👋 Welcome to Climate Drift: your cheat-sheet to climate. Each edition breaks down real solutions, hard numbers, and career moves for operators, founders, and investors who want impact. For more: Community | Accelerator | Open Climate Firesides | Deep Dives

Hey there! 👋

Skander here.

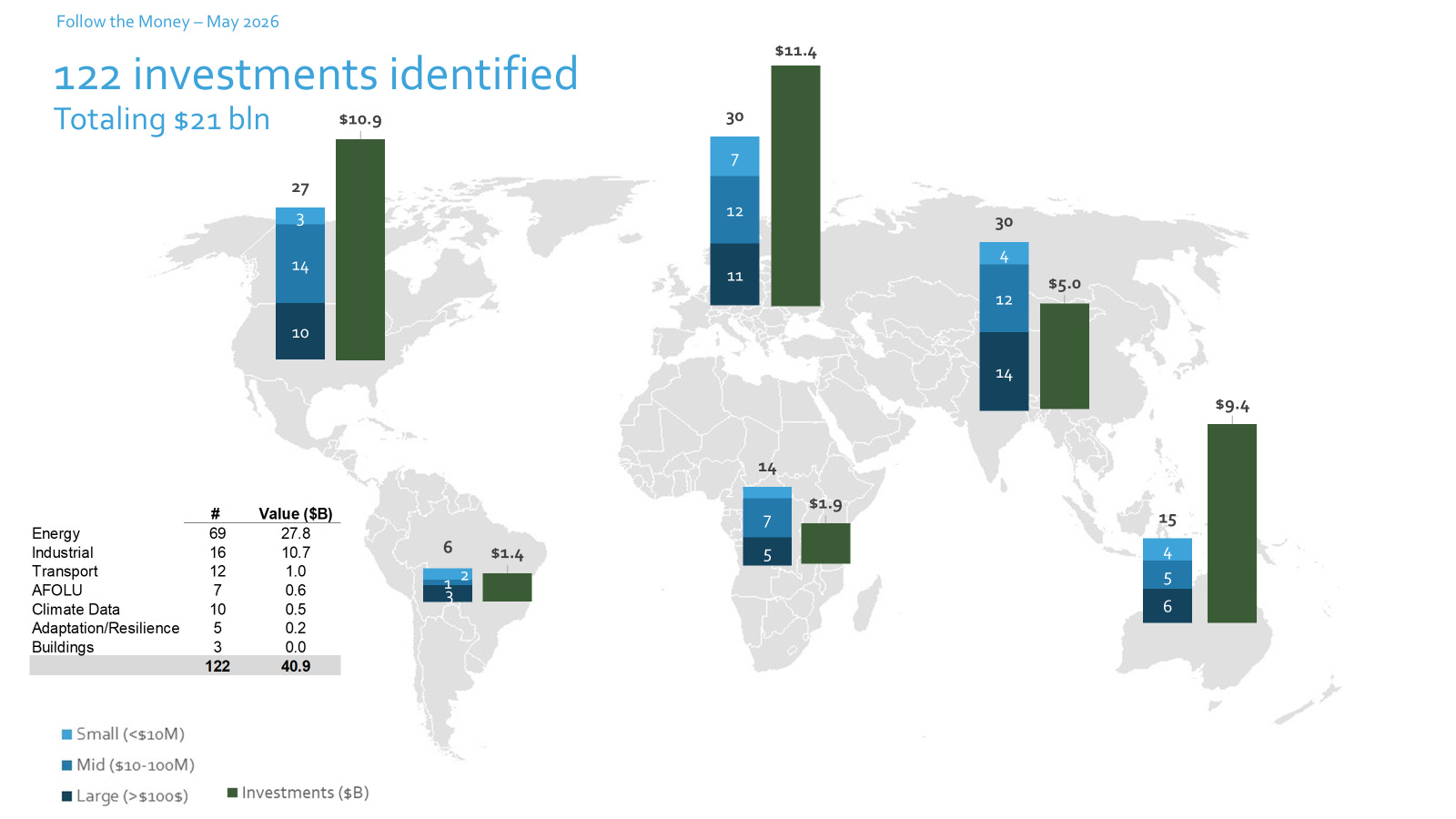

$41 billion across 122 deals. After April reset the ceiling at $55B, May settled back into a more typical month. The structure underneath sharpened, though: almost every big theme now routes through the AI energy bottleneck.

Jarek’s latest Follow the Money breaks down where the capital actually went, and the regional splits tell the story.

🇪🇺 Europe: $11.4B across 30 deals, leading the month. Two industrial anchors set the tone: Germany’s $5.9B Carbon Contracts for Difference scheme and Vulcan Energy’s €2.2B financial close for carbon-neutral lithium from geothermal brine (enough lithium hydroxide for ~500,000 EVs a year). Below them, one of the deepest mid-stage deep tech layers anywhere: Focused Energy’s $240M fusion Series A (RWE is providing a decommissioned nuclear site for the demonstrator), ICEYE’s €300M SAR satellite facility, and the EU’s first dedicated industrial heat auction, awarding €400M across 65 projects.

🇺🇸 North America: $10.9B across 27 deals, the sharpest thematic concentration of the month. The U.S. is buying firm, dispatchable power for the AI build-out at a pace no other region matches. Fervo Energy priced Wall Street’s largest clean energy IPO ever at $1.89B, opened 35% up, and closed above a $10B market cap, backed by a Google framework for up to 3 GW of enhanced geothermal. Thea Energy raised $100M for stellarator fusion, Enchanted Rock filed a ~$600M IPO on a $1.3B data center backlog, and Panthalassa raised $140M for floating ocean nodes that run AI inference on wave power.

🌏 Asia: $5.0B across 30 deals. China anchored the truck and battery rounds: Zeron raised a $200M Series B2 (roughly $400M in two months) for autonomous electric heavy trucks, and Sunwoda’s power unit added ~$228M ahead of a Hong Kong IPO. India filled the renewables long tail, led by CleanMax’s $575M project financing for ~1 GW of C&I solar and wind, plus Bhutan’s $515M Dorjilung hydropower scheme.

🌍 Rest of World: $13.6B across 35 deals. Australia had a huge month at $9.4B, driven by the A$7.2B Cheaper Home Batteries program and Edify Energy’s $2.08B solar-plus-storage close, with Rio Tinto buying 90% of output for 20 years to power aluminium smelting. Brazil’s Acelen closed $1.5B for a biorefinery producing 1 billion liters of SAF and renewable diesel per year.

