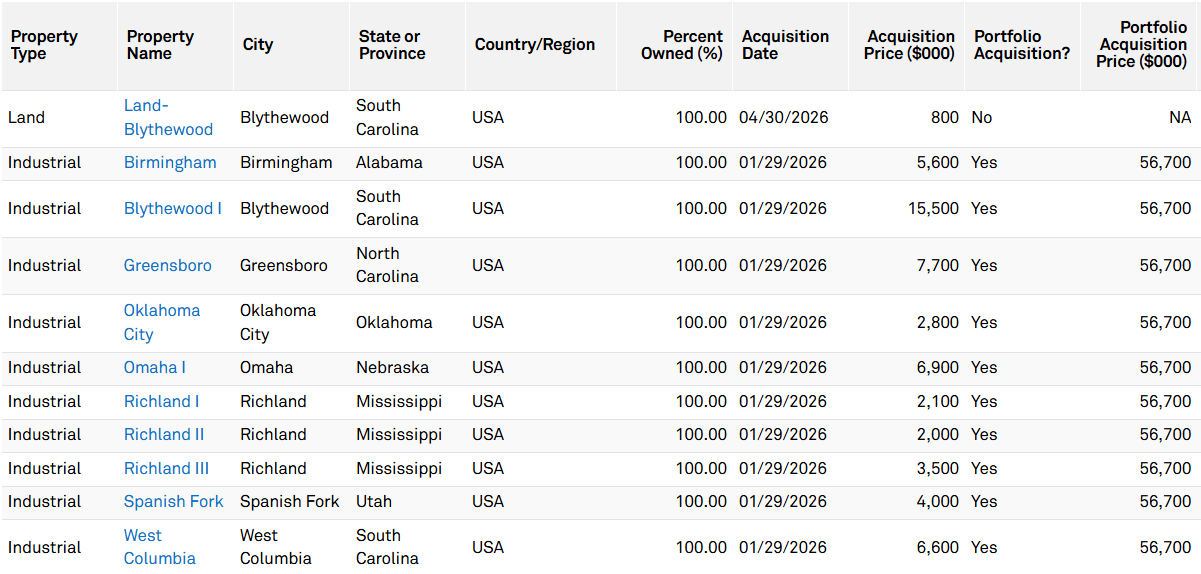

OLP was a mix of industrial, retail, and miscellaneous, but they have been selling off retail and other assets to buy almost exclusively industrial. As of 1Q26, the portfolio is 84% industrial and growing.

OLP

This is a transition we have seen many times in REITs. It is quite common for REITs to sell less favored property types and buy into the hot sector.

It is not by default a good thing to make such a transition. In selling the cold asset class to buy the hot asset class there is a substantially negative cap rate trade off.

