For an asset class built on the premise that no one else holds your keys, the honest answer has usually been: nothing good. Self-custody hands you complete control and, in the same motion, removes the safety net that a bank, a broker or a probate court would normally provide. Lose the keys and the coins are inert. Die without a plan and your heirs inherit a puzzle they may never solve.

Kresus, a San Francisco self-custody wallet firm, put a product against that problem. Kresus Inheritance lets a user name a beneficiary who can access their portfolio only after a defined period of account inactivity has passed. Private keys are never shared during the process, the company says, and Kresus does not take custody of user assets. It costs $99.99 a year and sits inside the existing wallet.

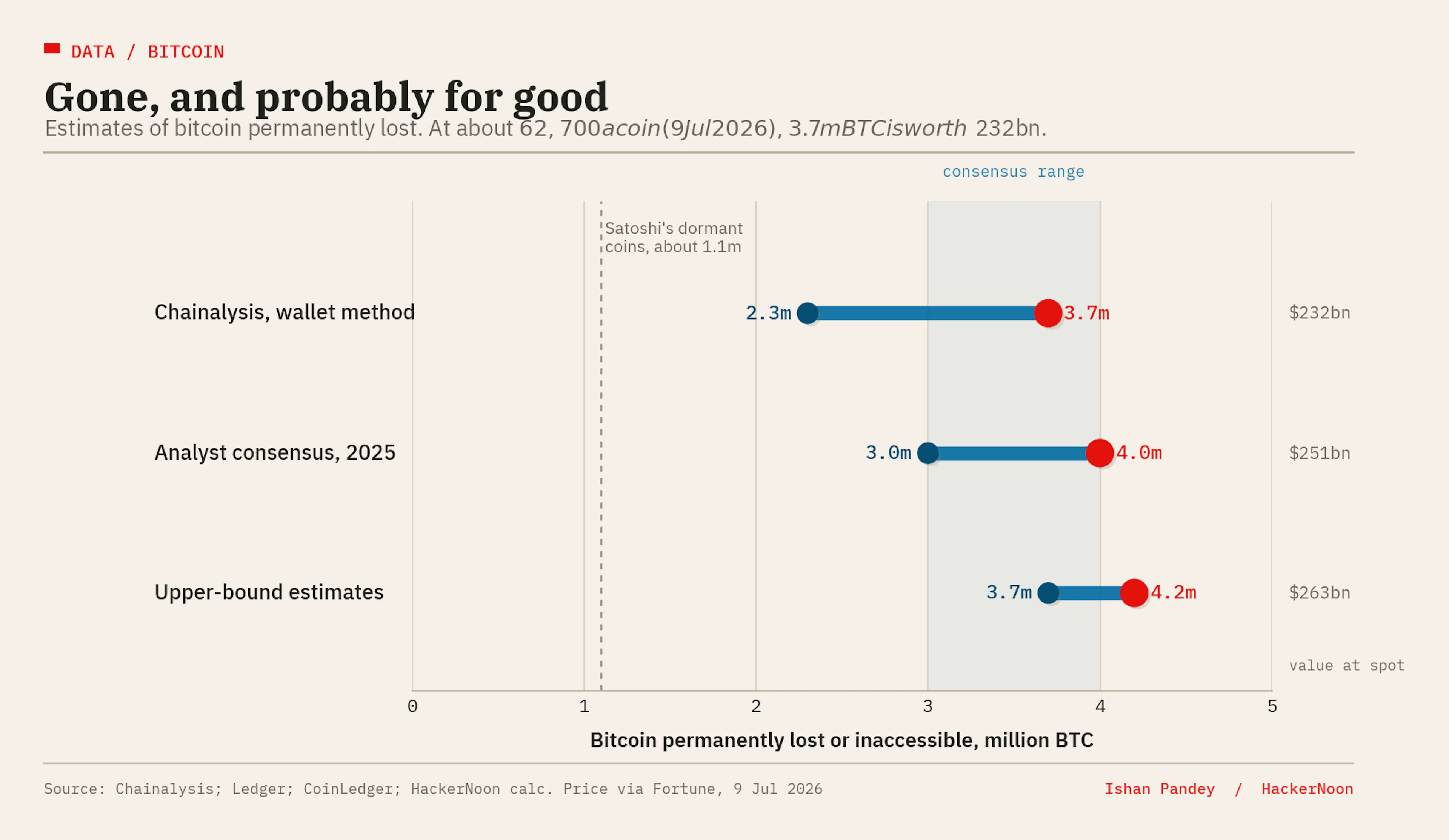

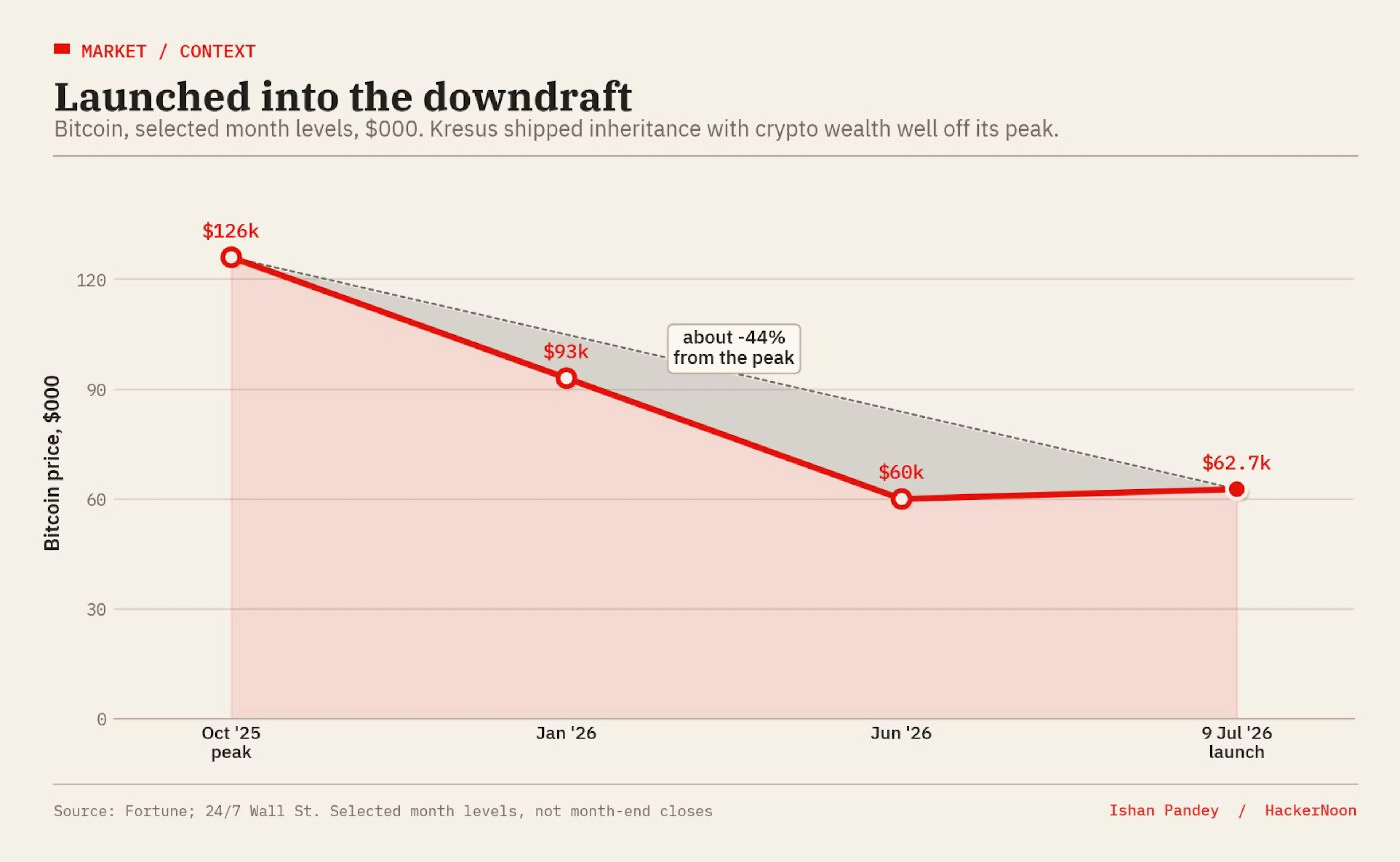

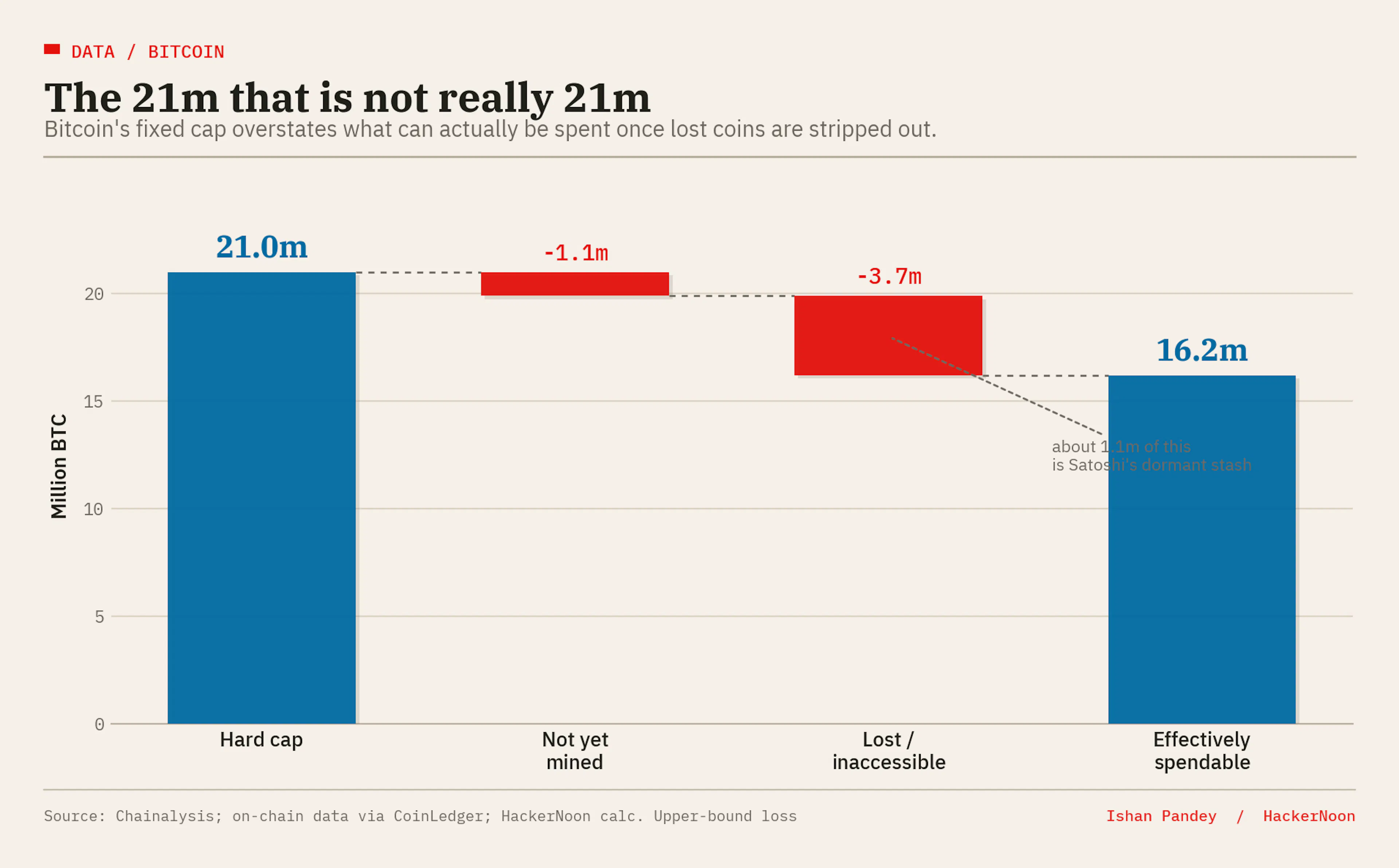

The scale here is not rhetorical. Blockchain analytics firm Chainalysis has estimated that between 2.3 million and 3.7 million bitcoin are permanently lost, and most analysts settle on a range of 3 to 4 million, or roughly 15 to 20 percent of the 21 million that will ever exist. At about $62,700 per coin on the day Kresus launched, with bitcoin down around 44 percent from its October 2025 high, the upper end of that lost pile is worth close to $232 billion. Some of it belongs to Satoshi Nakamoto. A great deal of the rest belongs to people who died, or who simply forgot, and told no one where to look.

Estimates of permanently lost bitcoin, in millions of coins.

Estimates of permanently lost bitcoin, in millions of coins.