A few patterns worth flagging: a cluster of raises (GridCARE, Utilidata, Nyobolt, Iceotope, Star Catcher) exists purely to feed or firm AI compute, so climate capital is increasingly AI-energy capital. The EU heat auction went 77% to mature resistance heating, with zero geothermal, a reminder of how early industrial heat electrification still is. And the strangest signal came from a trading desk: Mexico City’s Moreton Capital is raising $500M to trade corn, palm oil and wheat against a super El Niño that NOAA now gives two-in-three odds by winter. Climate finance has started pricing the weather itself.

🌊 Jarek breaks it all down below, region by region, theme by theme.

But first: Who is Jarek?

Jarek Dmowski is a global transformation leader who partners with high-growth companies with positive climate impact. He combines industry and climate finance expertise with a strong track record of driving growth—across PE/VC-backed scaleups, ABN AMRO, and BCG.

He scaled a data-driven technology company ~2.5x to ~$25M in revenue and led post-merger integrations that enabled ~6x accelerated growth. At a global financial institution, he spearheaded a $2B capital reallocation toward new energy and mobility. He also developed a comprehensive climate plan that translated the Paris Agreement into actionable targets across sectors and established a $250M program to drive efficiency gains and reduce emissions at an energy utility.

Jarek is passionate about how the climate transition reshapes economies and business models, creating significant opportunities for multi-country growth and impact.

Welcome to the next edition of “Follow the Money” - a monthly briefing on the capital flows shaping the climate transition.

$41B in May. America’s ~$2B geothermal IPO. A €2.2B carbon-neutral lithium close. And Europe’s first industrial-heat auction.

After April reset the ceiling at $55B, May settled back into a more typical - but still substantial - month: 122 tracked climate-related investments worth $41B.

The most striking signal may not have come from a startup round, but from a trading desk. Mexico City-based hedge fund Moreton Capital Partners is reportedly raising $500M for a special-purpose vehicle to trade commodities exposed to a potential “super El Niño” - from South African corn and Malaysian palm oil to Australian wheat. With NOAA now putting the probability of a very strong event by winter at roughly two-in-three, the message is hard to miss: climate finance is not only about building the new system. It is also about pricing the physical climate risk.

On the financing side, the through-line was unmistakable: capital is being routed through the AI energy bottleneck. The U.S. took its biggest geothermal developer public in a ~$1.9B Nasdaq IPO. Fusion raised on both sides of the Atlantic. Europe closed a €2.2B carbon-neutral lithium-and-geothermal project. And a wave of grid-software, exotic-power and high-power-battery rounds all pointed toward the same customer: the data center. Let’s dive deeper.

Explanation of the approach and source data: The investment list was developed based on disclosures, newsletter monitoring and review of climate news. Although not exhaustive, 122 climate-related investment deals were tracked - amounting to roughly $41 billion (all data in US$), covering all continents and different life stages of companies and development finance programs. Data skew toward early-stage companies and investments, as well as development financing programs. We are continuously working to expand the data sources and coverage of investments.

So, where did the money flow in April 2026?

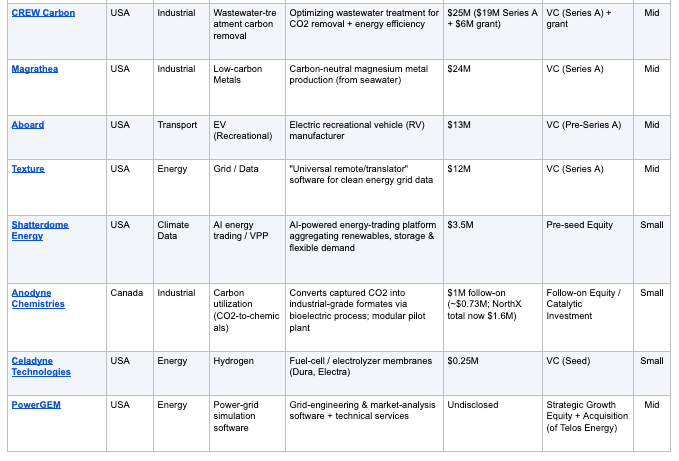

Europe led the month with ~$11.4B across 30 deals, followed closely by North America (~$10.9B, 27 deals) and Australia (~$9.4B, 15 deals) - the latter swollen by Australia’s federal budget programs. Asia (~$5.0B, 30 deals), Latin America (~$2.3B, 6 deals) and Africa (~$1.9B, 14 deals) rounded out the field. Unlike April, no single region dominated.

Energy once again dominated, accounting for ~$27.8B across 69 deals - by far the largest category, month after month. Industrial was a clear #2 (~$10.7B, 16 deals), lifted by Germany’s carbon-contracts scheme and Vulcan’s lithium close, followed by Transport (~$1.0B), AFOLU (~$0.6B), Climate Data (~$0.5B), Adaptation & Resilience (~$0.2B) and Buildings (~$36M). Buildings remained structurally undercapitalized relative to its emissions share - a persistent gap.

AI’s influence is now structural. A cluster of raises – grid-capacity software (GridCARE $64M, Utilidata $40M), exotic generation (Panthalassa $140M, Star Catcher $65M), high-power batteries (Nyobolt $60M) and data-center cooling (Iceotope $26M) – all exist to feed or firm AI compute.

Public and development finance anchored the market at scale. Multilateral institutions and government programs again supported well over $15B - from Germany’s ~$5.9B carbon-contracts-for-difference scheme and Australia’s battery and cleaner-fuels programs to a number of MDB and DFI infrastructure, adaptation and on-lending facilities across Africa, Asia and Latin America.

Let’s now dive deeper into 2026 watchlist themes (please refer to our December perspective for more details) and across regions to highlight technologies with real scaling potential over the next 3-5 years.

Which (of our 2026) themes were most strongly visible in April?

The divergence we have tracked since December held firmly in May. In North America, capital concentrated in dispatchable, capital-heavy power for the AI build-out. The headline was Fervo Energy, which priced Wall Street’s largest clean-energy IPO ever on May 12 at $27/share – above range – raising ~$1.89B (rising to ~$2.17B with the over-allotment) and opening ~35% up for a market cap above $10B. Its enhanced geothermal systems (EGS) turn horizontal drilling and fiber-optic sensing into engineered, dispatchable baseload, backed by a Google framework agreement for up to 3 GW. Fusion raised on both coasts of capital, too: Thea Energy closed a $100M Series B for its software-shaped “planar coil” stellarator, while gas-microgrid developer Enchanted Rock filed for a ~$600M IPO on the back of a ~$1.3B data-center backlog.