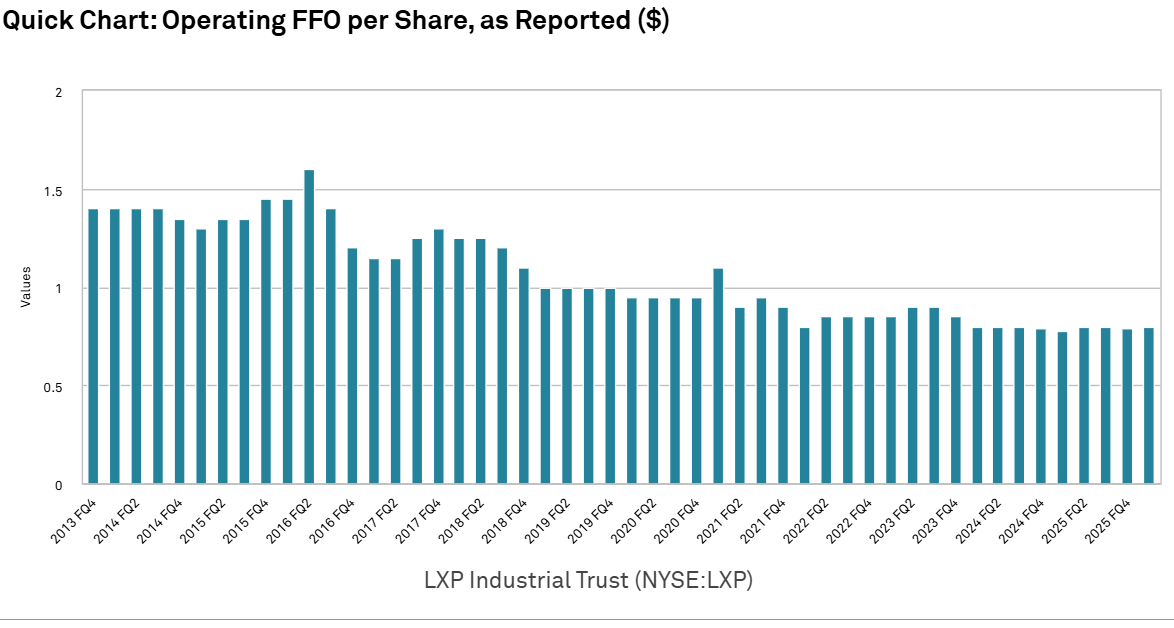

LXP sold its office at high cap rates around 8%+ and bought industrial at much lower cap rates. Thus, NOI was much lower, and it dragged earnings down. FFO/share plummeted throughout LXP’s transition.

S&P Global Market Intelligence

Mack Cali similarly lost substantial FFO/share as it transitioned to high-end apartments.

Execution matters quite a bit in making these changes. If a company rushes the transition or is sloppy in asset selection, earnings power gets hit hard.

Gladstone Commercial has largely managed to maintain FFO/share in its transition to industrial. They used 2 techniques to make the move less painful:

Since these asset class transitions can go very well or very poorly, we think it is worth scrutinizing the details of how OLP is executing the maneuver.

OLP is facing a similar negative cap rate spread that other companies have faced when changing asset classes. They are selling retail and other assets at medium to high cap rates.

High-quality industrial assets like the ones they are buying trade at lower cap rates. Thus, in each property trade, they are net losing current NOI. However, OLP is a long-tenured company, not focused on the next quarter. They are thinking more long-term about the overall IRR of assets.

The properties they are selling often have the following attributes:

In contrast, the assets they are buying have:

So while they are losing on immediate NOI, the overall IRR is arguably a favorable tradeoff.

To some extent, OLP is lucky in that retail is a hot asset class right now. Shopping centers are a key focal point of private equity, and I would argue that the buyers of OLP’s sales overpaid for lower-quality assets.

Due to the favorable sale environment for retail assets, the cap rate spread OLP is facing in its transition is nowhere near as painful as the spread suffered by LXP.

That is likely why OLP has been able to transition with minimal AFFO/share loss. The AFFO/share has also buoyed because the transition was over a number of years, which gave time for escalators on the industrial purchases to kick in.

Due to a mix of good execution and a favorable environment, OLP was able to get a substantial quality upgrade at minimal cost to AFFO/share.

Industrial is a broad asset class. It consists of both manufacturing and logistics which have distinctly different characteristics. I like both, but specific property attributes matter quite a bit.

OLP is buying almost exclusively logistics warehouses with an emphasis on fungibility. They have been rejecting specialized properties that are only useful to specific users and instead going for properties with attributes that make them broadly useful for general logistics use.

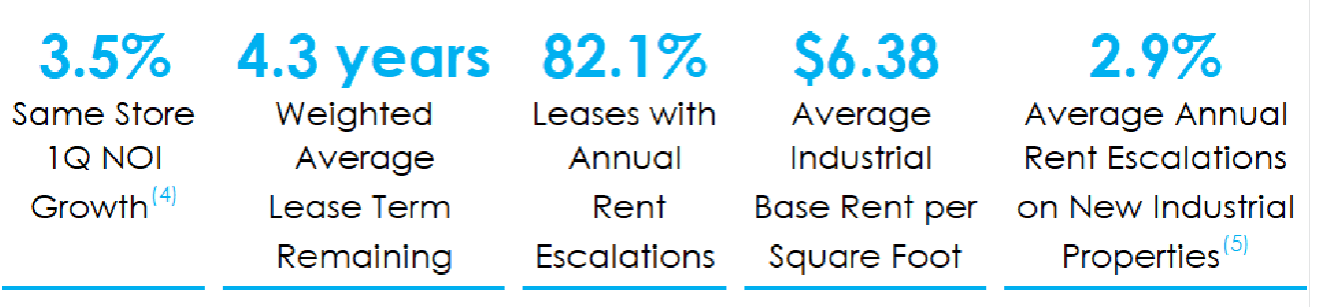

This sets them up well for re-leasing to the same or a new tenant when lease terms end. I suspect new lease rent spreads will be around +10% - +15%.

