Modern credit risk decisioning software must go beyond static scoring to leverage signals derived from mapping multi-source, multi-table data and up-to-date behavioral data. It must translate complex data patterns into transparent, easily understandable decision rules that risk leaders can analyze and deploy quickly. Using this type of “signal intelligence” allows underwriters to identify portfolio shifts before they become losses.

Auto lenders rely heavily on a combination of quarterly credit bureau refreshes, FICO scores, and in-house scoring and prediction risk models to clear originations. At the same time, operational shifts like dealer-driven income inflation or subtle combinations of payment gaps begin to erode portfolio quality and performance. Lenders have begun to recognize that credit decisioning system can be blind to the subtle yet high-impact risk signals that put pressure on balance sheets.

The impact of even the smallest variables becomes larger as the total volume of loans grows. Considering total industry exposure, the problem is only growing; in fact, according to data from the New York Fed, U.S. auto loan debt reached nearly $ 170 billion in the first quarter of 2026, the largest on record.

To create a safety net in such an environment, risk infrastructure needs to evaluate data across multiple systems and multiple data types simultaneously. Modern credit decisioning platforms must be able to link core loan applications with dealer data, borrower credit histories, and up-to-date market information to identify intersecting variables that reveal subtle but critical signals of applicants’ true debt-service capability.

Signal Intelligence, powered by dotData, addresses this need by providing a strategic front end that converts raw enterprise and bureau data into actionable, system-ready rules. The platform serves as a non-technical risk-strategy workbench for credit executives while operating an automated back-end signal-discovery engine for data scientists. This combination empowers risk leaders to isolate overlooked vulnerabilities without requiring data science teams to manually build new model architectures from scratch.

The value of automating the credit decisioning process becomes greater in large-scale lending business operations. A top-tier non-prime auto lender recently faced severe operational backlogs due to manual analytics processes that took months to complete. By deploying a Signal Intelligence platform, the lender automated the evaluation of raw transactional data to identify thousands of potential predictive signals in a single day. Automating the analytics workflow delivered a 10 ppt predictive lift in their in-house behavioral scoring model, protecting net interest margin.