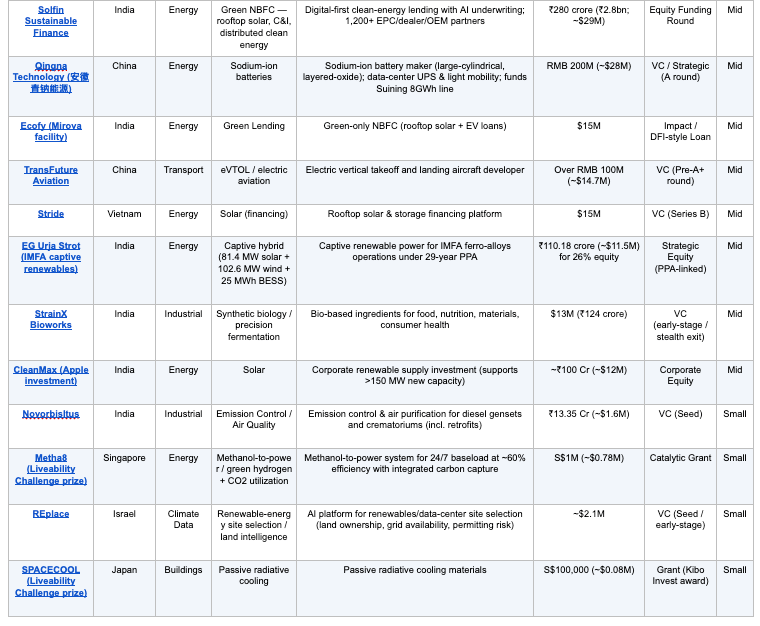

The “cheap batteries + localized electrification” thesis kept widening across road, rail, air and water. The deepest layer was again road freight in China: autonomous electric-truck maker Zeron (Jiangsu Zero One Auto) raised a $200M Series B2 – roughly $400M in two months – for vertically-integrated electric heavy trucks, while Zaihe Truck passed ~$140M cumulative financing for AI-defined new-energy trucks, including a hydrogen-electric flagship with ~1,500 km range. In the air, China’s TransFuture Aviation raised a ~$15M Pre-A+ for a tilt-rotor passenger eVTOL.

The supporting toolkit scaled too. Nyobolt (UK) closed a $60M Series C at a $1B valuation for niobium-anode batteries that charge 0–80% in under five minutes – built for warehouse robots, humanoids and data-center UPS rather than just cars. Austria’s REPS raised ~$24M for a magnet-based “road power plant” that harvests kinetic energy from decelerating trucks (already live at the Port of Hamburg), and Germany’s CMBlu Energy added a ~$59M initial Series C close for non-lithium organic flow batteries.

This was arguably the defining cross-cutting theme of May. As climate volatility and geopolitical risk converge, investors are funding companies that braid resilience, decarbonization and national security into a single thesis. Finland’s ICEYE secured a €300M (~$326M) revolving credit facility to scale the world’s largest SAR satellite constellation – all-weather flood and disaster monitoring with an obvious defense/intelligence dual-use. Tomorrow.io (USA) added $35M to its Series F for AI-native weather intelligence and its “DeepSky” satellites, with the U.S. DoD, Air Force and NASA among its customers. Star Catcher (USA, $65M) is building an orbital power grid – and has the former first Chief of Space Operations of the U.S. Space Force on its board – while Germany’s LiveEO ($33M) drew in defense-focused VC Helantic for AI satellite monitoring of grids, rail and pipelines.

The clearest single signal was the EU Innovation Fund’s first dedicated industrial-heat auction (IF25), which on May 22 selected 65 projects for ~€400M (~$466M) of grants across ten countries – expected to deliver ~16.3 TWh of decarbonized heat over five years and avoid 6.6 Mt CO₂, displacing more than 1.5 billion m³ of natural gas. Notably, the awards were dominated by mature resistance heating (~77% of projects), with thin representation of heat pumps and solar thermal and no geothermal – a reminder that, even with policy support, industrial heat electrification is still early.

