👋 Welcome to Climate Drift: your cheat-sheet to climate. Each edition breaks down real solutions, hard numbers, and career moves for operators, founders, and investors who want impact. For more: Community | Accelerator | Open Climate Firesides | Deep Dives

Hey there! 👋

Skander here.

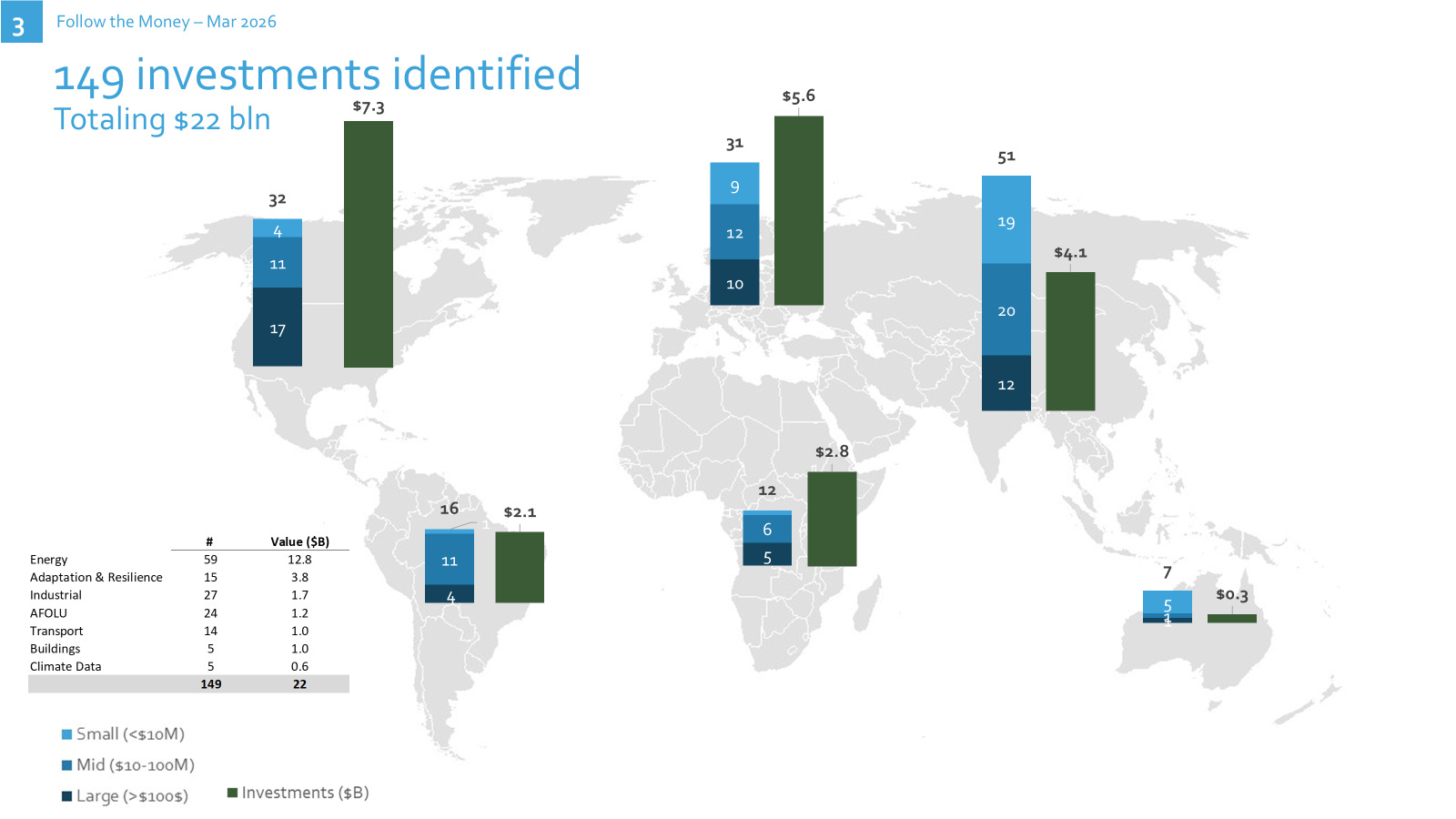

$22 billion across 149 deals. March 2026 was the biggest month we’ve tracked this year.