The properties have high escalators averaging 2.9% and fairly short remaining lease terms.

OLP

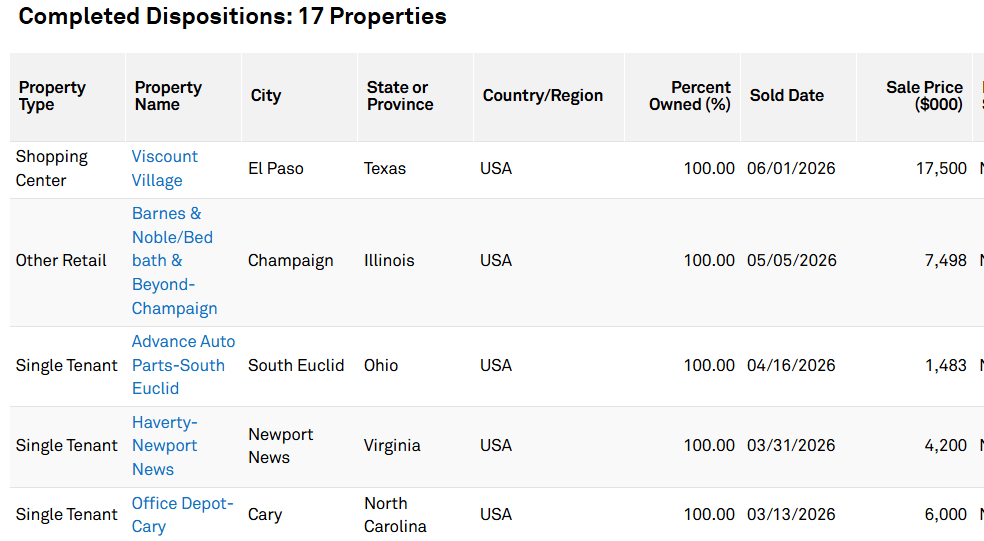

So far in 2026 OLP sold 5 properties.

S&P Global Market Intelligence

Proceeds went to buying a portfolio of industrial assets and a parcel of land.

S&P Global Market Intelligence

There will be a few more quarters of negative NOI tradeoff due to heavy acquisition/disposition activity. This will counteract the positive same-store NOI of the rest of the portfolio causing roughly flat AFFO/share in 2026.

2027 and beyond are well positioned for AFFO/share growth. As the portfolio gets closer to 100% industrial, there will less negative cap rate trade-off from transition and more organic growth.

With the acquisitions already executed they are very close to that threshold. OLP is now a company with moderate forward growth. This has substantial implications for valuation.