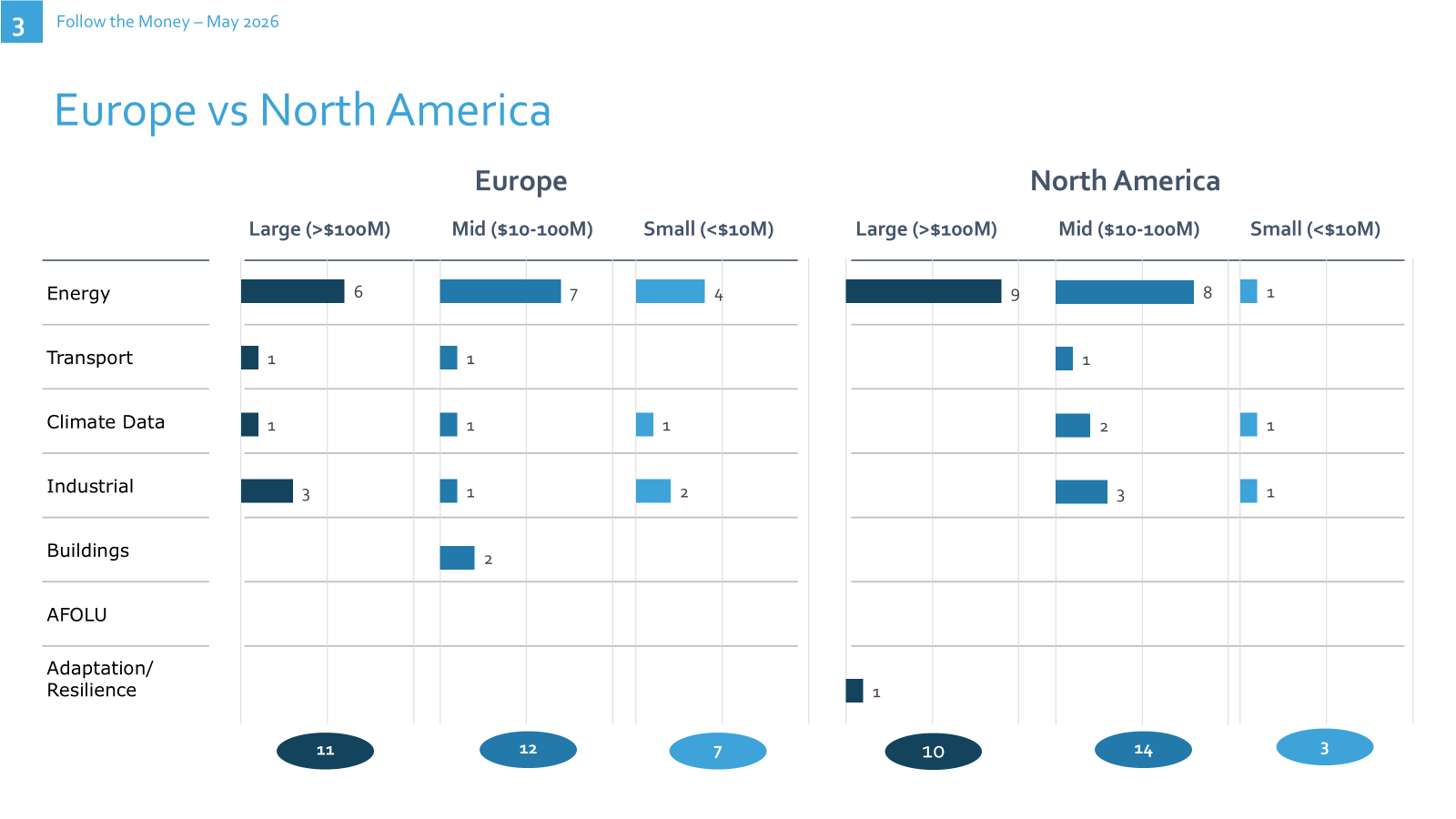

Europe recorded ~$11.4B across 30 deals, leading the month - blending very large public-finance and industrial packages with one of the deepest mid-stage deep-tech layers in the world: carbon-neutral lithium, fusion, flow batteries, natural hydrogen, SAR intelligence and refrigerant-free heat.

The structural anchors were two industrial-decarbonization packages – Germany’s ~$5.9B EU-cleared Carbon Contracts for Difference scheme and Vulcan Energy’s ~$2.4B Lionheart financial close – reinforcing the pattern of European public finance underwriting deployment while private capital concentrates on first-of-a-kind technology. Below them, a wide variety of clean tech investments.

Selected May financings:

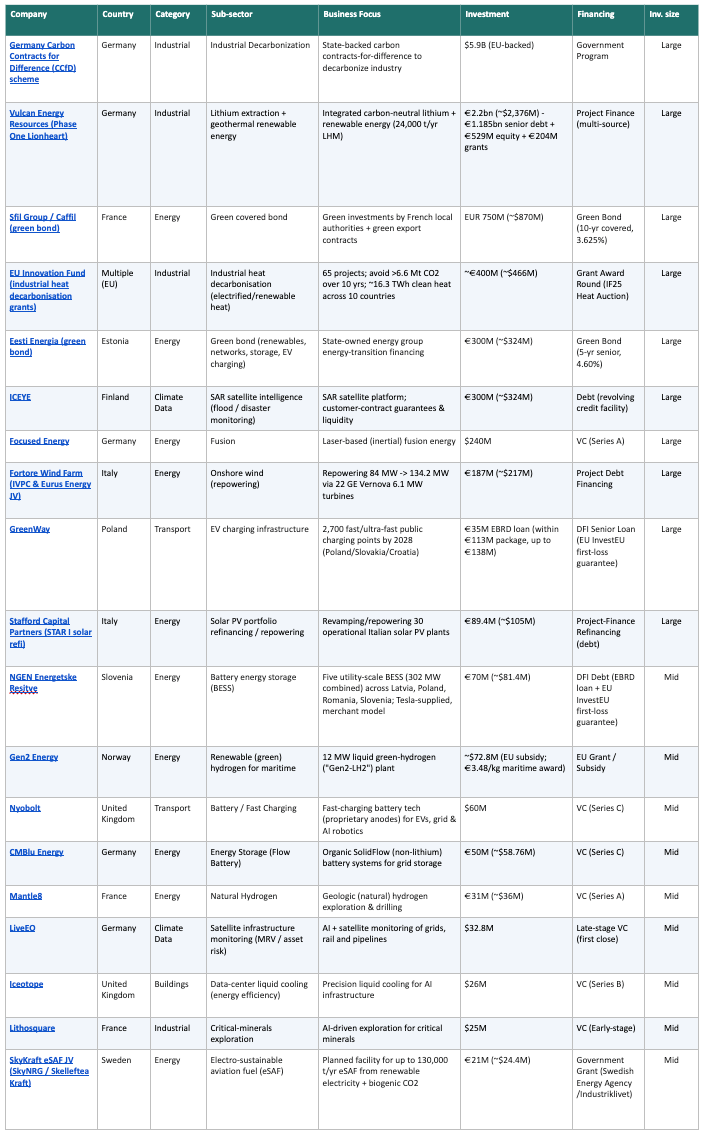

Vulcan Energy Resources (Germany) – ~€2.2B Phase One Lionheart financial close (May 28); integrated carbon-neutral lithium + geothermal energy producing 24,000 t/yr lithium hydroxide (enough for ~500,000 EVs) via proprietary VULSORB direct-lithium-extraction, powered by geothermal brine.

Focused Energy (Germany) – $240M Series A, described as the largest fully-secured fusion Series A to date; utility RWE led and is providing the decommissioned Biblis nuclear site for the “Lighthouse” direct-drive inertial-fusion demonstrator.

ICEYE (Finland) – €300M (~$326M) three-year revolving credit facility (Citi, Danske Bank lead) for the world’s largest SAR satellite constellation; flood/disaster monitoring with a strong defense dual-use.

Nyobolt (UK) – $60M Series C at a $1B valuation (Symbotic lead); niobium-tungsten-oxide anodes charging 0–80% in under five minutes, >20,000 cycles, for robots, humanoids and data-center UPS.

CMBlu Energy (Germany) – ~€50M (~$59M) initial Series C close (Samsung Ventures joining), crossing unicorn status; “SolidFlow” non-lithium organic flow batteries with a 5 GWh Uniper framework.