Jarek’s latest Follow the Money breaks down where the capital actually went, and the regional splits tell you more than any macro forecast could.

🇺🇸 North America: $7.3B, almost entirely concentrated in batteries, nuclear, and geothermal. The U.S. is buying firm, dispatchable power for AI infrastructure. Valar Atomics ($450M), Fervo Energy ($421M), and a string of utility-scale BESS financings made that case loud and clear.

🇪🇺 Europe: $5.6B across 31 deals, anchored by Nscale’s $2B raise and the Andalusian Green Hydrogen Valley reaching FID. But the real signal is the mid-layer: iron fuel (RIFT), SMRs for district heating (Calogena), gene-edited bananas (Tropic), precision fermentation (Standing Ovation). Europe’s deep tech pipeline is producing first-of-a-kind closes.

🌏 Asia: $4.1B but 51 deals, the highest count of any region. China dominated the large rounds (Galaxy Universal Robotics at $344M, Zeron at $165M), India filled the mid and small layer with EV, solar, and climate fintech.

A few patterns worth flagging: AI-enabled climate solutions showed up in 15 separate raises. Robotics got its own tracking category for the first time, with five investments, mostly in China. And AFOLU had its strongest month of the quarter, led by Halter doubling its valuation to $2B.

🌊 Jarek breaks it all down below, region by region, theme by theme.

But first: Who is Jarek?

Jarek Dmowski is a global transformation leader who partners with high-growth companies with positive climate impact. He combines industry and climate finance expertise with a strong track record of driving growth—across PE/VC-backed scaleups, ABN AMRO, and BCG.

He scaled a data-driven technology company ~2.5x to ~$25M in revenue and led post-merger integrations that enabled ~6x accelerated growth. At a global financial institution, he spearheaded a $2B capital reallocation toward new energy and mobility. He also developed a comprehensive climate plan that translated the Paris Agreement into actionable targets across sectors and established a $250M program to drive efficiency gains and reduce emissions at an energy utility.

Jarek is passionate about how the climate transition reshapes economies and business models, creating significant opportunities for multi-country growth and impact.

Welcome to the next edition of “Follow the Money” - a monthly briefing on the capital flows shaping the climate transition.

March wrapped up a busy Q1, and the first quarter of 2026 is officially in the books. We tracked 149 climate-related investment deals totaling ~$22.0 billion in March - marking the highest monthly volume we have recorded so far this year.

Explanation of the approach and source data: The investment list was developed based on disclosures, newsletter monitoring and review of climate news. Although not exhaustive, 149 climate-related investment deals were tracked-amounting to roughly $22 billion (all data in US$), covering all continents and different life stages of companies and development finance programs. Data skew toward early-stage companies and investments, as well as development financing programs. We are continuously working to expand the data sources and coverage of investments.

So, where did the money flow in March 2026?

Regional distribution was led by North America with ~$7.3B across 32 deals, followed closely by Europe (~$5.6B, 31 deals) and Asia (~$4.1B, 51 deals - the highest deal count by far)

Energy continues to dominate, accounting for ~$13 billion across 59 deals - by far the largest category month after month. Adaptation & resilience emerged as a clear #2 (~$3.8 billion, 15 deals), followed by Industrial, Transport, and AFOLU. Buildings and Climate Data remained undercapitalized (~$0.1B).

AI’s influence is becoming structural. Fifteen AI-enabled climate solutions raised capital in March, reinforcing the role of artificial intelligence as an accelerator of deployment, optimization, and cost reduction across sectors.

Robotics, a new tracked category, saw five investments in March, particularly in China, underscoring its growing industrial and climate-adaptation roles.