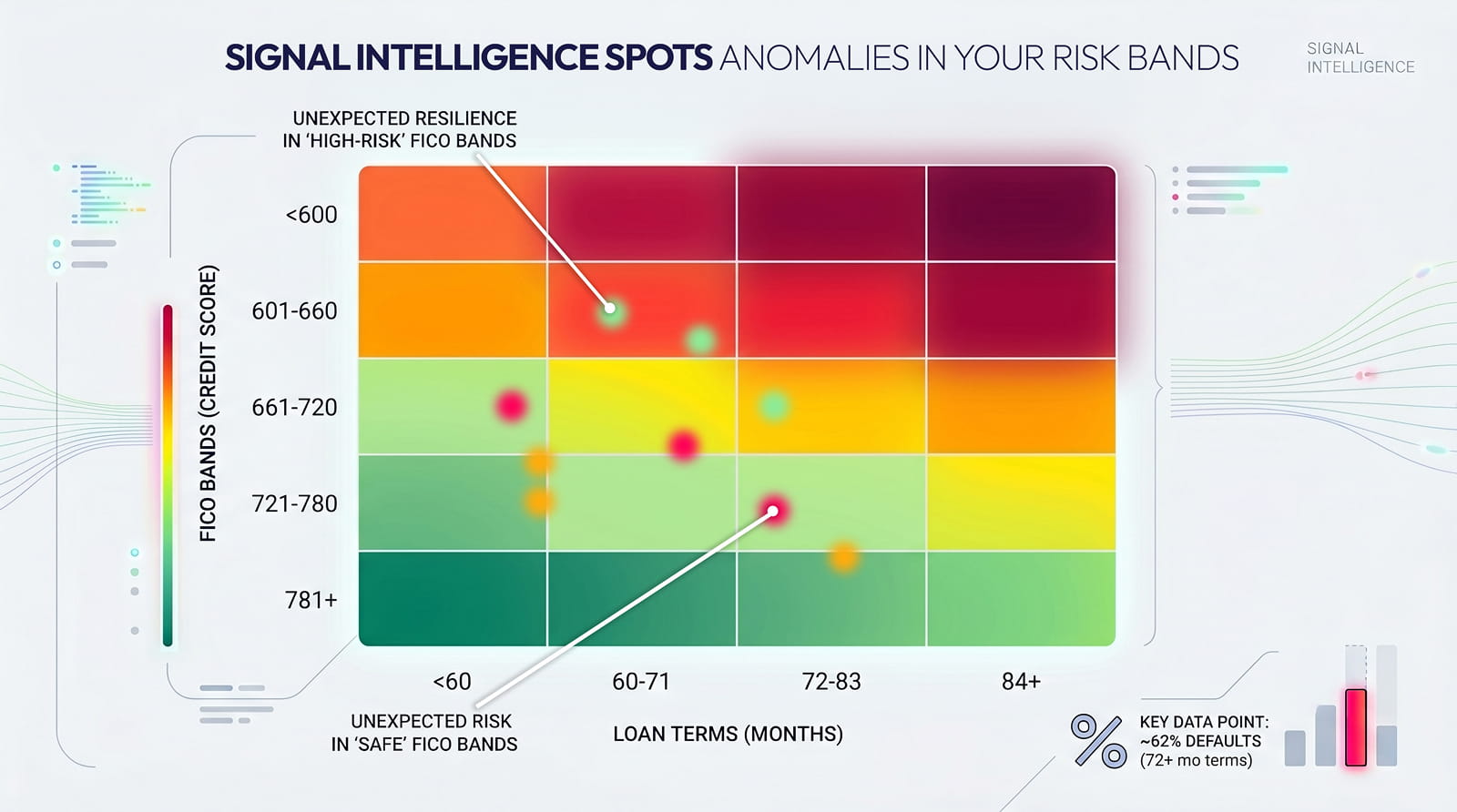

Reducing exposure to early payment default (EPD) risk means shifting from static risk tiers to identifying precise borrower Precision Impact Segments. Lenders need to identify and analyze precise signals of borrower behavior during origination, such as changes in dealer trade-in values and short-term shifts in borrowers’ employment. The granularity achieved with Precision Impact Segments can flag verifiable, repeatable, and scalable default patterns in credit applications before the first missed payment cycle.

An early payment default might be a random act of bad luck, but it might also be the result of a failure of the origination scorecard. When a loan defaults in the first 90 days, the underwriting framework miscalculates the defaulting borrower’s ability to repay the loan. By relying on aggregate credit tiers across varied dealer networks, lenders can leave their portfolios exposed.

According to data from the New York Fed, loan delinquency velocity is not limited to traditional “high risk” tiers. In fact, the share of auto loans moving to serious delinquency (90+ DPD) climbed to 2.97% in Q1 2026, showing that traditional front-end verification practices are insufficient to prevent rising losses.

To reduce exposure to rising loan delinquencies, lenders need to monitor diverse data points from multiple sources to understand how their interactions over specific time frames affect delinquencies. For example, a small change in credit card utilization, combined with additional unverified sources of income for a borrower, may signal financial stress that the lender had not predicted. Traditional credit decision engines often assess such attributes in isolation and miss the complex relationships among them.

Signal Intelligence engines like dotData provide a strategic front end that allows risk leaders to identify and measure specific Precision Impact Segments where EPD risk is concentrated. By identifying complex relationships among signals, such as clusters of recent credit inquiries paired with specific vehicle brands or types, executives can adjust underwriting parameters with high precision to affect only the borrowers in question. These platforms can automate the scanning of disparate data sources and tables, linking data such as customer contact histories, dealer behaviors, and core banking records to find hidden risk signals.

Isolating compound behaviors can yield significant financial benefits. For example, a major captive auto lender conducted a precise analysis of a very specific subset of loans that was experiencing losses outside of predicted limits. By understanding how call frequency, quarterly FICO refreshes, and other negative signals combined, the lender identified a subset of 330 loans that showed a loss rate over 5X higher than predicted, projecting over $6 million in unexpected losses that traditional scoring models had completely missed.

Extended loan terms of 72 months or more can create problems for loss forecasting models by lengthening the period during which the borrower has negative equity, increasing the chances of an acceleration in roll rate velocity. Traditional credit risk decisioning platforms are not equipped to model how unforeseen economic pressures compound over a six to seven-year period, exposing risk teams to increased losses as delayed defaults impact outdated reserve projections.

