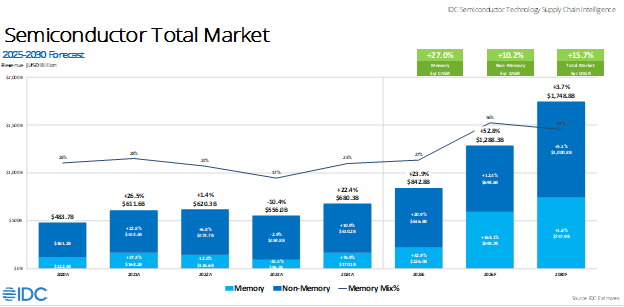

The global semiconductor market is undergoing a seismic transformation. IDC’s latest forecast projects the industry will surge past the $1 trillion revenue threshold in 2026, significantly ahead of prior forecast expectations. The growth will be driven overwhelmingly by AI infrastructure investment which is reshaping the entire market.

Total semiconductor revenues are forecast to reach $1.29 trillion in 2026, up 52.8% year-over-year from $842.8 billion in 2025. The memory segment is at the epicenter of this upheaval: DRAM revenues alone are projected to nearly triple in 2026 to $418.6 billion, driven by demand for High-Bandwidth Memory (HBM) and DDR from hyperscalers and AI infrastructure providers. Meanwhile, non-memory semiconductors are growing at a robust but more measured pace, reaching $693.5 billion in 2026.

Let’s break down the three big forces reshaping semiconductors right now: why AI infrastructure has become the industry’s new center of gravity, what’s really happening in memory markets (and why it matters beyond the data center), and how other markets from automotive and IoT to mobile and PCs are trying to navigate a market that increasingly plays by AI’s rules.

The single most consequential shift in the semiconductor market is the emergence of AI infrastructure as a structurally dominant end market. What began as a cyclical uplift in data center spending has evolved into a self-reinforcing investment cycle that is reshaping demand patterns across the entire semiconductor value chain.

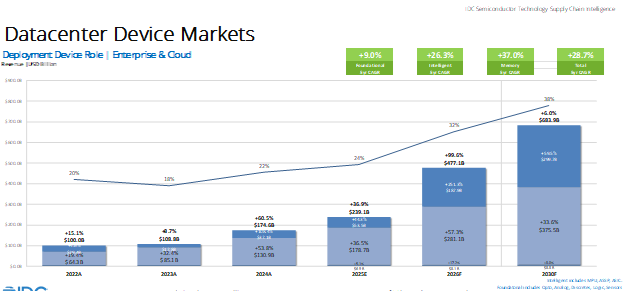

Hyperscale capital expenditure exceeded $100 billion for the first time in Q3 2025, and the i4 alone are expected to increase their CapEx by 70% year over year to approximately $600 billion in 2026. IDC forecasts data center semiconductor revenues to reach $477.1 billion in 2026. By 2030, data center semiconductors will account for $843.2 billion — nearly half the total semiconductor market at that point.

“The semiconductor industry has crossed a structural threshold. AI is no longer a demand catalyst — it is the demand foundation. The race to build out AI infrastructure is consuming silicon at a pace the industry has never seen, and the implications for memory, logic, and packaging are profound.” — Jeff Janukowicz, Research VP, Semiconductors & Semiconductor Manufacturing, IDC

The $281 billion “Intelligent” datacenter segment — encompassing CPUs, AI accelerators, GPUs, custom ASICs, and the associated networking silicon — now constitutes the single largest identifiable category within non-memory semiconductors. Spending is heavily concentrated among the top-tier hyperscalers (Amazon Web Services, Google Cloud, Microsoft Azure, Meta, and a handful of sovereign AI infrastructure programs) who have secured long-term supply agreements with leading chip manufacturers.

Three things are keeping this growth self-sustaining rather than cyclical:

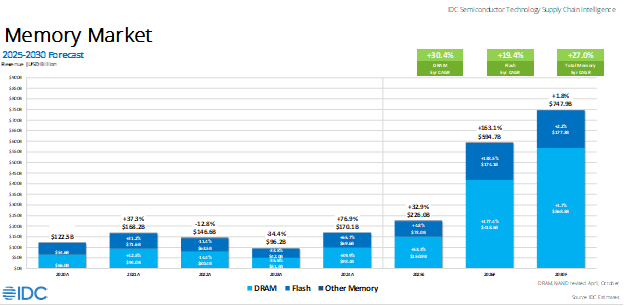

If you want to understand what’s really happening in semiconductors right now, start with memory. The numbers are almost difficult to comprehend: Total memory revenues rise from $226 billion in 2025 to $594.7 billion in 2026, then to $790.4 billion in 2027. This isn’t a recovery cycle — that’s a market being fundamentally repriced and structurally changed.

DRAM is where the action is. IDC forecasts $418.6 billion in DRAM revenues for 2026, up 177% year-over-year. And what makes that figure notable is this: It’s not primarily a volume story driven by consumer devices. The hyperscalers aren’t just buying more DRAM — they’re buying a fundamentally different, far more expensive class of memory, and they’re willing to pay a premium to secure supply. Each HBM chip requires significantly more silicon real estate, further tightening the availability of other types of DRAM.