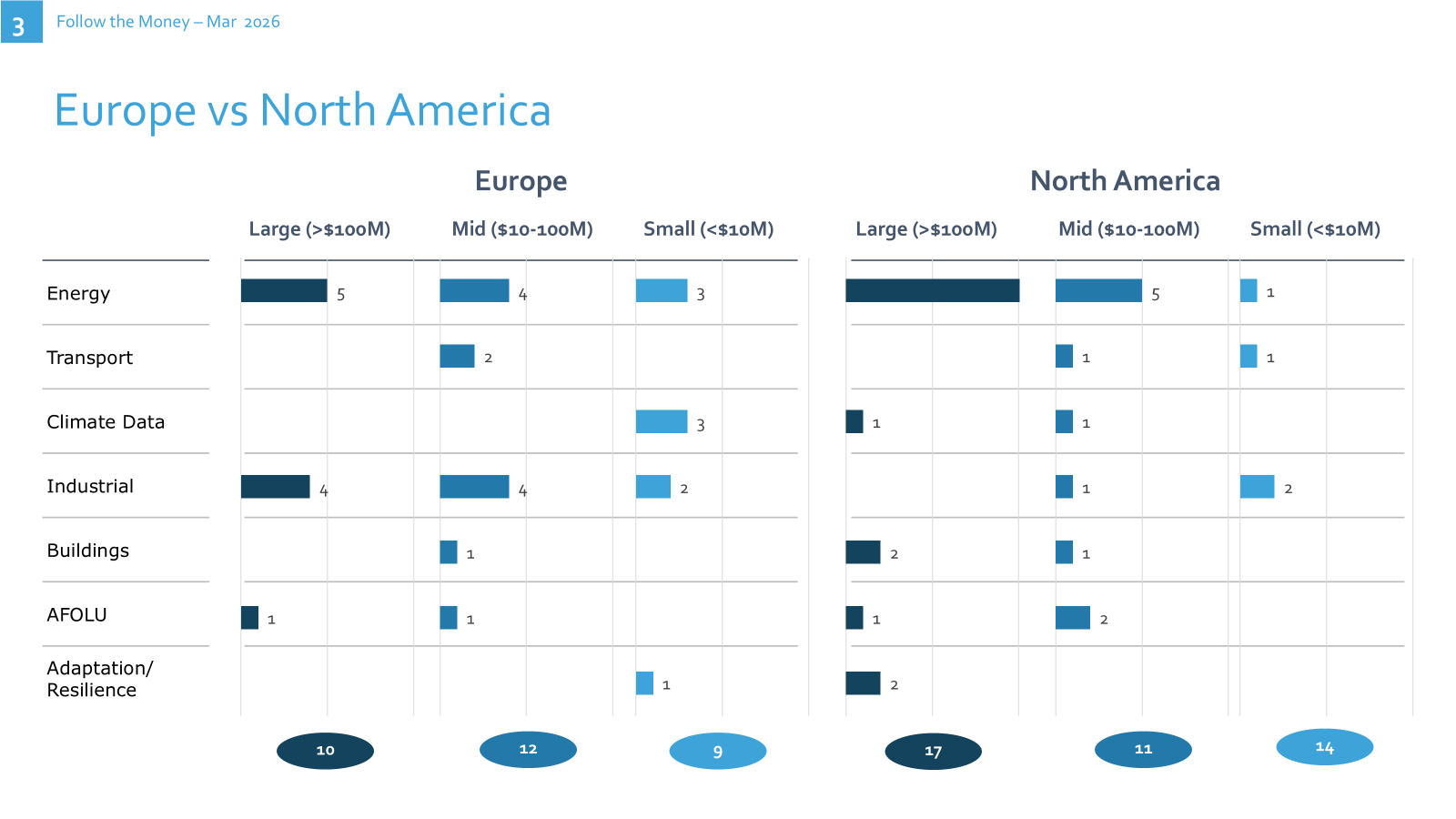

Venture capital activity remained strong. We tracked 57 venture and growth investments (Seed through Series F), with an average round size of ~$92 million. Asia led with 24 deals, followed by Europe and North America with 17 and 13 deals, respectively.

Public and development finance continued to anchor the market. Multilateral institutions and government programs supported ~$6.8 billion across ~33 deals, with a strong focus on infrastructure and adaptation.

Let’s now dive deeper into 2026 watchlist themes (please refer to our December perspective for more details) and across regions to highlight technologies with real scaling potential over the next 3-5 years.

Which (of our 2026) themes were most strongly visible in March?