Mantle8 (France) – €31M Series A (Sandwater lead, with Breakthrough Energy Ventures); proprietary 4D subsurface imaging to locate high-purity natural (geologic) hydrogen at modeled costs as low as €0.80/kg.

Iceotope (UK) – $26M Series B (Two Seas Capital, Barclays Climate Ventures); chassis-based precision liquid cooling cutting data-center power up to 40% and water up to 96%.

Lithosquare (France) – $25M seed (World Fund, Kindred Capital co-lead); a “geology AI” foundation model accelerating discovery of copper, lithium and rare earths up to 10x.

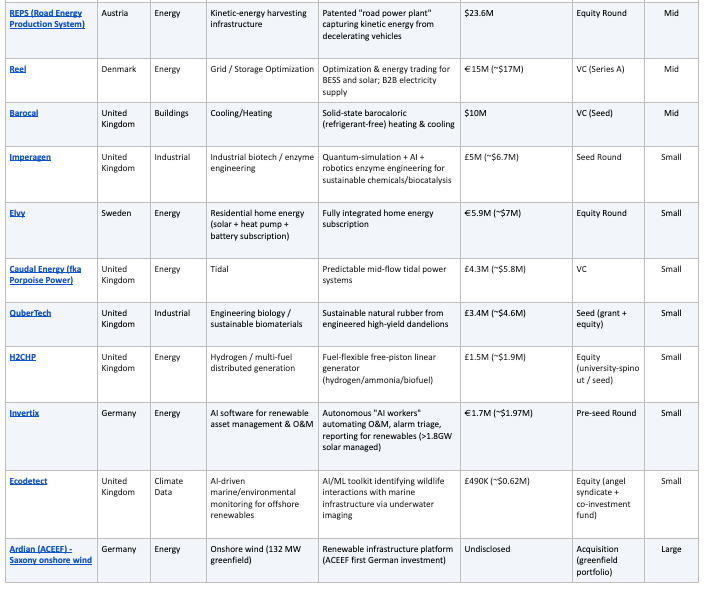

REPS (Austria) – ~$24M for a magnet-based “road power plant” harvesting kinetic energy from decelerating vehicles, live at the Port of Hamburg.

Barocal (UK) – $10M seed (World Fund, Breakthrough Energy Discovery); refrigerant-free solid-state barocaloric heating and cooling, a Cambridge spinout.

GreenWay (Poland) – ~$131M EBRD senior loan (EU InvestEU first-loss guarantee) to build 2,700 fast and ultra-fast public charging points across Poland, Slovakia and Croatia by 2028.

Stafford Capital Partners (STAR I) (Italy) – ~$105M project-finance refinancing (with BPER) to revamp and repower a 30-plant operational Italian solar PV portfolio.

SkyKraft eSAF JV (Sweden) – ~$24M Swedish Energy Agency / Industriklivet grant to SkyNRG and Skellefteå Kraft for a planned facility producing up to 130,000 t/yr of electro-SAF from renewable electricity and biogenic CO₂.

Reel (Denmark) – ~$18M Series A; optimization and energy trading for batteries and solar plus B2B clean-electricity supply.

Elvy (Sweden) – ~$7M equity (atop a €500M credit facility) for a fully integrated residential solar + heat-pump + battery energy subscription.

Imperagen (UK) – ~$7M seed; quantum-simulation + AI + robotics enzyme engineering for sustainable chemicals and biocatalysis.

Caudal Energy (UK, formerly Porpoise Power) – ~$6M for predictable mid-flow tidal power systems inspired by marine-mammal locomotion.

Invertix (Germany) – ~$2M pre-seed; autonomous “AI workers” automating O&M, alarm triage and reporting across >1.8 GW of managed solar.

Ecodetect (UK) – ~$1M angel/co-investment; an AI/ML underwater-imaging toolkit identifying wildlife interactions with offshore-renewables infrastructure.

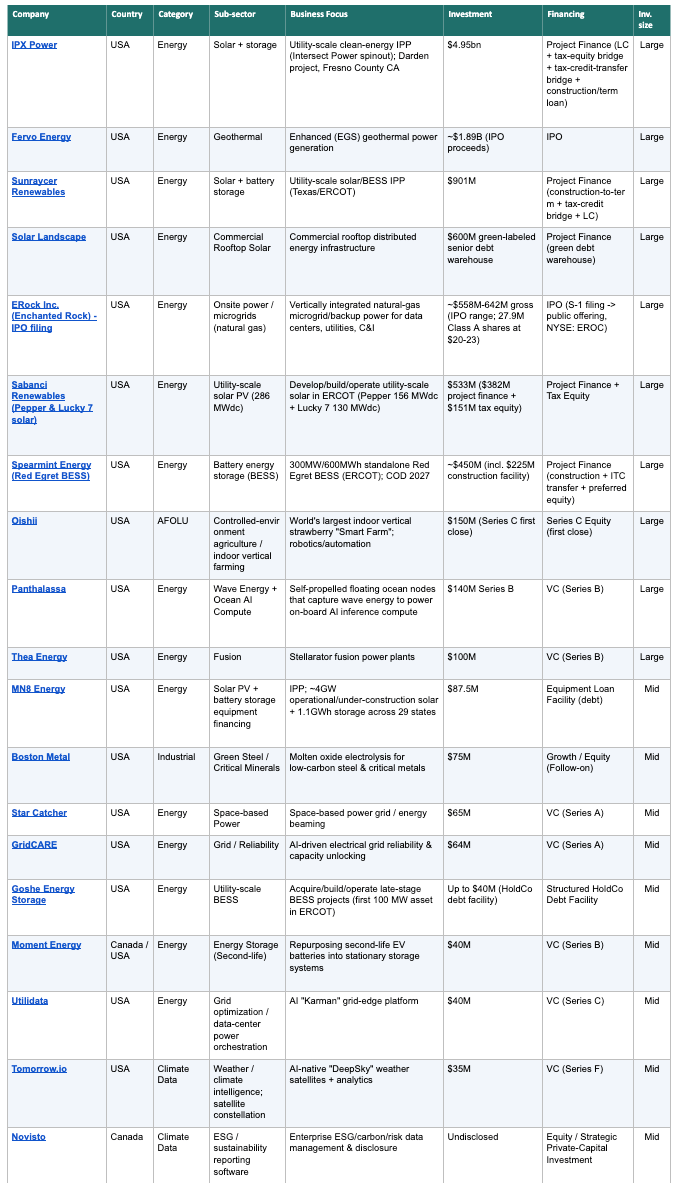

North America recorded ~$10.9B across 27 deals - the sharpest thematic concentration of the month. The defining narrative is now unmistakable: the U.S. is buying firm, dispatchable power and the infrastructure to feed AI - geothermal, fusion, gas microgrids, grid-capacity software and critical materials - at a pace and conviction no other region matches.