“The memory market is at an unprecedented inflection point, with demand materially outpacing supply. For an industry long characterized by boom-and-bust cycles, this time is different. The rapid expansion of AI infrastructure and workloads is placing significant pressure on the memory ecosystem. As a result, the market is shifting from a cyclical recovery following the 2023 downturn to a more structurally constrained environment, with clear implications for end markets.” — Jeff Janukowicz, Research VP, Semiconductors & Semiconductor Manufacturing, IDC

High-bandwidth memory (HBM) has become the primary constraint in the AI accelerator supply chain. Most capacity is already pre-committed through 2026, with leading suppliers indicating limited availability and forward allocations extending into 2027. That capacity is concentrated in NVIDIA and AMD GPU platforms, along with a growing set of hyperscaler custom AI silicon programs, leaving little unallocated supply. The production economics are fundamentally different from conventional DRAM: HBM relies on through-silicon via (TSV) stacking and advanced packaging on silicon interposers alongside logic dies, resulting in per-bit costs that are several times higher — typically in the ~3–5× range—than standard DRAM.

Samsung, SK Hynix, and Micron have all committed to aggressive HBM capacity expansion, but the capital intensity and technical complexity mean meaningful new supply will not reach the market until late 2026 at the earliest. This supply constraint is, paradoxically, a positive pricing dynamic for memory vendors even as it creates severe allocation challenges for systems integrators.

NAND Flash revenues are forecast to reach $174.1 billion in 2026, up 138.5% from $73.0 billion in 2025. AI infrastructure is the dominant demand driver here as well, though through different mechanisms: large language model checkpoint storage, training dataset infrastructure, and high-performance NVMe storage for inference farms are absorbing NAND supply at unprecedented rates.

Unlike DRAM, where HBM has created a two-tier pricing structure, the NAND market is experiencing a broader-based repricing. Enterprise SSD contract prices have surged 50-90% in early 2026, as hyperscalers secure priority allocation through long-term supply agreements. As a result, NAND availability in consumer and OEM channels for devices such as PCs and smartphones is increasingly constrained, with prices rising significantly.

While AI infrastructure commands the headlines, the non-AI semiconductor economy tells a more nuanced story. Non-memory, non-datacenter revenues are projected at $406.3 billion in 2026, with several end markets facing headwinds as memory cost inflation, supply allocation, and macroeconomic headwinds create significant margin and demand compression.

Mobile phone semiconductor revenues are forecast to decline to $89.8 billion in 2026, down 13.8% from $104.2 billion in 2025. This is one of the few major semiconductor end markets showing outright revenue contraction in the current cycle, and the causal mechanism is instructive.

The constraint is not demand for smartphones as consumer upgrade appetite remains solid, particularly for AI-capable devices. Rather, the problem is that memory cost inflation is compressing OEM margins and disrupting product planning. DRAM and NAND together typically represent 15-20% of a flagship smartphone’s bill of materials. With prices up significantly year-over-oyear, OEMs face three difficult choices: absorb the cost (margin destruction), pass it to consumers (unit volume risk), or reduce memory specifications (product differentiation erosion).

Several major OEMs have delayed planned H1 2026 flagship launches as a result, compressing the window for semiconductor content revenue recognition. Reflecting these dynamics, IDC has lowered its 2026 mobile phone forecast, citing weaker near-term demand and cost pressures from elevated component pricing. IDC expects the mobile semiconductor market to stabilize and return to modest growth in 2027 as memory pricing normalizes and AI-on-device silicon becomes a clearer demand driver.

Automotive semiconductor revenues are forecast to soften to $60.1 billion in 2026, down from $64.5 billion in 2025 — and unlike mobile, memory isn’t really the culprit here. While memory costs do impact automakers, they generally require automotive grade memory which is a different set of products. The segment is impacted by more traditional macro factors: tariff costs being passed through to consumers, high interest rates, and a demand shock from the Iran conflict disrupting the Strait of Hormuz and pushing energy prices and broader inflation higher. U.S. new vehicle sales are expected to decline modestly in 2026 after consumers pulled forward purchases ahead of tariff implementation in 2025. The new EV market has taken a hit from the expiration of the federal EV $7,500 tax credit.

The longer-term case for automotive silicon remains intact. More chips per vehicle, ADAS proliferation, and software-defined architectures are structural tailwinds that don’t go away. But in 2026, those tailwinds are being offset by forces well outside the semiconductor industry’s control. Automotive is best understood this year as a market in a holding pattern rather than in retreat.

The IoT semiconductor segment is projected at $136.6 billion in 2026, down modestly from $140.8 billion in 2025, before stabilizing at approximately $130-138 billion through 2028. The near-term softness reflects several overlapping pressures: inventory digestion among industrial IoT vendors, cost inflation from memory components, and macro-driven caution in enterprise IoT capex.

The more interesting question for IoT is what happens next. Edge AI, running inference locally on sensors, cameras, and industrial endpoints rather than sending data to the cloud, is starting to create a new, higher-value demand category within the segment. The chips required are more capable, more expensive, and more differentiated than traditional IoT silicon. IDC expects edge AI to be a meaningful growth driver for IoT semiconductors by 2027-2028, and that’s the storyline worth watching.

IDC’s base case forecast projects semiconductor revenues growing to $1.75 trillion by 2030. Several key dynamics will shape this trajectory:

“What the data makes clear is that the semiconductor market has undergone a permanent expansion of its addressable opportunity. AI infrastructure has reset the demand baseline, memory has repriced as a strategic asset, and the industry’s growth trajectory through 2030 is no longer contingent on a consumer refresh cycle.” — Nina Turner, Research Director, Semiconductors, IDC

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。