U.S: Nuclear and Geothermal vs. RoW: Solar and Wind

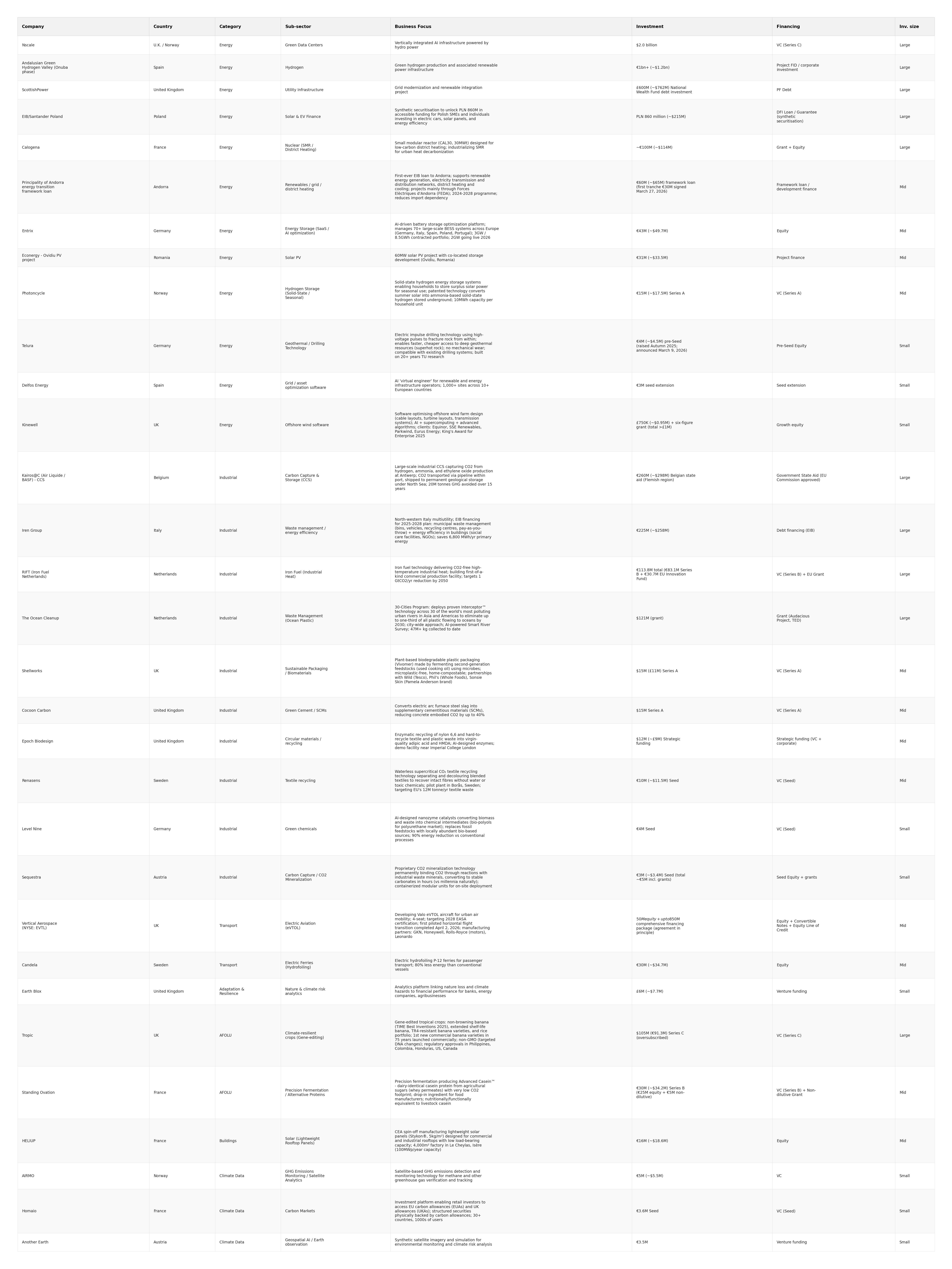

March continued to support this theme. In the U.S., the two largest non-project-finance cleantech equity rounds of the month were Valar Atomics ($450M advanced nuclear) and Fervo Energy ($421M enhanced geothermal), while solar and BESS also attracted financing (Primergy/Quinbrook and Zelstra projects). Outside the U.S., the biggest renewable cheques were EIB Sub-Saharan Africa ($1.15B), Envision Energy ($600M SLL, wind/storage), Clean Max Enviro ($364M solar+wind IPO, India), and ACEN Corp India ($81M onshore wind).

Not a single non-U.S. advanced-nuclear or geothermal round of similar scale. The pattern is structural now: the U.S. is paying up for firm, dispatchable, capital-heavy electrons to run AI factories; everyone else is paying down for the cheapest levelized-cost MWh they can build.

