Although the joint statement on the interim US–India Bilateral Trade Agreement (BTA) did not say so, a simultaneous executive order from President Trump claimed that India has agreed to his demand to reduce the purchase of Russian crude to zero.

While the Indian authorities have not confirmed this, such a move is quite likely to increase India’s crude oil import bill. Data on import prices disseminated by the Ministry of Commerce shows that though the discount between crude oil from Russia and from other sources has narrowed from the highs recorded in 2022–23, Russian crude oil is still cheaper than most alternative suppliers, such as the US, UAE, Nigeria and Saudi Arabia, as of December 2025.

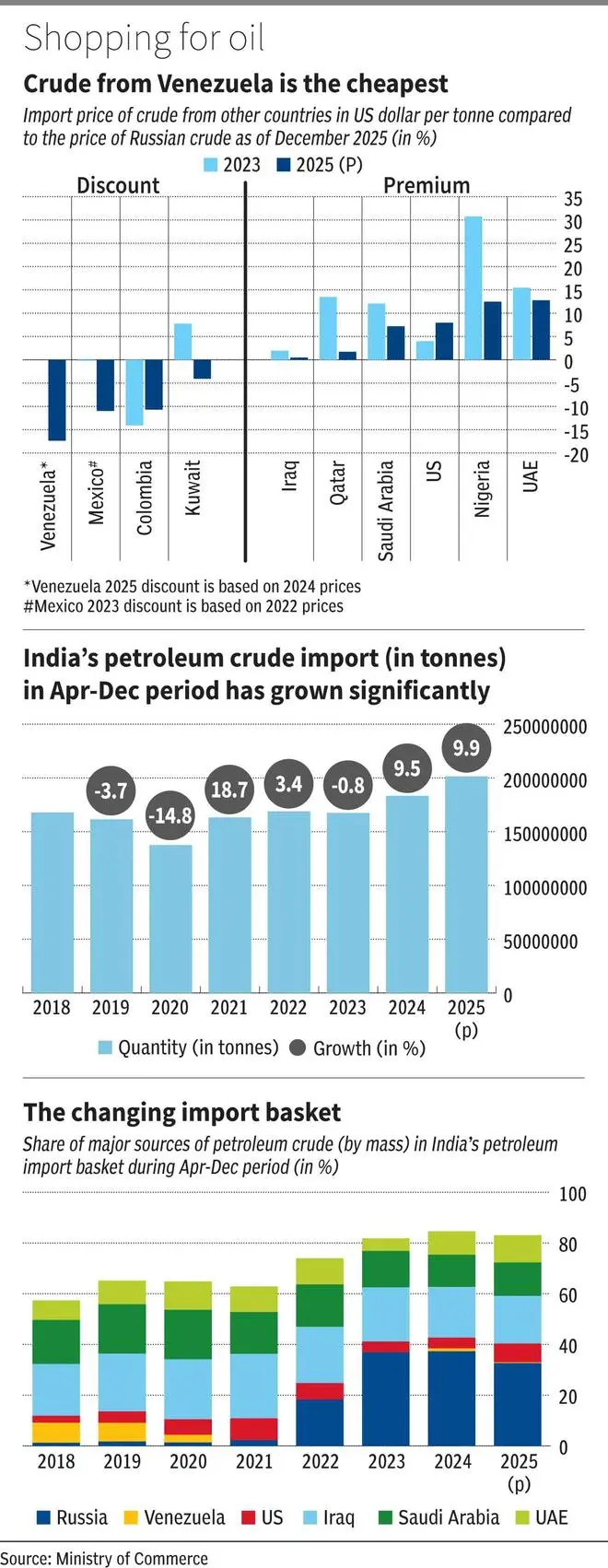

Discounts and premiums in Dec 2025

According to the Ministry of Commerce, price per tonne of petroleum crude oil from Russia averaged $469 in December 2025. Meanwhile, petroleum crude from the US which was priced at $506.7 per tonne in December, was at a 7.9 per cent premium to Russian crude. Crude oil from the UAE was priced at $529.4 and from Saudi Arabia at $503.2 per tonne.

Saudi Arabian crude was at a premium of 7.2 per cent to crude oil from Russia while the UAE had a premium of 12.8 per cent compared to crude oil from Russia. Nigerian crude at $527.9 per tonne, enjoys a steep 12.5 per cent premium because it predominantly supplies light crude.

Supplier-wise pricing shows deep discounts persisting across a few sanctioned or distressed producers. Venezuela’s crude was about 17.4 per cent cheaper than India’s average import price from Russia in December 2024, while Mexico was about 11.0 per cent and Colombia about 10.7 per cent cheaper than Russian crude in December 2025. Important to note here is, all three of Venezuela, Mexico and Colombia export heavy to very heavy grades of crude, requiring significant processing costs.

Sourav Mitra, oil & gas partner at Grant Thornton Bharat said, “India’s Russian oil imports hit a peak of about 2 million barrels per day (bpd) in June 2025, which has come down to 1.1 million bpd in January 2026. However, the oil flow from Russia to India is unlikely to vanish completely anytime soon as these strategic decisions are based on factors such as supply chain reorientation, diplomatic alignments, pricing stability, and energy security.”

Rising import volumes, changing supplier shares

India’s crude import demand continues expanding alongside economic growth. Total imports in 2025 (Apr–Dec) reached about 201.5 million tonnes, marking roughly 9.9 per cent year-on-year growth after a similar rise in 2024 and a strong rebound from pandemic-era lows.

Within this expanding market, sourcing patterns are shifting but not fully reverting. Russia still accounted for roughly 32.7 per cent of India’s crude imports in Apr–Dec 2025, down from 2024 yet far above pre-2022 levels. Iraq held about 18.8 per cent, Saudi Arabia 13.2 per cent, and the UAE 10.8 per cent, while the US supplied roughly 7.4 per cent. Venezuela’s presence remained marginal at about 0.3 per cent.

According to Akshat Garg of Choice Wealth, “India imports roughly 300 million tonnes of crude oil annually, with Russia accounting for about one-third of that. If those barrels are replaced at global prices that are even $8–10 per barrel higher, India’s annual oil import bill could increase by roughly $6–8 billion. This additional cost would widen the trade deficit, put pressure on the rupee and either feed into higher domestic fuel prices or raise the fiscal burden through subsidies.”

Published on February 9, 2026