Markets are often narrated through headlines. In one phase, liquidity becomes the defining explanation. In another, it is reform momentum, geopolitical uncertainty, interest rates, or foreign flows. Bull runs are celebrated as a triumph of confidence; weak phases are blamed on anxiety and indecision.

Yet, when one steps back and looks at the Sensex over the last 40 years, a quieter and more durable truth becomes evident. Markets, over the long run, are driven less by stories and more by arithmetic.

That arithmetic is uncomplicated. Equity returns over time broadly reflect earnings growth (Sensex basket of companies), with changes in valuation adding or subtracting from returns only temporarily. Put simply, investors ultimately earn what corporate India delivers in profits. Excitement, pessimism, and market mood may influence prices in the short term, but over a decade or more, earnings do the heavy lifting.

This is an unfashionable conclusion in an era increasingly drawn to index milestones, target levels, and dramatic market calls. But it is the most useful lesson that the Sensex offers as it completes four decades of existence.

Earnings do the heavy lifting

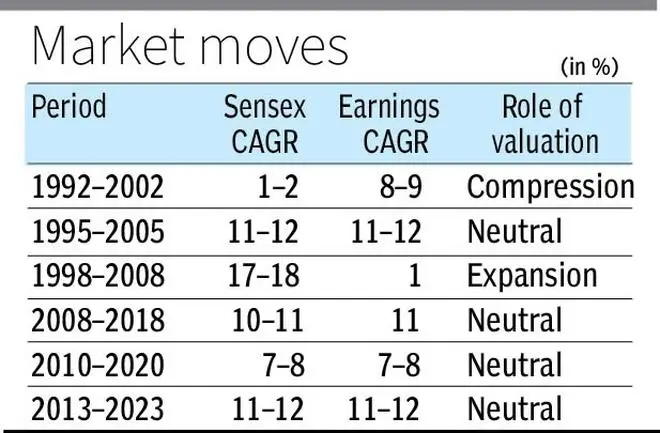

A long view of market history shows that over most rolling 10-year periods, Sensex returns have broadly tracked earnings growth. On average, both have stayed in the vicinity of 10-11 per cent. There have been periods when returns have moved well above this band, but those episodes were typically driven by a combination of strong earnings growth and a sharp expansion in valuation multiples. They were exceptions, not the rule.

The years from the late 1990s to 2008 remain the most striking example. That period combined rapid profit growth with a powerful re-rating of the market. Earnings growth moved into the mid-teens, while price-to-earnings multiples expanded significantly. The result was a phase of unusually strong equity returns that still shapes investor memory today. But that memory can also be misleading. Exceptional periods tend to become the standard against which normal market behaviour is judged, and that often distorts expectations.

Myth of extraordinary returns

The post-global financial crisis period offers a useful counterpoint. Market returns in many of those years were far more restrained and largely mirrored earnings growth, with little help from re-rating. This underlines a critical point: valuation expansion can amplify returns for a while, but it rarely sustains wealth creation on its own. Unless earnings keep growing, markets eventually run out of momentum. This is why investors often misread long phases of subdued market performance. Range-bound or moderate-return periods are frequently seen as signs of stagnation or disappointment.

In reality, they are often phases of adjustment, when earnings continue to rise but valuations remain stable or contract. Such stretches are not signs of market failure. They are part of the natural process through which markets reconnect prices with fundamentals.

Realistic reading

This has direct relevance for the present market environment. India’s equity market today appears to be in an earnings-led phase rather than a valuation-led one. Earnings growth remains reasonably healthy, but valuations are already demanding, and the interest-rate backdrop does not offer the kind of broad support that typically fuels a dramatic re-rating.

Under such conditions, expecting returns to remain broadly aligned with earnings growth may be more realistic than hoping for another prolonged phase of outsized gains. That is not a pessimistic view. It is a disciplined one.

The problem with equity investing is rarely that long-term returns are inadequate. The problem is that investors often expect them to be spectacular all the time.

The enduring lesson

The larger lesson from 40 years of the Sensex is therefore both simple and humbling. Corporate earnings grow over time. Market returns, over long periods, broadly follow that growth. Valuation cycles can create temporary bursts of exuberance or phases of disappointment, but they do not rewrite the long-term equation.

The arithmetic of markets may not be dramatic. But it has proved more reliable than the stories told around them.

Saravanan is Professor of Finance, IIM Tiruchirappalli; and Manas is Associate Professor of Finance, Goa Institute of Management, Goa

More Like This

Published on April 6, 2026