“Solarpunk” Continues

March was a strong month for “EV beyond cars.” Allfleet/PMI Electro ($310M, India, buses) and Zeron ($165M, China, heavy trucks) anchored the commercial-vehicle layer; Euler Motors ($77M, India, 3-/4-wheel last-mile) continued to scale; Candela ($34.7M, Sweden, hydrofoiling ferries), Vertical Aerospace ($50M immediate, UK, eVTOL), Arc ($50M, USA, electric marine), Zeno ($25M, Kenya, e-motorcycles) and Battery Smart ($7.4M, India, 2W/3W swapping) covered water, air and two-wheel mobility.

On the residential side, cheap batteries and electrification kits kept scaling - Photoncycle ($17.5M, Norway, seasonal H₂ storage for households), HELIUP ($18.6M, France, lightweight rooftop solar), Ecofy ($42M, India, green NBFC lending for rooftop and EVs), and GSIS Ginhawa Solar ($218M, Philippines, sovereign rooftop-solar loan pool).

March 2026 highlighted several capital structures successfully navigating this perilous valley. The key to unlocking capital for TRL 4-5 technologies lies in securing advanced offtake agreements and intelligently blending non-dilutive government grants with private equity. RIFT’s €113.8 million raise for its iron fuel technology was heavily anchored by a €30.7 million grant from the EU Innovation Fund, which de-risk the subsequent private capital injection from regional development funds and impact investors. Fervo Cape Station ($421M non-recourse project finance) was the first enhanced-geothermal facility to reach utility-scale project financing. Electra, developing a low-temperature electrochemical process for manufacturing green iron, successfully utilized a $30 million venture debt facility from J.P. Morgan.

AFOLU had its strongest month of Q1. Halter ($220M, New Zealand, AI virtual fencing) doubled its valuation to $2B. Tropic ($105M, UK, gene-edited bananas) anchored climate-resilient crops. TARGAN ($100M, USA, poultry AI) and Captain Fresh ($31M, India, seafood) covered animal-protein productivity. Standing Ovation ($34.2M, France, casein) was one of the cleaner alt-protein closes of the year. PlasmaLeap ($20M, Australia, plasma ammonia, Gates Foundation + Yara + Investible), Solugen ($50M, Canada, manure-to-fertilizer) and Sistema.bio FarmCarbon ($53M, Global) extended the smallholder-and-circular-fertilizer stack.

In March 2026, massive capital inflows poured into (mostly) the Chinese robotics ecosystem. We tracked Galaxy Universal Robotics ($344M, CATL battery-factory humanoids), Robot Era ($138M, humanoid L7), Kunwei ($13.8M, force sensors for humanoids), AgriPass ($7.5M, Israel, weed-control robotics) and Skye Air ($9M, India, BVLOS delivery drones). In many cases, the climate value-add is indirect - higher-velocity clean-manufacturing throughput, less labour-constrained.

Europe recorded ~$5.6B across 31 deals in March 2026, blending two mega-deals (Nscale, Andalusian Green H₂ Valley) with a deep, mid-sized layer of first-of-a-kind deep-tech - iron fuel, SMRs, lightweight solar, seasonal hydrogen storage, precision fermentation, gene-edited crops.

Selected March financings:

Nscale (UK / Norway) - $2.0B Series C led by Aker ASA. Hydro-powered AI hyperscaler; board adds Sheryl Sandberg and Nick Clegg. $14.6B valuation. This is Europe’s most ambitious answer to the U.S. data-center build-out - and the first pure-play European AI hyperscaler that looks investable at scale.

Andalusian Green Hydrogen Valley (Onuba phase) (Spain) - €1B+ (~$1.2B) FID. Moeve, Masdar and Enalter confirmed the first-phase construction of the Huelva green H₂ corridor - one of a handful of European mega-projects actually reaching FID rather than slipping.

RIFT (Iron Fuel Netherlands) (Netherlands) - €113.8M (~$131M) (€83.1M Series B led by PGGM + €30.7M EU Innovation Fund). World’s first commercial iron-fuel facility for industrial heat - zero-CO₂ high-temperature process heat by burning iron powder and regenerating it with clean electricity. If this works at FOAK scale, it rewrites the playbook for decarbonizing heavy industry.

