Rupee fall: Complex factors at play | Photo Credit: Rasi Bhadramani

For the past few months, the decline in the value of the rupee and the RBI’s efforts to contain it have become the among most discussed features of the Indian economy. There is no doubt that the decline in the nominal value of the rupee, especially with reference to the US dollar (which has otherwise been declining itself with respect to other major currencies) has been sharp.

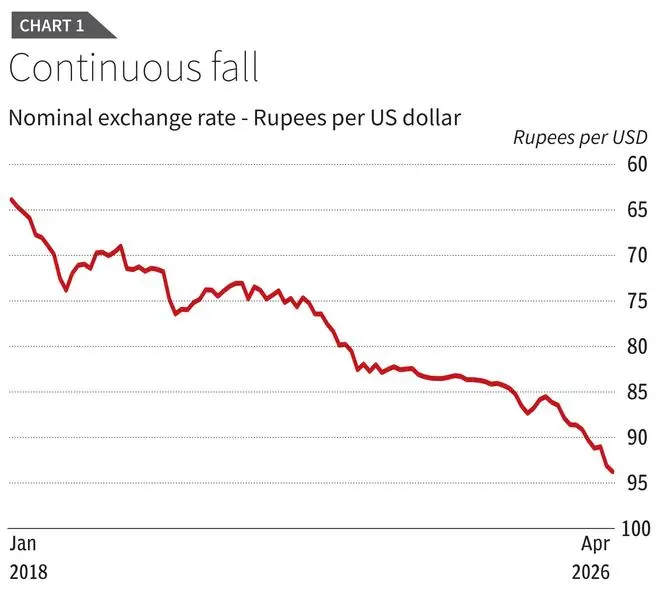

Figure 1 shows that this is not a new tendency, and that the rupee has fallen almost continuously since 2018, by nearly 50 per cent. However, the recent decline, since the turn of the year, has been especially sharp.

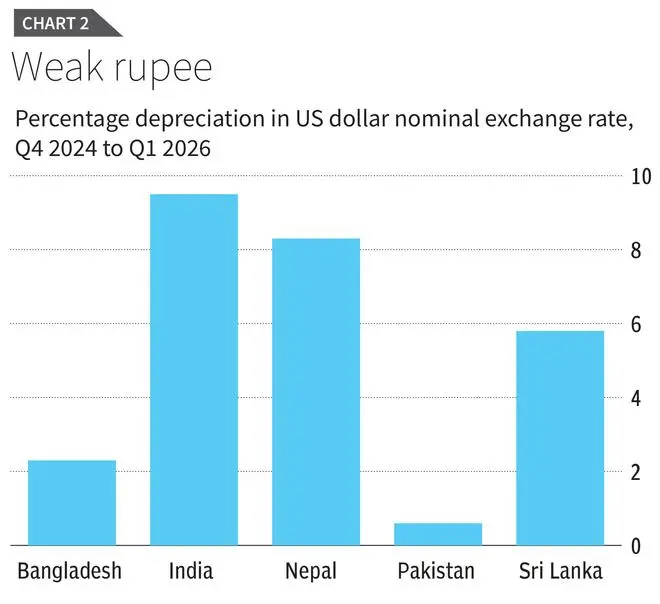

Indeed, the period since the US-Israel war on Iran has been especially bad for the Indian rupee. The currency has underperformed, not only with respect to its peers in the BRICS countries, but more tellingly even in South Asia. Figure 2 shows how (taking an average of the values in every quarter) between Q4 (Oct-Dec) of 2024, before the war started, and up to Q1 (Jan-Mar) of 2025, the Indian rupee depreciated more than all other South Asian currencies.

Bear in mind that all our South Asian neighbours are experiencing various degrees of political and economic crisis or instability, and the poor performance of the Indian rupee becomes even more telling.

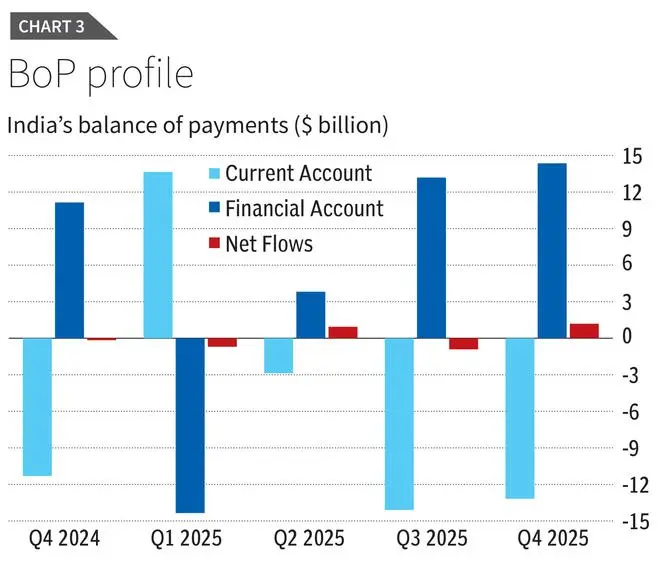

Normally, changes in the overall balance of payments would provide a clear answer as to why this has been occurring — and that too, so dramatically. Either current account deficits would have grown without adequate change in capital inflows, or financial outflows, in the form of capital flight, would have triggered this process of rupee decline. Of course, if both occur together, then a sharp decline is only to be expected.