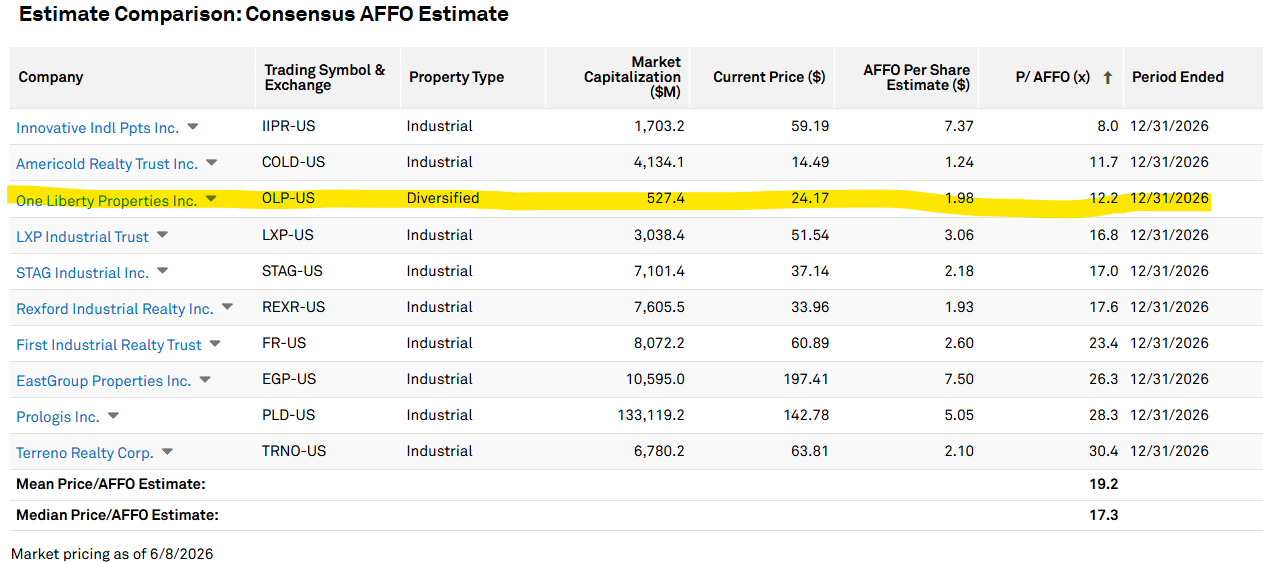

Industrial REITs trade at a median AFFO multiple of 17.3X. OLP trades at 12.2X.

S&P Global Market Intelligence

Americold (COLD) and Innovative Industrial (IIPR) are in cold storage and cultivation, respectively which each have entirely different fundamentals.

OLP is by far the lowest multiple among the traditional industrial property REITs. Its peer set ranges in AFFO multiple from16.8X to 30.4X.

I think OLP will and should trade slightly below its peer set due to 2 factors:

In my opinion, fair value is about 15X AFFO. This implies a market price of $29.7 or about 22% above current market price.

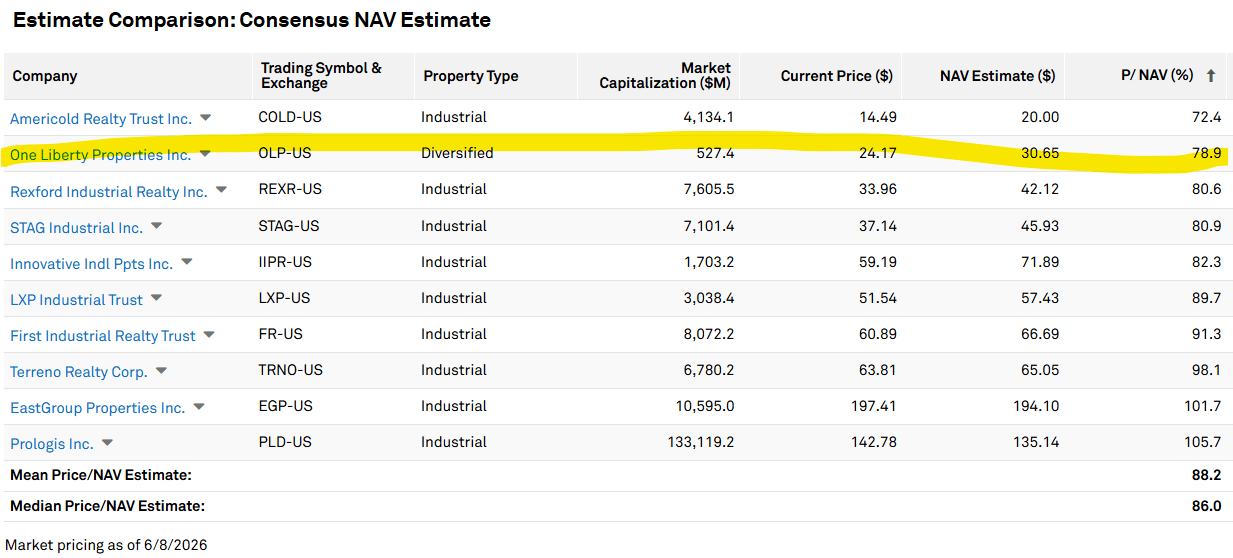

This fair value is backed up by net asset value which sits at $30.65.

S&P Global Market Intelligence

While OLP is well positioned to grow steadily going forward, that growth may not appear in 2026 depending on which metric one looks at. There are 2 upcoming headwinds:

As 2026 acquisitions/dispositions largely did not impact the 1Q26 numbers, 2Q26 could come in slightly lower.

