When former IAS officer Kunal Mali (name changed) fell ill in Ahmedabad, his family was given the “option” of choosing between Indian and more expensive German stents. The family, predictably, said they wanted the “best”, and four stents were inserted in a single operation. Despite Mali’s Central Government Health Scheme card, the family ended up paying a few lakh rupees out of pocket (this was before stents were brought under price control).

A few years later, when the 77-year-old Mali was rushed to the All India Institute of Medical Sciences (AIIMS), New Delhi, with similar complaints, the doctors were aghast that four stents had been used previously in one go! His daughter, a senior government official, said: “We were scared and trusted the doctors. It never crossed our minds that they could be misleading us.”

In urban India, such stories are commonplace, fuelled by the expansion of private healthcare and a growing pool of patients who opt for it, whether enabled by insurance, discouraged by long waits in public hospitals, or compelled by the urgency of their condition. Unsurprisingly, their trust in the medical system and in doctors is fast eroding. But since doctors remain the face of a system that is unregulated and focussed on corporate profits, they bear the brunt of the ire while the system itself remains largely unscrutinised.

Popular literature and cinema from the turn of the 20th century up to the 1950s and 1960s often featured a benevolent doctor who treated patients with little or no money, sometimes being paid in fruits and vegetables while braving the barbs of his impoverished family. Doctors and Indian healthcare have traversed a long road since then, as has, admittedly, the quality of healthcare. India’s life expectancy at birth was 32 years at the time of Independence; it is 68 to 70 years now. India is also a healthcare destination for patients around the world.

But this development has come at a price. Catastrophic health expenditure annually pushes an estimated 63 million Indians into poverty. At least since the last decade, a slew of government insurance schemes have sought to address this issue, but they do not cover the cost of outpatient care, drugs, or rehabilitative therapy.

According to NITI Aayog estimates, there are an estimated 40 crore people—the “missing middle”—who are too “rich” to be eligible for these schemes but cannot afford to buy a comprehensive private health insurance plan either. Healthcare inflation in India is estimated to be at 14 per cent, several times the retail inflation rate, which hovers at around 3 per cent. The exponential rise in healthcare expenses is not an isolated phenomenon. It is due primarily to four factors: the rising cost of medical education, rapidly evolving medical technology, scant government oversight on the billing practices of private hospitals, and as counter-intuitive as it may sound, the increased penetration of health insurance.

The PMJAY rate has become the benchmark for all patients, insured or otherwise. Here, a woman waits with her infant at Modern Government Maternity Hospital, in Petlaburj, Hyderabad, on August 5, 2022. | Photo Credit: G. Ramakrishna

According to grassroots researchers, the Pradhan Mantri Jan Arogya Yojana (PMJAY)—widely seen as a game changer for providing Rs.5 lakh annual health cover to eligible families—has also, paradoxically, boosted smaller private players and intensified existing inflationary pressures in healthcare. (The PMJAY is the tertiary care plan of India’s flagship health programme, Ayushman Bharat.)

Dr Shailendra Hooda and his team at the Institute for Studies in Industrial Development have tracked healthcare costs in Rajasthan from the time the Rashtriya Swasthya Bima Yojana (RSBY) was the only government health insurance scheme and that too primarily intended for migrant workers. The annual cover provided under the RSBY was Rs.30,000. In 2015, the State launched the Bhamashah Swasthya Bima Yojana (BSBY), which subsumed the RSBY and increased the total annual health coverage to Rs.3.30 lakh, with a distinction made between general illnesses (with a coverage limit of Rs.30,000) and serious illnesses (Rs.3 lakh).

Then came the PMJAY in 2018 under which annual family health insurance cover jumped to Rs.5 lakh. As I was doing research for my book Games Hospitals Play, Dr Hooda explained to me: “Under the RSBY, the cover for natural childbirth, for example, ranged from Rs.2,500 to Rs.4,500. The hospital would spend between Rs.3,000 and 3,500 for every procedure. So, patients sometimes had to pay a small sum out of their pockets. Under the BSBY, the cover went up to Rs.5,000. Hospitals now began making a small profit. The PMJAY pays Rs.9,000 per delivery.”