Selected highlights:

Fervo Energy (USA) – ~$1.89B IPO (rising to ~$2.17B with the over-allotment), priced above range at $27/share on Nasdaq (FRVO) – Wall Street’s largest clean-energy IPO ever; enhanced geothermal (EGS) baseload backed by a Google framework for up to 3 GW and a ~$7.2B contracted-revenue backlog.

IPX Power / Darden (USA) – $4.95B construction financing for up to 1.15 GWac solar + 4.6 GWh storage in Fresno County, CA; the utility-scale spinout of Intersect Power following Google’s $4.75B acquisition.

Panthalassa (USA) – $140M Series B (Peter Thiel’s Founders Fund lead); self-propelled floating ocean nodes that capture wave energy and run AI inference onboard, cooled by seawater.

Thea Energy (USA) – $100M Series B (Thomas Tull’s USIT lead); a software-shaped “planar coil” stellarator replacing complex 3D magnets with mass-manufacturable flat arrays.

Boston Metal (USA) – $75M growth round with new strategic investor Tata Steel; molten oxide electrolysis for low-carbon steel and critical metals, now pivoting near-term to niobium, tantalum and vanadium.

Star Catcher (USA) – $65M Series A (B Capital lead); an orbital power grid that beams concentrated sunlight via optical power beaming to client satellites’ existing panels – a clear climate + defense dual-use.

GridCARE (USA) – $64M Series A (Sutter Hill Ventures lead); physics-based AI that finds latent grid capacity and compresses data-center interconnection from years to months.

Utilidata (USA) – $40M Series C extension completing a $100M round; the NVIDIA-based “Karman” platform embedded at the data-center rack to unlock stranded power capacity.

Enchanted Rock (ERock) (USA) – ~$600M IPO filing (NYSE: EROC) on a ~$1.3B data-center backlog; low-emission natural-gas microgrids as bridge-to-power amid interconnection delays (a speed-to-power, not zero-carbon, play).

Magrathea (USA) – $24M Series A; carbon-neutral magnesium from seawater via next-generation molten-salt electrolysis, a DoD-backed defense-critical “gateway metal.”

CREW Carbon (USA) – $25M Series A ($19M equity + $6M grant; Burnt Island Ventures lead); wastewater alkalinity enhancement permanently converting CO₂ to bicarbonate, a Yale spinout with >$33M of offtake.

Moment Energy (Canada/USA) – $40M Series B; repurposing second-life EV batteries into UL-certified stationary storage systems.

Novisto (Canada) – ~$27M strategic investment (La Caisse) for enterprise ESG, carbon and risk data management and disclosure software.

Aboard (USA) – ~$13M Pre-Series A; a next-generation electric recreational-vehicle / travel-trailer manufacturer.

Shatterdome Energy (USA) – ~$4M pre-seed; an AI-powered energy-trading and virtual-power-plant platform aggregating renewables, storage and flexible demand..