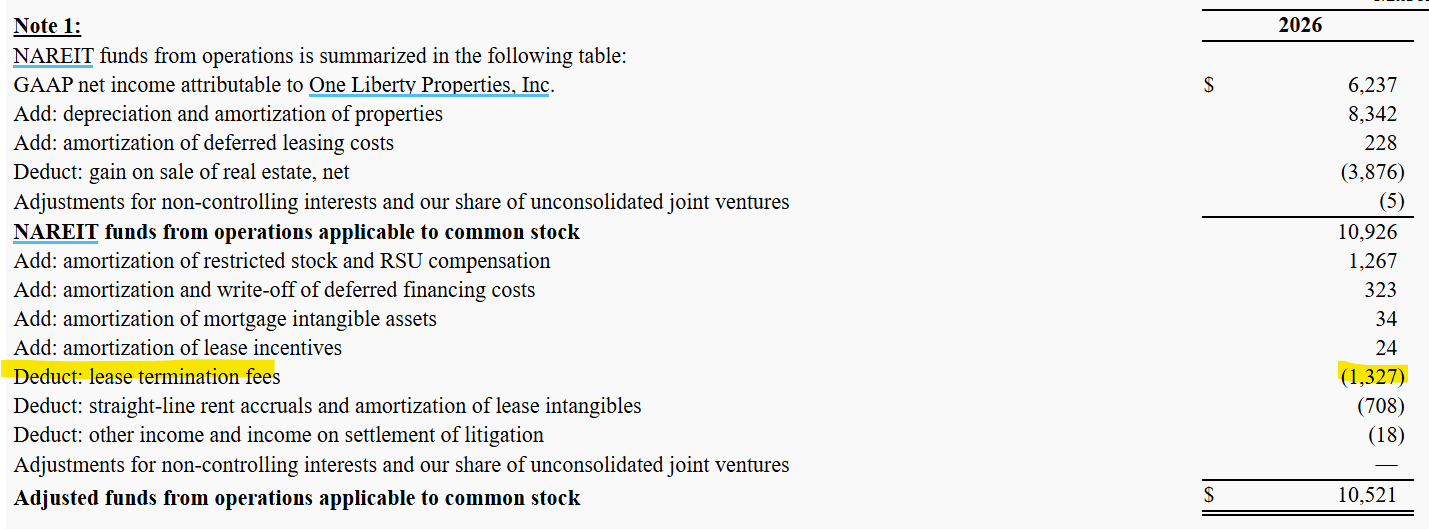

Additionally, OLP had a $1.3 million one-time gain in 1Q26 which will of course not recur in 2Q26. The lease buyout was a favorable event which will lead to higher NOI in the long run as described in the 10-Q:

“In March 2026, we recognized an aggregate of $1.3 million from two industrial tenants in lease buy-out transactions; we replaced such tenancies on economic terms more favorable to us than those of the terminating tenancies.”

OLP properly adjusted for it in AFFO by removing the gain from their AFFO number.

Supplemental

Thus, AFFO will not move down in 2Q26 as a result, but FFO will. $1.3 million is about 6 cents per share so expect AFFO to come in flat in 2Q and FFO to come in well below 1Q26 numbers.

This could result in adverse trading depending on which metric the market is focusing.

OLP intentionally runs a high dividend payout ratio, most recently at 96.3%.

S&P Global Market Intelligence

Given how steady their cashflows are, I don’t see much risk of a cut. However, I would prefer that the company lower their payout ratio over time as growth comes in.

In my opinion, it would be a mistake to raise the dividend 5 cents when AFFO/share grows by 5 cents.

80% is a healthier payout ratio for an industrial REIT to retain some cash for growth and a rainy-day fund.

I also believe OLP would benefit substantially from holding public earnings calls. REITs that don’t communicate broadly with the public often trade at discounts (look at Saul Centers as an example).

One Liberty Properties is still trading at the multiple of a no-growth company. 12.2X AFFO is too low of a multiple for an industrial REIT with organic growth including strong escalators.

As the growth comes in and the market recognizes that OLP is now an industrial REIT, I suspect the multiple will expand to around 15X. Buying at today’s price offers 22% upside to fair value along with a 7.5% dividend yield.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。