The Reserve Bank of India’s rate-setting panel preferred to err on the side of caution, standing pat on the repo rate and continuing with the neutral monetary policy stance as the spillover from the ongoing West Asia war threatens to stoke inflation and impede growth.

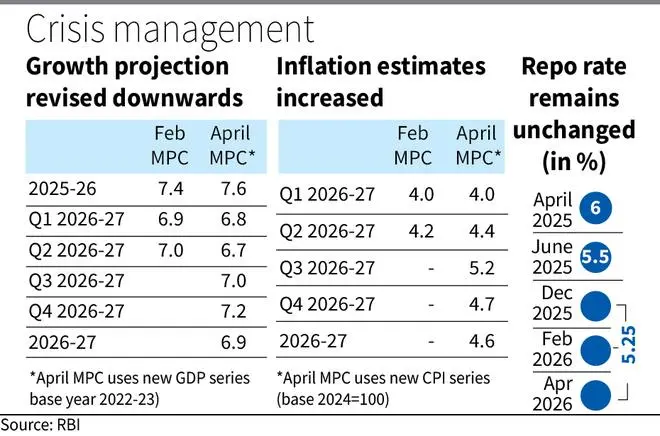

At their first meeting of FY27, all six members voted unanimously to leave the policy repo rate (the interest rate at which the RBI provides liquidity to banks to overcome short-term mismatches) unchanged at 5.25 per cent.

The repo rate was last cut in December 2025 by 25 basis points, from 5.50 per cent. In June 2025, the monetary policy stance changed from “accommodative” to “neutral.”

While no action on the repo rate and stance fronts was widely anticipated by bankers and economists, the RBI’s real GDP and retail inflation projections for FY27 clearly reflect the fact that the West Asia conflict has heightened risks to inflation and growth.

The RBI expects real GDP growth to be a shade below 7 per cent at 6.9 per cent (vs the NSO's FY26 estimate of 7.6 per cent). Further, it projected FY27 retail inflation at 4.6 per cent (vs RBI’s FY26 estimate of 2.1 per cent).

For the first time, the RBI gave a core inflation (excluding food and energy components) projection. This is projected at 4.4 per cent for FY27.

The surge in global crude oil prices since the West Asia conflict, exacerbated by significant supply disruptions, has tilted risks to inflation on the upside and growth on the downside, per the latest monetary policy report.

Governor Sanjay Malhotra observed that a supply shock is confronting the economy. So, it is prudent to wait and watch the changing circumstances and the evolving growth-inflation outlook.

Assessing the impact of the ongoing West Asia war on the Indian economy, the RBI chief warned that elevated crude oil prices could increase imported inflation and widen the current account deficit.

“Disruptions in energy markets, fertilisers and other commodities may adversely impact industry, agriculture and services, reducing domestic output.

“Heightened uncertainty, increased risk aversion and safe haven demand could impact domestic liquidity conditions, economic activity, consumption and investment,” he said.

Malhotra underscored that weaker global growth prospects may dampen external demand and reduce remittance flows. Further, adverse spillovers from global financial markets could tighten domestic financial conditions and raise the cost of borrowing.

“Overall, the initial supply shock can potentially transform into a demand shock over the medium term if the restoration of supply chains is delayed,” he cautioned.

The RBI Chief emphasised that the fundamentals of the Indian economy are on a stronger footing at the current juncture than in the previous crisis episodes, as well as many other economies, providing it with greater resilience to withstand shocks.

To a specific question on the current low interest rates continuing, Malhotra said: “So, it is quite possible that these low rates continue for a long time. As I mentioned, structurally, the Indian economy is very strong, very resilient, very robust. Despite shocks, we are projecting 6.9 per cent real GDP growth.”

He highlighted that structurally, long-term macroeconomic fundamentals continue to remain very strong (because of various measures taken by the government, the RBI and various institutions), driving growth on the one hand, and keeping price pressures contained on the other.

Published on April 8, 2026