In KPMG’s 2025 Banking Survey, 91% of banking executives said data‑driven insights and personalisation are their top investment priorities. They see utilising data as the clearest path to operating efficiency and customer satisfaction.

The survey also highlights data privacy as one of the biggest obstacles to getting there. There’s a clear need for privacy-centric solutions and ethical data tools. Teams need ways to work with and analyse behavioural data, but without over-collecting, over-tracking or violating local requirements.

This piece looks at how data analytics in banking personalise financial services, reduce risk and support decision making, as well as how privacy-first solutions like Matomo help teams do it responsibly.

Data analytics in banking is the process of collecting, organising and analysing financial, marketing and customer information to understand performance and make better future decisions.

It turns large volumes of raw data, such as transactions, channel performance or operational records, into meaningful insights that can support everyday banking operations and long-term strategy.

For example, instead of a bank seeing a simple list of monthly withdrawals, banking analytics identifies a consistent pattern of transfers to brokerage firms. With this insight, the bank can offer its own investment products to the customer.

Data analytics helps banks identify strategic goals and work towards them with confidence, whether the focus is growth, customer retention or entering new markets. Data helps reveal problems to fix and opportunities worth investing in.

Without data analytics, decision makers don’t know how bad a problem might be or how good an impact a simple change might create. There’s no way to pinpoint what’s really driving customers away or what’s bringing them in.

Ultimately, data helps answer questions that drive success. What onboarding steps are creating the most friction with customers? Which regions are the most profitable? Which transactions have the highest fraud risk? The wins for banks are more clarity, the ability to pivot faster and less risk. Let’s take a look at how these data analytics benefits play out for banks.

Boards relying on quarterly reports show past performance but offer limited forward visibility. This makes long-term planning slower.

Data analytics brings financial, operational and risk data into a single view. For example, predictive modelling can help directors evaluate potential outcomes before making any decisions. Similarly, indicators such as forecasted risk exposure or revenue trends help banking leaders stay in control.

Interest rate changes, economic uncertainty and evolving regulations all affect the banking environment. Traditional reporting methods may not be able to catch up when there are sudden shifts in rates, regulations or the market.

With analytics, banks are able to track performance trends in real time and test potential outcomes through scenario analysis. Tracking margin movement or liquidity trends can help banks adjust pricing, lending strategies or risk posture earlier, improving organisational agility.

Finding out in which area capital delivers the best returns is difficult when banks rely only on overall profit numbers.

Data analytics allows deeper visibility into product performance, customer segments and regional activity. Metrics on factors such as product profitability, marketing channel performance and cost efficiency help shift resources towards sustainable growth rather than historical priorities. As a result, banks can identify high-margin areas, reassess legacy offerings and refine branch investment decisions.

An institution’s true value can be difficult to judge when customer behaviour patterns and portfolio risks are unclear.

Analytics allows banks to examine customer retention, credit quality and what products or segments carry risks. These reveal warning signs like which portfolios are profitable but carry hidden threats. This information leads to better acquisition decisions and fewer post-merger surprises.

Customer attrition can happen without any signals when systems are disconnected.

However, analytics allow teams to comprehensively look into usage behaviour and churn indicators to understand customer needs and product affinity. This early identification can guide timely retention efforts, improving customer lifetime value.

Uniform messaging won’t work for individual financial needs and choices.

Analytics helps banks to understand customer spending habits and interaction history. This can help with personalised outreach and improve engagement and conversion while also building trust. For example, if a customer repeatedly checks loan options in a banking app but doesn’t apply, this signals interest and allows the bank to share helpful guidance instead of broad promotions.

So, how are banks and other financial institutions using data analytics to improve customer engagement, reduce risk and drive growth? Let’s take a look.

Banks are using analytics for everything from fraud detection to ad optimisation. It’s powering faster, more confident decisions related to lending, marketing and operations.

Some use cases involve real-time monitoring for faster responses, while others involve drawing on historical data to create context for big-picture decisions that drive growth. All of these banking analytics use cases involve collecting and analysing data while maintaining privacy controls and consent requirements. That way, insights can feed decisions without eroding customer trust or impacting compliance.

Analytics allow banks to assess if a borrower can repay a loan and track lending risk.

Banks use analytics to detect suspicious activity by combining different types of customer and transaction data that may look normal on their own.

According to the U.S. Department of the Treasury, enhanced fraud detection processes that rely on data analysis and AI prevented and recovered more than $4 billion in fraud and improper payments in 2024.

Analytics helps banks group customers based on behaviour and life stage so services match real financial needs.

Banks use analytics to reduce friction in everyday processes while maintaining service quality.