But this is where the issue becomes more complex. An examination of the overall balance of payments data does not suggest such a severe imbalance over the past year that would generate such a change in the value of the currency. In fact, the net balance of payments appears to have been largely stable in 2025.

As Figure 3 indicates, there was a brief period of January-March 2025 when the current account was in net surplus (largely due to the inflow of foreign remittances and the decline in imports, including oil and gold). But this was counterbalanced by net capital outflows in the period. In all other quarters since the last quarter of 2024, the current account has been in deficit while the financial inflows have been positive.

This seems to be counterintuitive. There has been much evidence — and discussion — on the increased extent and pace of private financial outflows, so this seems quite contrary to the observed reality of capital flight that the RBI is now apparently trying to control. But if net capital inflows have been positive, and more than balanced the current account deficit, then how and why is the rupee depreciating in value?

The answer obviously requires further investigation, but one hypothesis is clearly worth exploring. This is the growing role of internal trade in the rupee, through banks, foreign exchange brokers and other such entities, who have been speculating on the possibility of future declines in rupee value and have thereby made their own expectations self-fulfilling. To the extent that such trades do not require the intermediation of the RBI, they would not be reflected in the balance of payments. And large legacy holdings of dollars or other “hard currencies” within the country could be part of this trade.

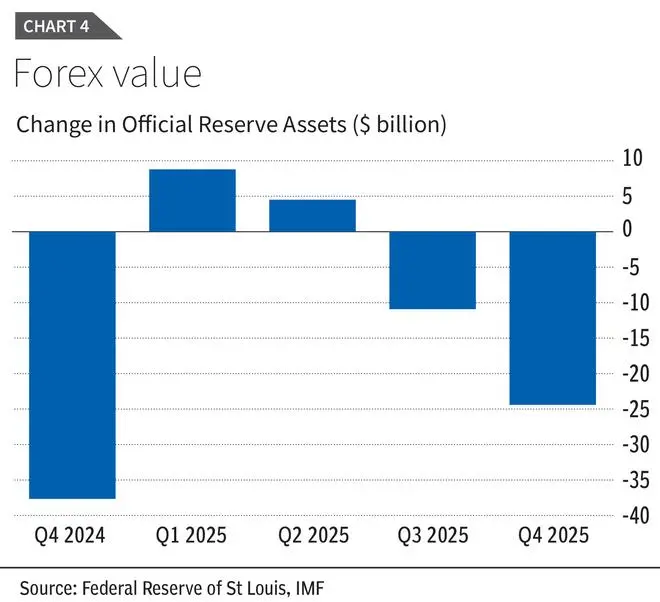

Also, as and when the RBI intervenes in forex markets, its actions also contribute to the “financial flows” that appear in the balance of payments. And such intervention has been strongly evident in the past year. Figure 4 indicates the very large changes in the value of foreign exchange reserves held by the RBI, with a fairly sharp decline of nearly $38 billion in the last quarter of 2024.

Thereafter there were two quarters when forex reserves were built up once again, but since July 2025 there has clearly been a revival of open market operations by the RBI, with rupee purchases designed to stabilise the currency. These would effectively be part of the net financial inflows.

This was so extensive that apparently the RBI recorded a net sale of $53.1 billion of reserves in the financial year 2025-26. This was around $12 billion more than its net sales in the previous financial year. And there seem to be no signs of this abating: as recently as Thursday May 21, the RBI apparently sold at least $2 billion in the open market on one day alone.

So some of what appear to be “market fundamentals” could actually reflect the RBI operating to curb speculative activity in the forex market, in a situation in which domestic financial agents and traders are able to use their deregulated powers to bet on a falling rupee. This helps to explain some of the other measures the central bank has taken. In March, the central bank put a limit of $100 million on net open rupee positions of banks, which are estimated to have grown to significant levels of anywhere between $25-25 billion. But this had little effect as banks then exited their position by offering them to corporate clients. As a result, in early April, the RBI barred banks from offering rupee non-deliverable forwards to resident and non-resident clients and barred companies from rebooking cancelled forward contracts.

Essentially, therefore, the RBI is fighting speculative activity that has become much harder to control after various financial deregulation measures allowed the onshore trading of the rupee. It was only to be expected that such speculation will accentuate and intensify the economic pressures that are already evident and likely to become even worse as global economic uncertainty persists. The need for greater financial regulation has never been more evident.

Published on May 26, 2026

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。