Calogena (France) - ~€100M (~$114M) combining a €48M France 2030 grant with private equity from Groupe Gorgé, SNEF and Banque des Territoires. 30MWt SMR purpose-built for district heating rather than power - a smart design choice that dodges the levelized-cost-of-electricity fight entirely.

Tropic (UK) - $105M Series C co-led by Forbion Bioeconomy Fund and Corteva Catalyst, with Just Climate and Temasek alongside. Gene-edited non-browning, TR4-resistant bananas - the first new commercial banana variety in 75 years, and a template for climate-resilient staple crops.

Candela (Sweden) - €30M (~$34.7M). Electric hydrofoiling P-12 ferries consuming 80% less energy than conventional vessels; IFC joining with €8M. Funds a second manufacturing facility in Poland. 65+ vessels on order.

Standing Ovation (France) - €30M (~$34.2M) Series B co-led by Bpifrance’s Ecotechnologies 2 and Crédit Mutuel Innovation. Precision-fermentation casein - dairy-identical protein with a much lower CO₂ footprint.

North America recorded ~$6.8B across 31 deals - the largest regional dollar total - driven by a tight cluster of themes: utility-scale batteries, advanced nuclear, geothermal, and the AI-data-center-power stack.

Selected highlights:

Ayar Labs (USA) - $500M Series E led by Neuberger Berman with ARK Invest, Insight Partners, QIA, Sequoia Global Equities, AMD Ventures and NVIDIA alongside. Co-packaged optics that drastically cut energy per bit in AI data-center interconnects. Valuation: $3.75B. The round that finally puts the “data-center power bottleneck” thesis into the mega-round bucket.

Valar Atomics (USA) - ~$450M ($340M equity + $110M debt). Clusters of small high-temperature gas-cooled reactors for AI data-center firm power. Backed by Palmer Luckey (Anduril founder), Shyam Sankar (Palantir CTO) and Snowpoint Ventures. $2B valuation. This is the advanced-nuclear-meets-defense-tech archetype crystalizing into a category.

Fervo Energy - Cape Station Phase 1 (USA) - $421M non-recourse project finance arranged by RBC. 100MW enhanced geothermal scaling to 500MW; PPAs with Southern California Edison, Shell Energy and California CCAs. First EGS facility to actually reach utility-scale project financing - a milestone, not a demo.

EnerVenue (USA) - $300M Series B extension led by Full Vision Capital. Metal-hydrogen battery storage - 30,000-cycle lifespan, no degradation. Funds manufacturing scale-up in the U.S. and Changzhou, China. A credible LDES contender that Li-ion can’t easily match on durability.

Frore Systems (USA) - $143M Series D at a $1.64B valuation. AirJet thermal chips cooling AI accelerators and edge devices - another “thermal stack” bet riding the AI power-density curve.

TARGAN (USA) - $100M committed facility ($30M initial tranche) from Symbiotic Capital. AI-powered feather-sex identification for poultry hatcheries at 30M+ chicks/week - an unglamorous but measurably emissions-reducing bit of animal-protein infrastructure.

Cultivo (USA) - $60M capital-deployment partnership with Octopus Energy Generation (total partnership $100M). Nature-based carbon removal across 650,000+ acres of regenerated grasslands; targeting 9M tCO₂ removal over 30 years. One of the cleanest corporate off-take structures we’ve seen in the NbS space.

Asia-Pacific recorded ~$4.3B across 59 deals - by far the highest deal count of any region, with China anchoring the large deep-tech rounds and India dominating the mid/small layer through EV, solar and climate fintech.

Key highlights from Asia in March:

Clean Max Enviro Energy Solutions (India) - ₹3,100 crore (~$364M) IPO. India’s largest C&I renewables platform (2.54 GW operational, 531+ corporate customers). A cleaner proxy than ReNew for the underlying Indian C&I demand curve.

Galaxy Universal Robotics (China) - RMB 2.5B (~$344M) growth round with the National AI Fund (Phase III) making its first embodied-AI investment. Galbot S1 humanoids now operational inside CATL battery factories. Climate relevance: clean-energy manufacturing productivity.

Allfleet (PMI Electro) (India) - up to $310M growth equity from KKR (Global Climate Transition Strategy). Platform to deploy 5,000+ electric buses across India - KKR GCT’s first India investment and one of the largest emerging-market e-bus deals on record.