Analytics helps with transparency so banks can meet privacy regulations.

Fintech firm 7Assets needed a familiar balance: better insight with strict privacy.

After moving to Matomo, the team limited collection to what was necessary, tracked website and in-product journeys and used session recordings to prioritise fixes while reducing legal overhead.

They were able to focus on collection, document decisions and keep users’ rights central with Matomo’s privacy-first approach to banking analytics.

Banks are using data analytics in new and evolving ways. The trends below explain the key shifts driving this change.

AI and machine learning can analyse large volumes of data fast. Machine learning models score transactions, prioritise sales opportunities and predict late payments. Large language models summarise customer cases and draft support responses, and predictive models identify churn risk and recommend next-best actions for customer engagement.

With real-time analytics, banks can track events as they happen instead of reviewing them hours or days later. For example, real-time systems can flag a card used in two distant locations within minutes. Repeated small payment attempts may trigger temporary card blocks before larger fraud occurs. Shared real-time data also helps service teams respond faster when customer behaviour signals frustration or urgency.

Banks are adopting advanced analytics to support sustainable financing decisions. ING, for example, has developed AI models that analyse sustainability indicators, evaluate transition strategies of high-emission businesses and benchmark environmental performance against industry peers.

HSBC is using computer vision and satellite imagery (remote sensing) to monitor forest cover, check biodiversity and evaluate environmental risk exposure within its lending portfolio.

As data use expands, banks are adopting techniques that reduce exposure to personal information. Federated learning and synthetic datasets train fraud detection and risk models without sharing raw customer data. Processing data closer to devices, such as mobile apps or ATMs, enables faster responses while limiting data movement.

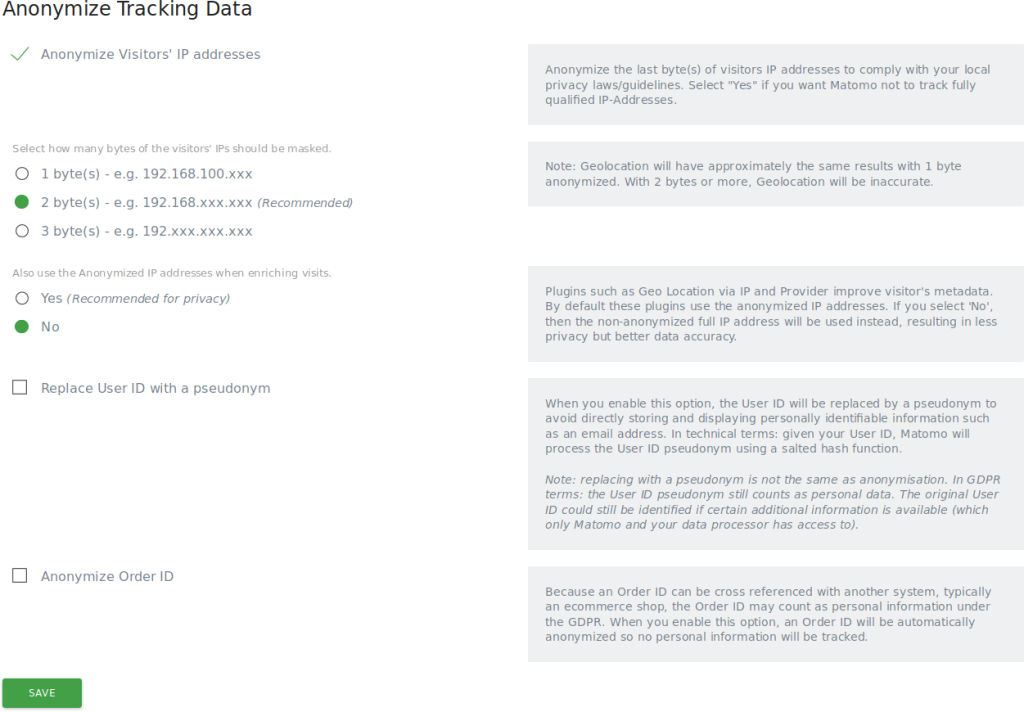

Growing reliance on analytics in lending, fraud detection and customer decisioning requires stronger data governance. Financial institutions need to follow responsible data practices to stay compliant, but also to maintain trust. Here are some ways banks are handling customer data ethically:

While there’s a lot on the horizon with AI-powered analytics and the adoption of privacy-first data management practices, there are still major challenges facing the industry.

Banks hold large volumes of customer data, yet making it usable, secure and compliant is hard work. From adhering to strict privacy rules to transforming data so it’s ready for analysis, these are the main challenges financial institutions face today when it comes to data analytics.

