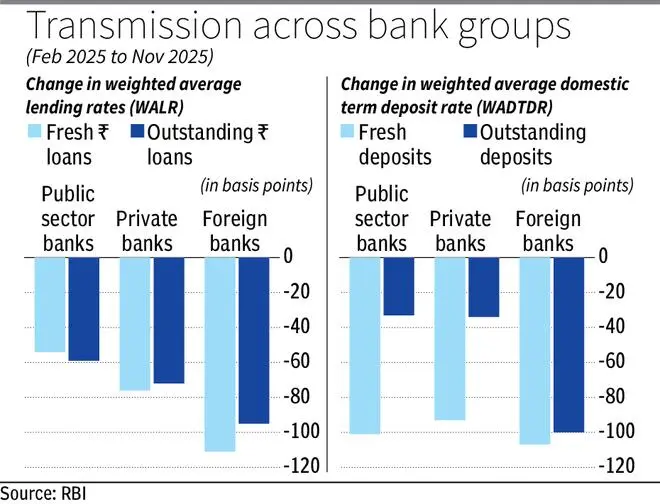

The effectiveness of monetary policy hinges on how quickly banks pass on repo rate changes to borrowers. Foreign banks have been the most agile in passing on the entire rate cuts in the current cycle (between February to November 2025) on both outstanding and fresh rupee loans. Private banks have completed around three-fourth of the transmission to loans.

But public sector banks have been the slowest, bringing down the weighted average lending rate (WALR) on fresh loans by only 54 basis points and WALR on outstanding loans by 59 basis points.

Deposit rate transmission

The RBI had cut the repo rate by 100 basis points between February 2025 and November 2025 in a bid to boost growth and to help the economy deal with geopolitical challenges.

Foreign banks have cut the deposit rates on both fresh as well as outstanding deposits by more than 100 basis points in this cycle, probably in a bid to protect their margins. Private and public sector banks have managed to pass the entire rate cut to fresh deposits, while the transmission in outstanding deposits is very low, around 33 per cent.

Transmission in lending rate

As far as lending rate is concerned, public sector banks have been markedly slow in transmission.

But foreign banks have cut the WALR for fresh rupee loans by 111 basis points in this cycle. The WALR on outstanding loans also fell 95 bps.

Private sector banks have also been quicker in bringing down their lending rates this cycle with WALR on fresh loans declining 76 bps while the rate on outstanding loans declined 72 bps.

Why Public Sector Banks Lag

The transmission of changes in ‘repo rate’ has been strongest in foreign banks due to almost 94 per cent of their outstanding floating rate loans being linked to external benchmark-linked (EBLR). Interest rates on EBLR linked loans are immediately reset when the repo rate is hiked or cut.

In contrast, the marginal cost of funds-based lending rate (MCLR) ties the lending rate to the cost of funds raised by the bank, and is slower to adjust.

Around 46 per cent of the outstanding floating loans of PSBs are linked to MCLR, while the proportion for private banks is only 10 per cent.

Published on January 26, 2026