Consider a borrower with a 72 or 84-month auto loan. A borrower with such a loan is essentially being trusted to maintain a stable financial situation for nearly a decade, even as the vehicle’s value is likely to fall faster than the loan is repaid. When unexpected life events occur or market conditions change, creating gaps in employment or income, lenders can get stuck with an often undetected buildup of loans that can quickly erode capital reserves.

The data, in fact, backs this hypothesis. According to research by LendingTree, borrowers with loan terms of 72 months or longer account for 61.9% of all auto defaults. The high prevalence of 72+ month loans in auto defaults shows that extending loans past vehicle lifecycles can significantly increase risk.

Signal Intelligence provides an executive-friendly workbench that can analyze thousands of related variables across extended-term cohorts. The system can detect signals that a long-term borrower’s risk profile is deteriorating, enabling proactive portfolio management. Risk executives gain valuable insight into the velocity of credit mitigation across vehicle classes and multi-year origination tranches.

When a lender sees unexpected changes in roll rate velocity in their extended loan portfolio, loss forecasting models fall behind. A 50-basis-point variance in projected defaults across a $500 million extended-loan portfolio directly impacts capital allocation.

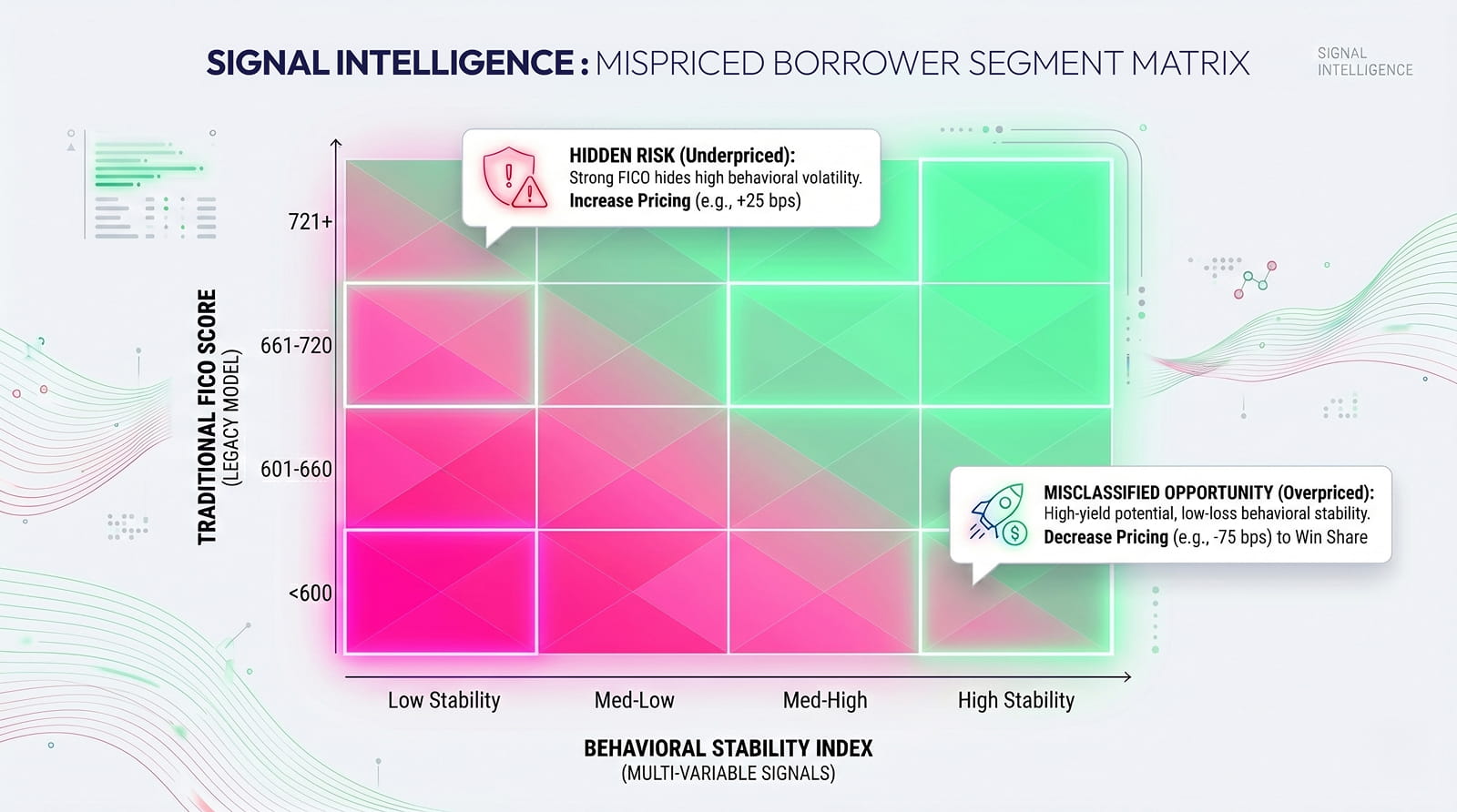

Optimizing loan pricing means discovering precise pockets within the portfolio where risk is either higher or lower than market-driven models indicate. By finding small but significant pockets, lenders can accept loans with higher- or lower-risk profiles than predicted by adjusting loan terms accordingly. Such an approach allows lenders to capture market share from competitors who rely on unadjusted macro-level models.

A financial institution that uses traditional credit decision models routinely rejects profitable borrowers and underprices hidden risks. Playing it “too safe” across entire credit tiers means lenders give up high-yield, low-risk loans to savvier competitors, sacrificing income without providing any guarantee of additional portfolio resilience.

Pricing inefficiencies are evident in recent industry performance benchmarks. According to TransUnion, auto loan 60+ DPD consumer-level delinquency rates have surpassed 2009 financial crisis peaks. In a high-risk environment, a broad tightening of credit lowers loan volume and suppresses net interest income without necessarily identifying the highest risk areas.

Surgical pricing optimization depends on finding hidden sub-segments of borrowers whose behavioral histories deviate from their nominal credit score. A borrower with a sub-600 FICO score may exhibit strong cash-flow stability when evaluating multi-relational variables such as a stable utility payment history and low debt-to-income volatility. Automating the discovery of these patterns allows institutions to price loans based on actual risk rather than broad market assumptions.