Zeron (China) - RMB 1.2B (~$165M) growth round co-led by NIO Capital. Electric heavy-duty trucks for long-haul - the “Tesla Semi” thesis, Chinese-flavored.

Robot Era (ROBOTERA) (China) - RMB 1B (~$138M) strategic round. L7 bipedal humanoid + direct-drive dexterous hand. 50% of orders from international markets; valuation >RMB 10B.

Dali Times Energy (China) - RMB 1B+ (~$116M) project investment. Wide-temperature-range, high-C-rate specialised lithium and semi-solid-state / solid-state battery production base. 2 GWh of planned annual capacity. Yunnan’s 2026 priority project.

Vertical Aerospace (UK-listed, covered here for Asia-relevance as the eVTOL category leader) - $50M immediate equity + up to $850M financing package. Valo eVTOL aircraft for urban air mobility - first piloted horizontal flight transition completed April 2, 2026.

Euler Motors (India) - INR 437.5 Cr (~$47M) Series E equity + INR 250 Cr (~$30M) debt. Electric 3- and 4-wheel commercial vehicles for last-mile logistics. 15,000+ vehicles on road. Lightrock and Hero MotoCorp lead.

RoW (Africa, South America, Australia) recorded ~$6.2B combined across 35 deals - roughly a quarter of March’s total volume. Across South America, Africa, and other emerging markets, the investment landscape remains primarily anchored by the interventions of MDBs and DFIs, alongside evolving blended finance mechanisms, while the flow of commercial private capital remains constrained.

Selected highlights:

Uruguay Climate Resilience Program (Uruguay) - $980M DFI loan from CAF. Transformation of vulnerable urban areas and public transport in Montevideo; flood prevention and green mobility. One of CAF’s largest single-country climate commitments of the cycle.

ASCENT-GREEN (GCF FP291) (21 African countries) - $250M. The largest single project approved at GCF B.44. Financing for distributed renewables, clean cooking and productive-use energy across Eastern and Southern Africa.

Investec Green Housing Finance (South Africa) - $200M DFI loan from IFC. 7-year senior unsecured facility supporting EDGE-certified green buildings plus a $3.8M UK-MAGC incentive to offset certification costs. Investec targets £18B (~$24B) in sustainable financing by 2030.

Ecuador Biodiversity Bond (Ecuador) - $120M bond issued by Banco Bolivariano with IFC ($50M), IDB Invest ($50M) and FMO ($20M). First biodiversity-labeled bond in Ecuador, largest in Latin America. Covers productive land use, sustainable marine, forestry and ecotourism.

ATOME Villeta Green H₂ Fertiliser Plant (Paraguay) - up to $95M (EIB tranche of a $420M package). Industrial-scale low-carbon nitrogen fertiliser using green hydrogen - 260,000 tpa CAN. IFC, IDB Invest, FMO and GCF alongside.

Zeno (Kenya) - $25M Series A ($20.5M equity + $4.5M debt) led by Congruent Ventures with Active Impact and Lowercarbon. Full-stack e-motorcycle + battery-swap platform for East Africa. 800+ bikes, 150+ swap stations, 25,000+ waitlist.

Halter (New Zealand) - $220M Series E led by Founders Fund with Blackbird, DCVC, Bond and Bessemer. AI-powered virtual fencing for livestock; $2B valuation, doubled in under a year. A rare climate-agtech unicorn with commercial traction in the U.S.

Q1 set the tone: capital is concentrating around firm power in the U.S., mass-market electrification in Asia, policy-backed project finance and deep-tech in Europe, and blended adaptation finance in the Global South. March did not break the pattern - it reinforced it, and added sharper industrial-heat and robotics signals.

We will be watching whether the themes identified in December continue to deepen:

U.S.: Nuclear and Geothermal vs. Rest of World: Solar and Wind

“Solarpunk” Momentum - electrification beyond cars, powered by cheap batteries

Dual-Use Innovation: Climate + Defense, Supply Chain, Compute

CapEx-Intensive Mid-Stage Tech and the “Valley of Death”

Industrial Heat Electrification

Nature-Based Solutions for Carbon and Biodiversity

AFOLU Innovation - including climate adaptation, robotics, and alternative proteins

The Rise of Climate Robotics

Stay tuned for next month’s edition as we continue to follow the capital shaping the climate transition.