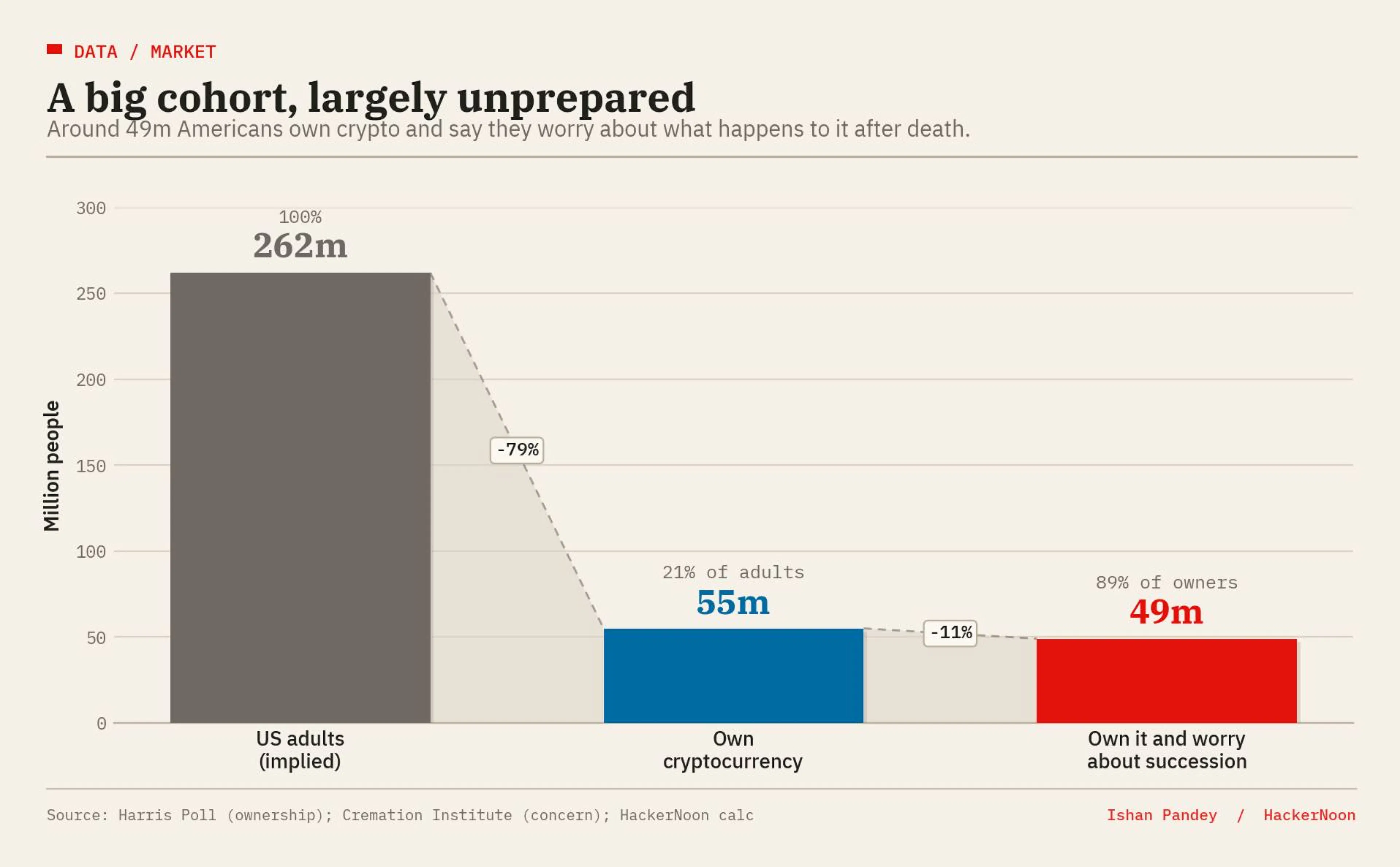

That is the supply-side tragedy. The demand-side anxiety is just as measurable. A Harris Poll cited by Kresus puts US crypto ownership at 55 million adults, about 21 percent of the population, while a Cremation Institute study found that 89 percent of crypto investors worry about what happens to their holdings after death. Put those two figures together and you get a cohort of roughly 49 million Americans who own crypto and are actively uneasy about its fate. Very few of them have done anything about it.

Ownership meets anxiety: the addressable, and largely unprepared, market.

Ownership meets anxiety: the addressable, and largely unprepared, market.