Signal Intelligence can serve as an executive workbench, enabling them to uncover profitable Precision Impact Segments hidden within high-risk buckets. The granularity of Signal Intelligence enables credit leaders to identify the predictive lift of specific signal combinations, allowing them to adjust rules accordingly and maximize interest income while maintaining strict risk guardrails. Because the automated credit decisioning engine extracts and identifies complex correlations between different sources of borrower data, it can reveal stable cash-flow signals that traditional black-box models would ignore.

For example, a credit union analyzing historical origins might identify segments with loss rates below the portfolio baseline. Finding precise segments of the portfolio that are overperforming would allow the institution to adjust risk-adjusted pricing by 75 basis points to win high-quality business without increasing risk.

Traditional credit scoring models rely on broad, static, point-in-time snapshots like FICO, which only capture averages. Signal Intelligence uses automated pattern discovery to analyze complex, multi-relational data across internal and external data sources. Signal Intelligence identifies behavioral and temporal signals, such as the Rate of FICO score increase, to provide a dynamic, highly accurate prediction of the risk trajectory for better decision strategies and a faster decision-making process.

A Precision Impact Segment is a highly specific group of borrowers defined by complex, combined risk signals found across multiple data sources. Impact segments isolate risk drivers, such as subtle shifts in employment combined with dealer trade-in variances, that drive EPD. By identifying these precise pockets, lenders can adjust underwriting with surgical precision, blocking toxic loans without restricting overall origination volume.

Automated signal discovery significantly reduces the latency tax of manual feature engineering, moving risk pattern identification from months to days. This efficiency enables weekly Signal Audits and Post-Model Adjustments, thereby protecting net interest margin and reducing operational cost. A 1% reduction in false positives or a 10% increase in predictive lift in behavioral scores can save large lenders millions in annualized losses.

Signal Intelligence acts as an overlay, outputting all discovered risk logic as transparent, system-ready SQL code or plain-English rules. This allows the new rules to be seamlessly fed into the existing loan origination system (LOS) via knockout rules or Post-Model Adjustments (PMAs). This capability eliminates the common “IT bottleneck” and enables credit teams to react instantly to market shifts.

Roll Rate Velocity measures the speed at which loans move from early-stage delinquency (30 DPD) to terminal default (90 DPD). Tracking the acceleration of this velocity is the most critical leading indicator of future charge-offs, providing the only viable window for intervention. When not monitored, an accelerating Roll Rate Velocity causes reserve projections to be outdated, directly impacting capital allocation and increasing loss severity.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。