The PMJAY rate has become the benchmark for all patients, insured or otherwise. “Hospitals have started saying that this is the fixed rate for deliveries. While 40 per cent of the population is covered under the PMJAY, others—except the minuscule population with private insurance—have in effect seen an increase in medical expenditure after the PMJAY,” Dr Hooda pointed out.

Pushing expensive treatments for the insured

The fact that insurance schemes have made healthcare pricey is well documented. Moral hazard refers to the tendency of insured individuals to take unnecessary risks knowing they will not bear the full cost of the consequences. In health, however, it is not the insured individual that takes more risks; the term refers to the propensity of healthcare providers—doctors or hospitals—to push more expensive treatment options to people who have health insurance. Procedures that qualify as “moral hazard” include hysterectomies (uterus removal), C-sections, angioplasties (insertion of stents to open blocked blood vessels), and appendectomies (removal of the appendix).

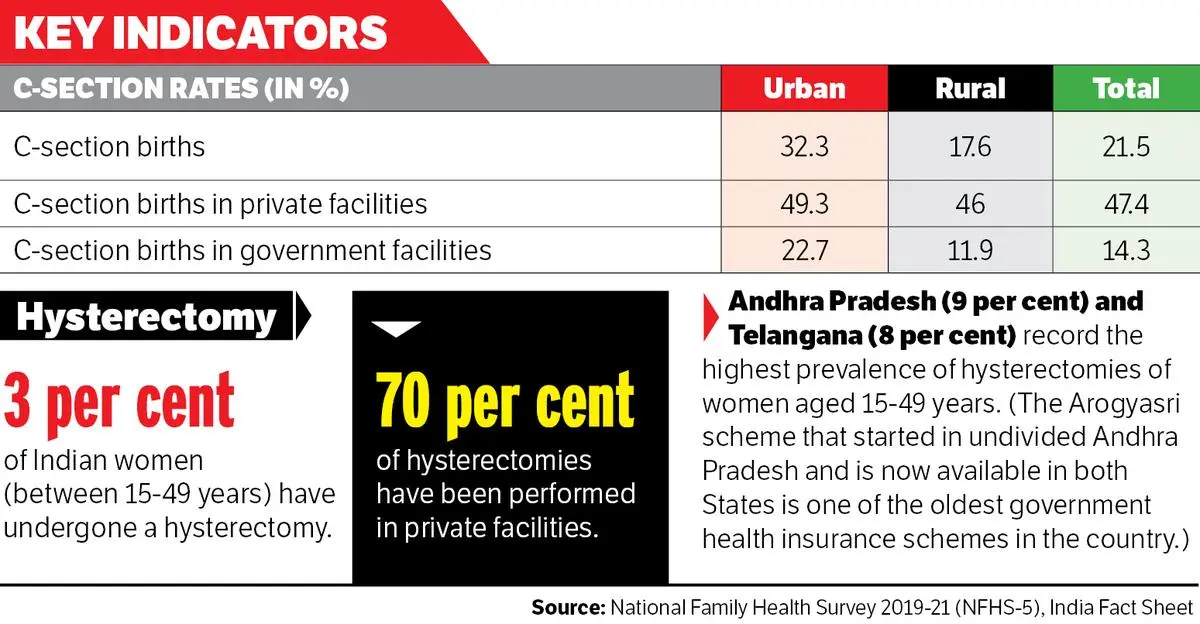

A report by the Federation of Obstetric and Gynaecological Societies of India in 2023 noted that hysterectomies were the most common non-obstetric gynaecological surgery among Indian women of reproductive age, with an estimated 3.3 per cent of women having undergone it. It noted: “There are also reports of potential coercion for financial benefits under health insurance schemes and concerns pertaining to the lack of information provided to women on side effects.” Around 70 per cent of all hysterectomies were carried out in the private sector, the National Family Health Survey 2019-21 (NFHS-5) found.

The choice of tests and technology to be used, at all stages of treatment, is a crucial determinant of cost. | Photo Credit: G. Ramakrishna

An analysis by the National Health Authority, the PMJAY’s administrative agency, found that 2 per cent of the claims submitted by women were for hysterectomies. And six States (Chhattisgarh, Uttar Pradesh, Jharkhand, Gujarat, Maharashtra, and Karnataka) generated three-quarters of all hysterectomy claims.