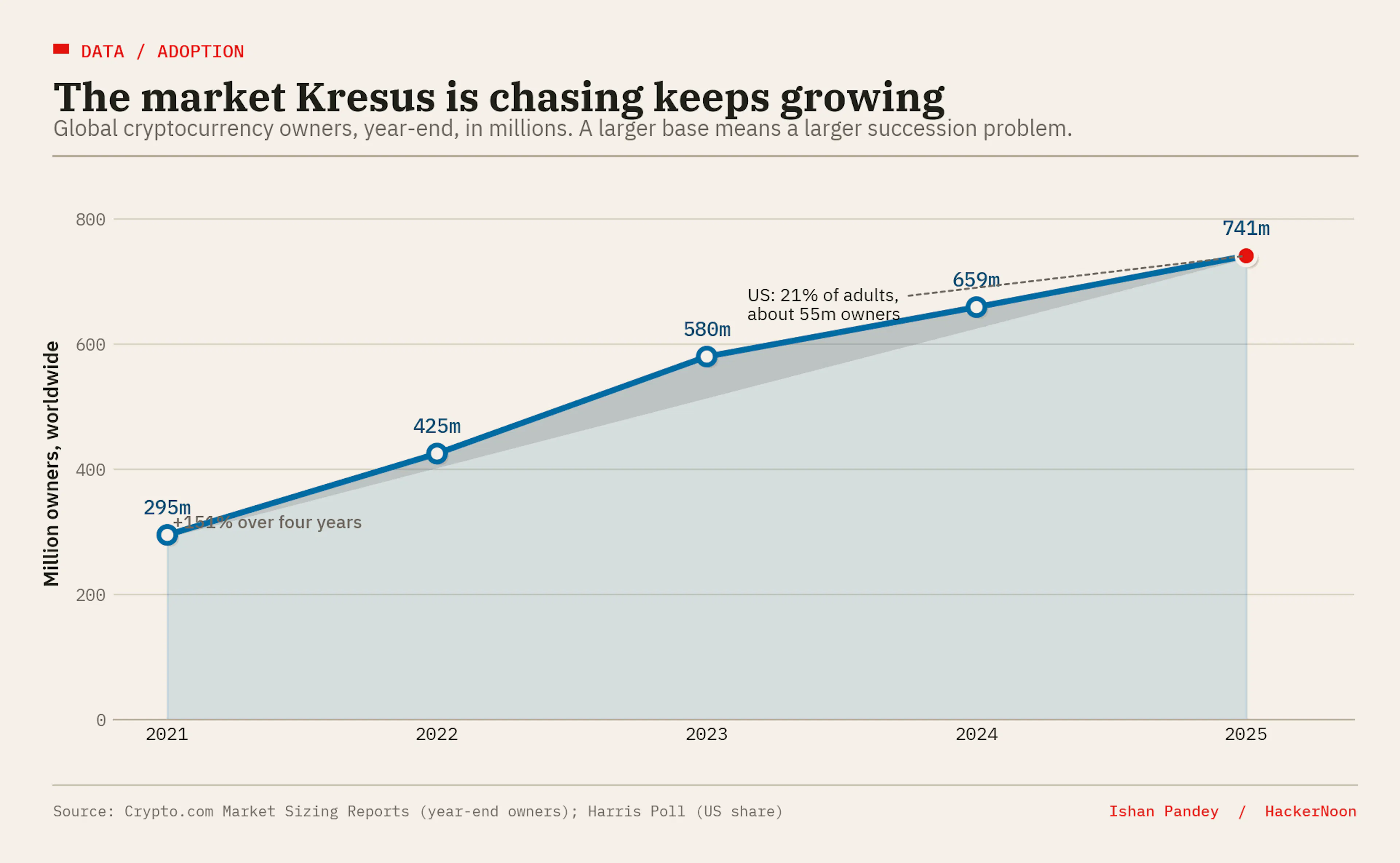

And the base keeps expanding. Global crypto owners rose from roughly 295 million in 2021 to 741 million by the end of 2025, on Crypto.com's count, a gain of more than 150 percent in four years. Every fresh cohort of holders is a fresh cohort of unsolved succession, which is precisely the demand curve a subscription feature wants to sit in front of.

Global cryptocurrency owners, year-end, in millions.

Global cryptocurrency owners, year-end, in millions.