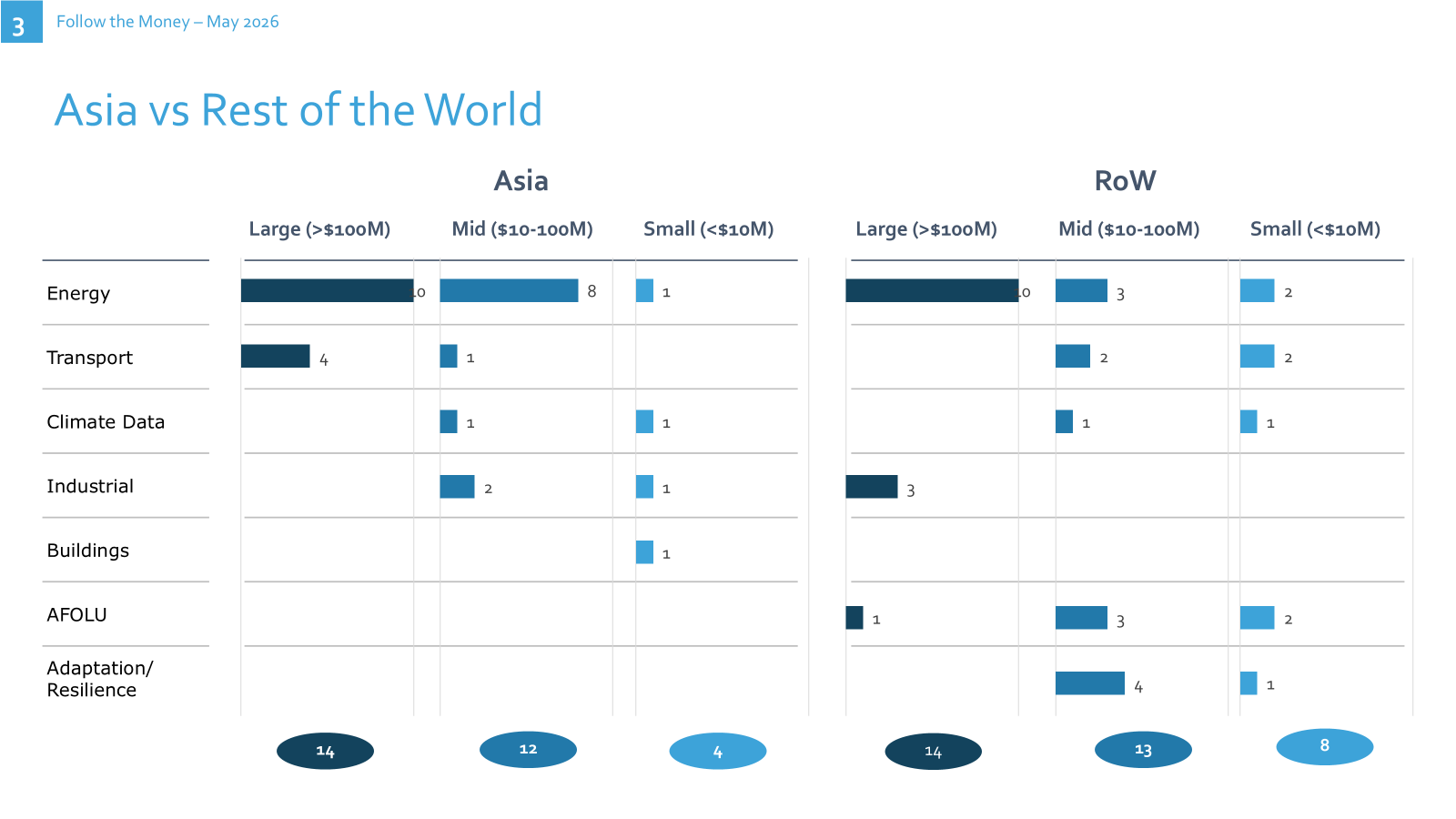

Asia-Pacific recorded ~$5.0B across 30 deals, with China anchoring battery, truck and grid rounds and India dominating renewables, hydropower and the green-financing long tail.

Key highlights from Asia:

HKSAR Government (Hong Kong) – ~$817M green-bond tranche (an €750M 8-year piece) financing eligible green and infrastructure projects.

Pentagreen Capital (Singapore) – ~$800M second close of its blended Green Investments Partnership for sustainable infrastructure across South and Southeast Asia.

CleanMax (India) – ~$575M project finance (ECB + FCNR(B) + INR facilities) for ~1 GW of C&I solar and wind across Rajasthan and Karnataka; Apple separately took a ~$12M stake supporting >150 MW.

Dorjilung Hydropower (Bhutan) – ~$515M World Bank / Tata Power development of a 1,125 MW hydropower scheme.

Zeron (Jiangsu Zero One Auto) (China) – $200M Series B2 (Temasek, Zijin Mining); vertically-integrated autonomous electric heavy trucks for mining and industrial logistics.

Sunwoda Power / EVB (China) – ~RMB 1.68B (~$228M) Series C capital increase; EV power batteries and storage expanding into solid-state, sodium-ion and AI data-center backup, ahead of a Hong Kong IPO.

Ola Electric (India) – ~$209M intra-group infusion to localize EV and Li-ion cell production.

Zaihe Truck (China) – ~$140M cumulative financing (Baidu Ventures, Horizon Robotics); AI-defined new-energy heavy trucks including a ~1,500 km hydrogen-electric flagship.

Zhibang Lithium (China) – ~RMB 500M (~$74M) Series A (backed by the Nongfu Spring founder’s Yangshengtang); solid-state battery electrolyte materials with an 11,000 t/yr project near production.

TransFuture Aviation (China) – ~$15M Pre-A+ for a tilt-rotor passenger eVTOL with autonomous takeoff and landing.

Tuoshen Technology (China) – ~$40M D round; an AI current-signature platform for user-side electricity safety, energy management and new-energy device monitoring.

Stride (Vietnam) – ~$15M Series B for a rooftop solar and storage financing platform.

Ecofy (Mirova facility) (India) – ~$15M impact/DFI-style loan from Mirova; a green-only NBFC lending for rooftop solar and EVs.