Further, the India Fact Sheet of the NFHS-5 report records that 32.3 per cent of deliveries in urban India and 17.6 per cent in rural India were C-sections. This is significantly higher than the 10 to 15 per cent that the WHO terms “optimal” in a population.

Private hospitals display an uncanny proclivity for surgical deliveries, with C-sections accounting for 49.3 per cent of births in urban facilities and 46 per cent in rural ones. The corresponding figures for government health facilities were 22.7 per cent and 11.9 per cent, respectively. C-sections, in fact, happen to be among the top 10 most used packages under the PMJAY.

With little regulatory oversight, scrutiny of private hospital billing falls largely to insurers, who may then exercise rudimentary price control through pre-negotiated rates with healthcare providers. This often happens to be the case when patients who pay out of pocket to bypass insurance approval delays find that their bill has gone up.

Increasing premiums and unexplained deductions in approval amounts also raise questions about insurance companies’ motive and functioning. During his tenure as Secretary of the Department of Financial Services, Vivek Joshi, a current Election Commissioner, had written to the Secretary of the Ministry of Health & Family Welfare at the time, Sudhansh Pant, saying there was a need for a health regulator to make insurance affordable.

A senior government functionary emphasised the need for regulation: “The Clinical Establishments (Registration and Regulation) Act, 2010, [or the CE Act] clearly lays down that hospital charges should be prominently displayed. But health is a State subject. There is no binding regulatory framework. The Supreme Court has now laid down that private hospitals need to be regulated. Programmes like the PMJAY do ensure some indirect regulation, but the problem is that the biggies do not join. During COVID-19, we used the Disaster Management Act [2005] to regulate the private sector. We have to figure out a tool to do that now. States have to step in. Even the CE Act, which was designed as a model, is stuck in a no man’s land. I think just around eight States have adopted it. We are looking for solutions. Civil society should also step in with suggestions. We are in listening mode.” The official did not come on record given the sensitivity of possible future interactions with private hospitals on the topic.

Doctors succumbing to management pressure

Significantly, young doctors have been under unprecedented financial stress in the last few years. Previously, while consultants could gently parry management pressure, new-age salaried doctors increasingly succumb to it. A senior respiratory medicine practitioner in Kolkata said: “I have worked in a private hospital for 23 years and have never taken a salary. In fact, I used to pay 10 per cent of the fees I received to the hospital. That gave me the freedom to practice medicine with integrity. When the management asked me about low admission rate, I could dismiss them in half jest, saying: ‘I am a good doctor. Patients get better in [my] OPD [outpatient department]’.”

Such legroom is shrinking for young doctors. For more than a decade, there has been a sustained policy focus on increasing the number of doctors in an effort to reach the WHO benchmark of 1 doctor for every 1,000 people. Flourishing private medical colleges have increased the number of medical seats but with an exponential fee hike, which in some cases touches Rs.1 crore.

At the crowded outpatient wing of a government hospital, in Vijayawada, on November 2, 2025. | Photo Credit: G.N. Rao

Burdened by enormous educational loans, young medical graduates are perfect candidates for corporate hospitals’ new model of employing salaried doctors. Like any corporate employee, they are given “targets” for the number of tests, admissions, and interventions to be carried out to recover the costs of their own salaries.

Additionally, a quid pro quo model of referral has emerged where if a doctor refers his patient to another, the latter must return the favour. A similar logic often dictates intra-hospital referrals too in the private sector. Meanwhile, the patient has to pay two doctors for visits and tests. Referrals are subjective decisions: some may save lives while others deplete bank balances. Even for tests, financial considerations may decide which pathology laboratory a doctor or a hospital prefers.

Dr Amar Jesani, a former editor of Indian Journal of Medical Ethics, traces unnecessary referrals to “structural asymmetry”: “In the 1960s, when the sector was nascent, the focus was on producing more doctors rather than strengthening the system. So, the system could not really absorb all the doctors being produced each year. About 25 per cent of them got government jobs. The others were left to the open market to build their own practices. Big cities were the only places where they could possibly make a living. To compete, they developed a fee-for-service system where they paid other medical practitioners, alternative medicine practitioners, and others to refer patients to them.”