Strip away the language and Kresus Inheritance is an inactivity-triggered succession mechanism, closer in spirit to a dead man's switch than to a will. The wallet owner stays in full control while active. If the account goes quiet for a defined window, a claim process opens for the named beneficiary. Nothing changes hands early, which neatly sidesteps the two worst do-it-yourself options: writing a seed phrase on paper that can be found, and handing keys to an heir who can then spend or lose them prematurely.

This is consistent with how Kresus has always positioned itself. The wallet is built on Base and Solana, leans on ERC-4337 account abstraction and markets a seedless experience secured by biometrics and device hardware rather than a twelve-word phrase. Traina, a serial entrepreneur and former US Ambassador to Austria, has described the goal as giving users "the comfort of your own bank." Inheritance is a logical extension of that thesis: take a feature that traditional finance treats as table stakes, the beneficiary designation, and bolt it onto self-custody.

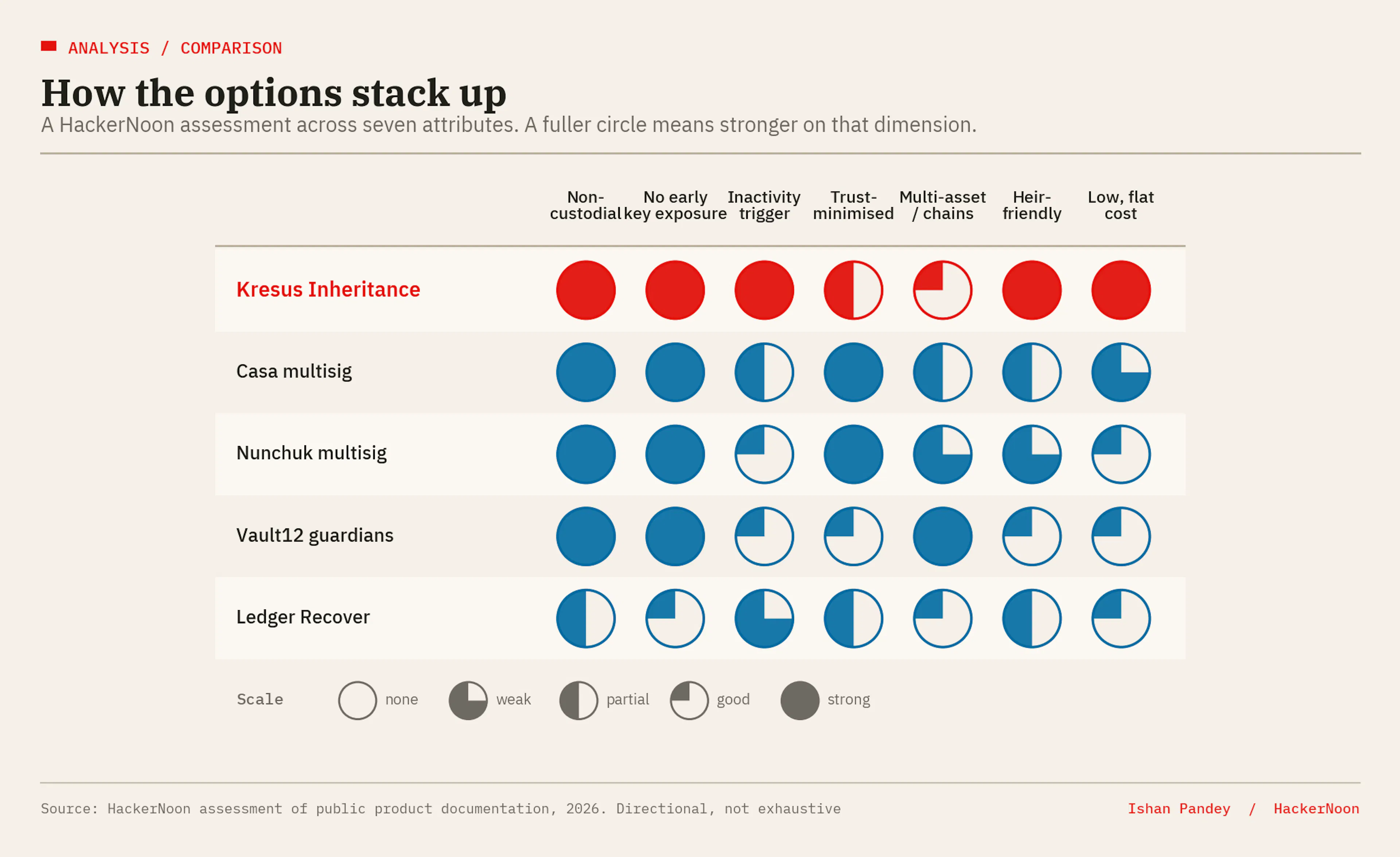

Kresus's release uses the word "pioneers." It should be read with a raised eyebrow. Crypto inheritance is not virgin territory. Vault12 has marketed itself as the category pioneer for years, using a guardian network that splits encrypted recovery shares across trusted contacts. Casa and Nunchuk offer multisignature inheritance, where the owner holds most keys and a service holds one, releasing it only after legal verification and a timelock. Ledger Recover shards a seed phrase across custodians. Each of these is more trust-minimised than a single-vendor inactivity switch. Each is also harder to set up and, for a non-technical heir, harder to execute under grief.

That trade-off is the whole story, and it is worth seeing on one plane.

The last mile of self-custody, mapped on ease against security. Bubble size is annual cost. Positions are a HackerNoon assessment.

The last mile of self-custody, mapped on ease against security. Bubble size is annual cost. Positions are a HackerNoon assessment.

Read attribute by attribute, the same picture holds. Kresus leads on the things a mainstream user feels, custody, key safety and heir-friendliness, and trails the multisig services on trust-minimisation, the thing a security purist prizes most.

A directional scorecard across seven attributes. A fuller circle is stronger.

A directional scorecard across seven attributes. A fuller circle is stronger.

The multisig cluster sits top-left: very secure, genuinely demanding. The do-it-yourself options sit bottom-right and bottom-left: cheap and either exposed or unusable by heirs. Kresus is making a deliberate move to the right, buying accessibility and a low, flat price at the cost of some trust-minimisation. For the 21 percent of adults who own crypto but are not crypto-native, that may be exactly the right trade. Whether it is the safe one depends on details the launch does not fully disclose.