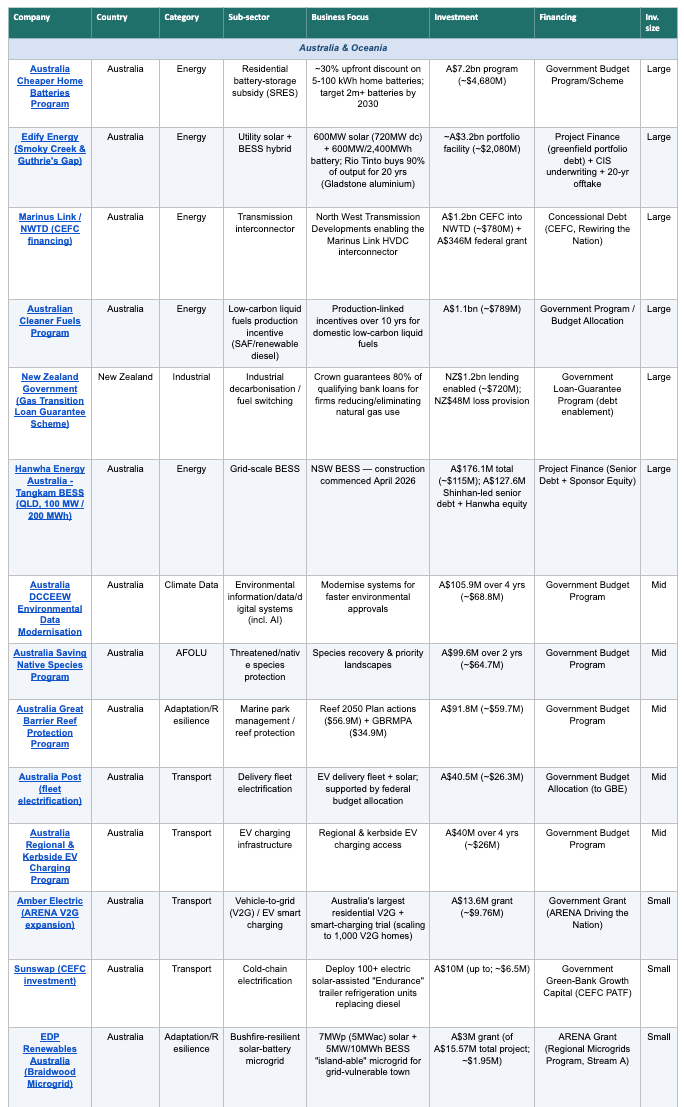

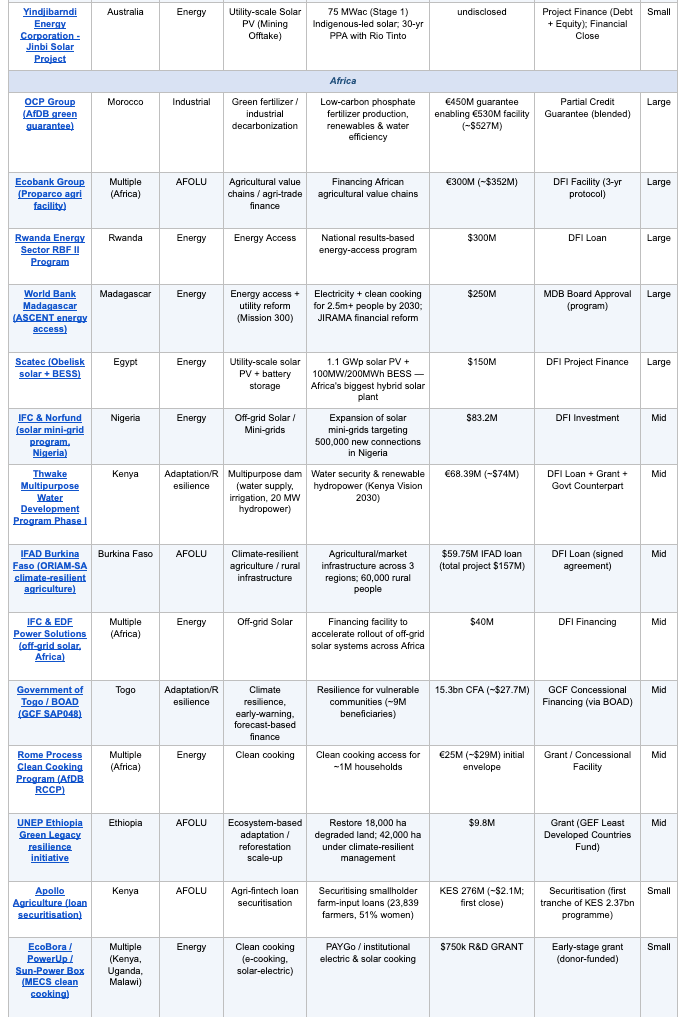

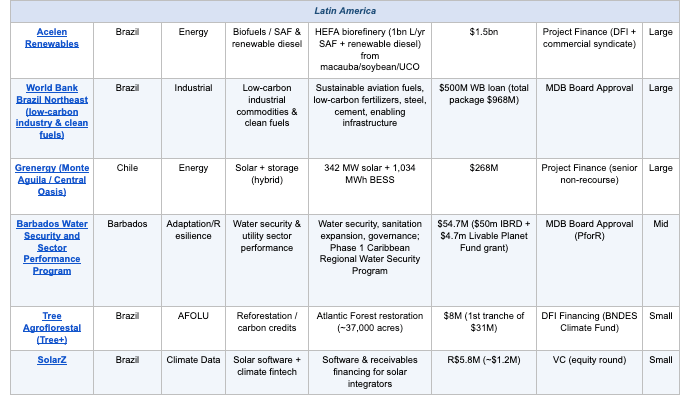

RoW (Africa, Latin America, Oceania) recorded ~$13.6B combined across 35 deals. Australia led at ~$9.4B (15 deals - heavily Australian government programs), followed by Latin America (~$2.3B, 6 deals) and Africa (~$1.9B, 14 deals). As in prior editions, the picture across these markets remains anchored by government programs, MDB and DFI interventions and blended-finance structures, while commercial private capital stays comparatively concentrated in a few large project closes.

Selected highlights:

Australia Cheaper Home Batteries Program (Australia) – ~A$7.2bn (~$4.68B) residential battery-subsidy program targeting 2m+ home batteries by 2030 (a program, not a single transaction).

Edify Energy (Australia) – ~$2.08B financial close on the Smoky Creek & Guthrie’s Gap hybrid (600 MW solar + 600 MW/2,400 MWh battery), with Rio Tinto buying 90% of output for 20 years to power Gladstone aluminium.

Acelen Renewables (Brazil) – ~$1.5B HEFA biorefinery financing (HSBC + IFC lead, deep DFI syndicate) for 1 billion L/yr of SAF and renewable diesel from macaúba, soybean and used cooking oil.

Marinus Link / NWTD (Australia) – ~$780M CEFC concessional financing for the North West Transmission Developments enabling the Marinus Link HVDC interconnector.

Sunswap (Australia) – ~$7M CEFC growth capital to deploy 100+ electric, solar-assisted “Endurance” trailer refrigeration units replacing diesel in cold-chain fleets.

OCP Group (Morocco) – ~€450M (~$489M) AfDB partial credit guarantee unlocking up to €530M of green financing for low-carbon phosphate fertilizer, renewables and desalination.

Grenergy (Oasis) (Chile) – ~$268M senior non-recourse project finance for 342 MW solar + 1,034 MWh of storage under a daytime PPA.

Scatec (Obelisk) (Egypt) – ~$150M EIB tranche within a ~$479M DFI package for Africa’s biggest hybrid plant (1.1 GWp solar + 100 MW/200 MWh BESS), first phase commissioned February 2026.

Apollo Agriculture (Kenya) – first close of Kenya’s first private-sector smallholder-ag securitisation (~KES 276M of a ~KES 2.37B program), underwritten with satellite imagery and ML yield models.

Tree+ (Tree Agroflorestal) (Brazil) – ~$8M BNDES Climate Fund tranche to restore ~37,000 acres of Atlantic Forest and develop carbon credits.

UNEP Ethiopia Green Legacy (Ethiopia) – $9.8M GEF-funded reforestation and ecosystem-based adaptation across 67,000+ hectares, benefiting 423,000+ people.

At ~$41B, May proved that April’s $55B was a spike rather than a new baseline - but the structure we have tracked all year held and, if anything, sharpened: firm, capital-heavy power in the U.S.; mass-market and utility-scale electrification across Asia and Oceania; policy-backed project finance and deep tech in Europe; and blended adaptation and nature finance across the Global South.

The cleanest signal of the month was that climate capital is increasingly AI-energy capital. Whether the next month sees fusion and geothermal raises keep climbing while solar-plus-storage project finance broadens will tell us whether the “firm-power premium” is a durable structural feature or a 2026 moment. We will be watching whether the themes identified in December continue to deepen:

U.S.: Nuclear and Geothermal vs. Rest of World: Solar and Wind

“Solarpunk” Momentum - electrification beyond cars, powered by cheap batteries

Dual-Use Innovation: Climate + Defense, Supply Chain, Compute

CapEx-Intensive Mid-Stage Tech and the “Valley of Death”

Industrial Heat Electrification

Nature-Based Solutions for Carbon and Biodiversity

AFOLU Innovation - including climate adaptation, robotics, and alternative proteins

The Rise of Climate Robotics

Stay tuned for next month’s edition as we continue to follow the capital shaping the climate transition.