He added: “Healthcare is a unique market. Prices do not necessarily come down when there are more providers. The competition may actually cause the price of healthcare to increase.”

Incidentally, some of the first independent hospitals were for maternity care, which built businesses using a slightly more expanded version of the model, reaching out to individual obstetrics and gynaecology specialists for referrals. Since specialists needed a place to perform deliveries and a fully functioning operation theatre for C-sections, they began working out of the hospitals for both a fee and a commission from the bill. From this development emerged the “consultant”. “As the system expanded and larger conglomerates came in, healthcare continued to get more pricey because the commissions downstream started being built into the model,” said Dr Jesani.

The lack of legal mandate enforcing compliance

The need for a regulator is a recurring theme in conversations on healthcare inflation. When the CE Act was passed, there were hopes of streamlining clinical decision-making processes to reduce uncertainties and unnecessary resource use. Standard treatment guidelines were introduced in all medical disciplines, but what is lacking is a legal mandate enforcing compliance. This means that an insured patient may be subjected to endless tests and billed without ever being provided with a diagnosis.

That is what happened to Arzoo Kumar (name changed) in March 2024 when a corporate hospital in Kolkata billed her for Rs.1,20,209.77, of which Rs.93,316 was for investigative tests. Her case was heard by the West Bengal Clinical Establishments Regulatory Commission that ruled that should the insurance ombudsman uphold her insurance provider’s decision to deny her claim on the ground that there was no diagnosis, the hospital must reduce her bill by Rs.1 lakh. Kumar underwent clinical investigations, including blood and urine tests, an ultrasound, a CT scan, an MRI, and even tests for autoimmune diseases, but nothing concrete was revealed about her pain.

This is not an isolated incident. It is a documented global phenomenon that patients in emergency care like Kumar are routinely overbilled. A 2017 analysis by researchers at the Johns Hopkins School of Medicine, based on Medicare billing records from 2,707 US hospitals, found that emergency admissions were billed at rates 340 per cent higher.

Prime Minister Narendra Modi at the launch of the Pradhan Mantri Jan Arogya Yojana, in Ranchi on September 23, 2018, which was attended by the then Jharkhand Governor and current President Droupadi Murmu and others. | Photo Credit: Manob Chowdhary

The choice of tests and technology to be used, at all stages of treatment, is a crucial determinant of cost. A senior oncologist formerly with the AIIMS cited the example of proton beam radiotherapy (PBR) to emphasise that technology is an enabler only when appropriately used. PBR is used to detect paediatric brain tumours with precision and to minimise damage to the surrounding areas. “To push PBR in all cases is like using a machine gun to kill a housefly. The cost differential is massive: the proton therapy could cost 80 to 90 per cent more than regular radiotherapy,” the doctor said.

A top neurosurgeon at a government trauma centre also said that better technology was not always the better option: “For patients with a head injury, the first test of choice is always a CT scan. It takes about a minute and may cost around Rs.1,000 at a private hospital. But most patients who are referred [to the government centre where I work] from the private sector have undergone an MRI and not a CT scan. An MRI takes about 30 minutes and can cost anything between Rs.10,000 and Rs.30,000.”

Healthcare inflation is multifactorial, but what has made it spiral out of control is the lack of guard rails. The issue has been raised repeatedly in Parliament, most recently by Swati Maliwal and Sanjay Singh in the Rajya Sabha. There have been instances of public outrage over unacceptably high bills handed to families of deceased patients, but redress has rarely been more than cosmetic. Government insurance schemes are a beginning, but for universal health coverage to become a reality in India, it is important to bring both the quality and the cost of healthcare across sectors to an optimal level.

Abantika Ghosh is a journalist and public policy professional. Her second book, Games Hospitals Play (Bloomsbury, 2025), deals with the billing practices of private hospitals.

Also Read | Ayushman Bharat PMJAY: A health scheme that needs healing

Also Read | Path to privatisation