Three questions deserve answers before anyone entrusts a legacy to a subscription.

First, mechanism. "No private key sharing" and "beneficiary gains access" are difficult to reconcile without either a smart-contract handoff, a shard-recovery scheme or some privileged role for Kresus at the moment of claim. The release does not say which. If access ultimately depends on Kresus running the succession process, then the non-custodial claim is doing lighter lifting than it appears, and vendor risk becomes inheritance risk.

Second, the failure mode of the trigger itself. Inactivity is a blunt proxy for death. A long illness, a lost phone, a stint offshore or simple neglect could start the clock. Casa uses a six-month timer once a claim begins; Nunchuk layers a timelock, a buffer period and owner notifications so the living can cancel a premature claim. Kresus will need comparable guardrails, and users will want to see them spelled out.

Third, scope and enforceability. Does the feature cover assets across chains, or only what sits in the Kresus wallet? Does a beneficiary designation inside an app carry any weight against a probate court or a contesting relative? These are not pedantic points. Inheritance is where software meets estate law, and the seam is where things break.

Zoom out and the launch reads as strategy more than charity. Kresus, founded in 2022 and backed by roughly $38 million in funding through a Series A that closed in February 2026, is trying to graduate from a place you store assets into a place you manage wealth. Inheritance is a sticky, recurring-revenue feature that deepens the relationship and, not incidentally, gives a bear-market wallet a reason to charge a subscription. Launching it with bitcoin down sharply from its peak is either awkward timing or shrewd timing, depending on your view: prices fall, but the structural problem of lost coins does not.

Bitcoin, selected month levels. Kresus shipped inheritance with crypto wealth well off its October 2025 high.

Bitcoin, selected month levels. Kresus shipped inheritance with crypto wealth well off its October 2025 high.

Bitcoin's hard cap overstates what can actually be spent once lost coins are removed.

Bitcoin's hard cap overstates what can actually be spent once lost coins are removed.

And that structural problem is the real prize. Every coin lost to a death without a plan is removed from circulation forever, quietly tightening supply for everyone who remains. Solving inheritance is good for individual families. Done at scale, it is also good for the asset. The question Kresus has picked is the right one. The market will decide whether a $99.99 wallet feature is a real answer or a comforting one.

Don’t forget to like and share the story!

Vested Interest Disclosure: HackerNoon has reviewed the report for quality, but the claims herein belong to the author. #DYOR.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。