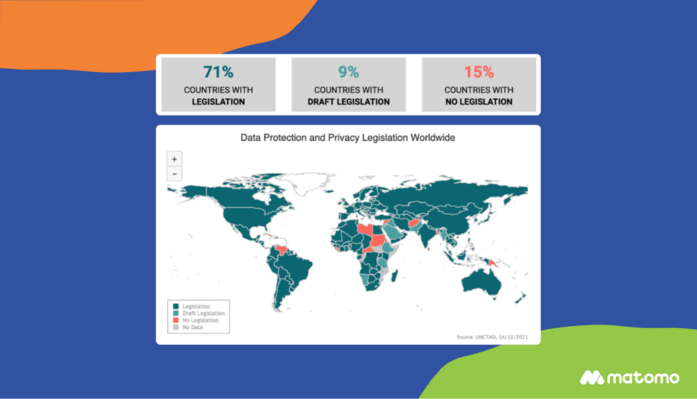

Banking operates under some of the strictest privacy rules of any industry.

Because these activities directly affect customers, regulators closely govern how financial institutions collect, analyse and transfer data. The main challenge is dealing with different rules across regions, which force banks to design analytics systems that remain compliant everywhere they operate.

In Europe, financial institutions have to follow the following data privacy regulations:

In the United States, there are several data privacy laws. Here are the main ones banks have to follow:

When navigating different regional laws, many banks adopt a practical strategy: they design analytics systems to meet the toughest regulatory requirements first and then adapt them for local markets. This reduces rework and helps teams scale analytics safely across regions.

Analytics is only as reliable as the data behind it, and banking data often comes from multiple systems built at different times. Customer names, dates, account identifiers and transaction categories follow different formats across platforms, which can lead to misleading insights and data confusion. Ad platforms also use their own data formats, making it difficult to compare cross-channel performance and determine which channels are bringing in customers.

Banks need the proper data infrastructure to make sure data is clean, structured and analysis-ready. Data cleaning and transformation involves removing errors and duplicates and structuring it so formats are aligned before they begin analysis.

Advanced analytics tools require investment in software, infrastructure, integration and skilled teams. Custom integrations with core banking systems can be expensive and slow.

Staff also need training to interpret results correctly and use models responsibly. A bank adopting a new analytics platform, for example, may spend months connecting historical data sources before seeing measurable value. The challenge is proving long-term return while managing short-term costs.

Matomo tracks channels and campaigns so banks can clearly see where new customers are coming from and what channels have the best return on investment (ROI) almost right away.

With filters and clear visualizations, it’s easier to turn data into insights quickly. And, your data stays private, so you won’t risk losing customer trust.

Privacy-focused analytics tools like Matomo can reduce regulatory friction by aligning technical design with legal expectations from the start.

Banks can use Matomo to:

All data stays under your control. And with our API and BigQuery and Data Warehouse export feature, you have the flexibility to pull raw data and move it to a warehouse for storage, giving you total control over where your data lives.

Data analytics is becoming the engine of modern banking.

Raw events and transactions are the fuel; models, governance and workflows turn that fuel into motion that improves service, reduces loss and finds new growth.

But engines also need brakes and gauges. Consent, data minimisation and audit trails keep programmes safe and fair, even as rules evolve and data volumes rise. That means joining behavioural and transactional data with a clear purpose, collecting only what’s needed and documenting every step.

Matomo helps teams do this with privacy-first analytics you own, accurate reporting without sampling and hosting options that fit banking controls. You get insight that’s defensible, and customers get confidence that their rights come first, as well as a great customer experience.

Start your 21-day free trial today. No credit card required.

Data analytics can help banks better understand their customers, so they can create a more engaging customer experience and optimise their marketing. It can reduce fraud risk, which leads to better compliance and higher customer trust. Data also helps leaders make better-informed operational decisions, helping banks become more sustainable.

Data analytics can help protect against fraud by analyzing aggregated historical data to flag high-risk transactions and assess risks using automated scoring. Banks can then use this information to mitigate issues in real-time.

Customers are very concerned about data privacy, and this is true across the globe. An analysis of financial app reviews worldwide published in Information and Software Technology found that customers are worried about their highly sensitive data being exposed during a breach, but they’re also uncomfortable with financial institutions sharing their data with third parties, particularly advertisers.

Many users won’t use an app if they’re asked to share personal information, such as location data or browsing history. They’re also likely to switch to a competitor if they feel the number of permissions is too high.

Banks can increase trust by being more transparent about how data is stored and shared. For example, providing clearer privacy policies can help. Using more robust privacy protection measures, such as having an opt-out function for web analytics tracking and making two-factor authentication available, can also help.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。