The Reserve Bank of India (RBI) has announced two key changes to provisioning norms in the banking sector as part of the development and regulatory measures in its monetary policy.

First, the RBI has scrapped the regulation on floating provisions (often referred to as FPA-like provisions). Previously, this norm barred banks from crediting profits to capital adequacy calculations if NPAs fluctuated by more than 25 per cent from the quarterly average. With this change, even if NPAs rise and provisions increase, banks can now bolster their capital adequacy ratios (CRARs), making their capital positions appear optically stronger.

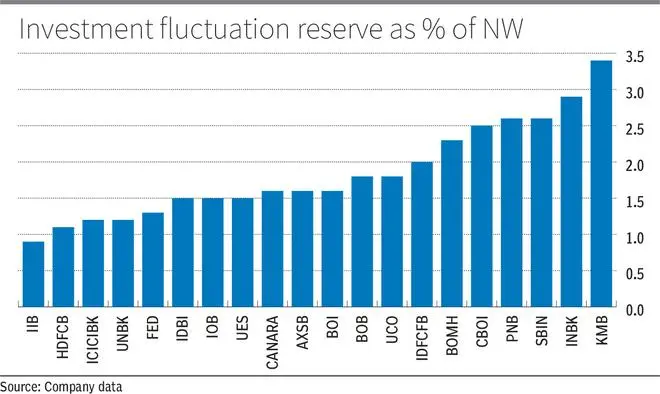

Second, the RBI is eliminating the Investment Fluctuation Reserve (IFR) requirement for banks that maintain adequate reserves in the Available for Sale (AFS) category, which already capture mark-to-market (MTM) movements. Banks holding existing IFR balances may now offset MTM impacts against these reserves, though the RBI is yet to clarify the exact treatment.

Both measures appear aimed at improving capital optics amid emerging stresses. This latest easing of regulatory guardrails reflects the RBI’s anticipation of higher MTM losses and rising credit costs, stemming from economic slowdowns and geopolitical disruptions, particularly the ongoing Middle East conflict. By allowing these impacts to be absorbed without directly hitting capital adequacy ratios, the central bank seeks to free up capital for lending.

These moves represent a continuation of the broader regulatory easing initiated under RBI Governor Sanjay Malhotra, which stands in sharp contrast to the tightening approach adopted by his predecessor, Shaktikanta Das, which was widely seen as the primary reason for growth slowdown.

Under Governor Das, the RBI had focused on tightening norms to curb risks associated with uncollateralised retail and NBFC lending, over-leveraged households (including borrowers with multiple loans), and AIF exposures. The objective was to prevent reckless credit growth. However, since assuming charge, Governor Malhotra has reversed several of these measures, including restrictions related to NPAs and credit cards, hoping for a turnaround in economic growth. During his tenure, the RBI has also implemented a cumulative 150 basis points rate cut in 2025, bringing the repo rate down to 5.25 per cent, and injected substantial liquidity into the system (approximately ₹14-15 lakh crore) through Open Market Operations (OMO), CRR reductions, and currency swap interventions.

Despite these efforts, the sharp depreciation of the rupee and lagging deposit growth led to hardening G-Sec yields, even as inflation remained relatively subdued, indicating weak transmission of the final leg of monetary easing; symptomatic of ineffectiveness of monetary policy measures in an economy confronting structural drags. Thus, economic growth remained subdued until the middle of FY26, prompting the government to introduce fiscal support measures such as GST rate cuts and income tax relief.

Revival in credit growth

A recent revival in credit growth, which surged to 15.4 per cent in April, has been driven by a combination of factors: an episodic spike in consumer loans (especially auto loans) linked to GST-related purchases, and industrial lending growth of 14.8 per cent YoY, largely due to distress-induced higher working capital demand amid rising raw material and energy costs, particularly in cyclical sectors. However, corporate sales and earnings have remained modest, with Nifty companies reporting just 3.5 per cent earnings growth in FY26 (and 1.5 per cent for Sensex constituents). Weakening top-line performance and operating cash flows point to underlying crunch. This pressure has spilled over to MSMEs and cyclical industrial sectors, further amplifying credit demand.

Services sector lending has also strengthened, particularly to NBFCs, supported by regulatory easing and a sharp rise in external commercial borrowing (ECB) costs due to the depreciating rupee. Meanwhile, the credit-deposit ratio for banks has climbed to 83 per cent, pushing them towards costlier wholesale funding. This has resulted in margin pressure, with early signs of stress visible in unsecured segments and narrowing spreads across the banking system.

The ongoing Middle East conflict has exacerbated these risks, potentially leading to higher MTM losses (especially for public sector banks), fresh NPAs arising from demand and supply shocks, oil shortages, and a rebound in inflation towards 6 per cent. With inflation now projected to rise to 6-7 per cent in FY27, well above the RBI’s target of 4.6 per cent with an upside bias, the central bank has limited room for further monetary accommodation.

Given the constrained space for conventional monetary policy support, these pre-emptive regulatory measures appear largely cosmetic. They seek to reclassify and mask risks within the capital framework rather than addressing underlying structural issues. With multiple guardrails eased over the past 1.5 years under Governor Malhotra, combined with external shocks from the war, there is a growing risk of excessive forbearance, which could leave the banking sector more vulnerable in the future.

Comparative regulatory stance

Shaktikanta Das’s tenure: Marked by a strong emphasis on regulatory tightening to mitigate risks arising from rapid growth in unsecured lending.

Sanjay Malhotra’s approach: Shifted the focus towards easing measures to support economic revival and reduce compliance burdens.

Key tightening measures under Governor Das:

Significantly increased risk weights on consumer credit (personal loans excluding housing, education, vehicles, and gold) to 125 per cent for both banks and NBFCs.

Raised risk weights on credit card receivables to 150 per cent for banks and 125 per cent for NBFCs.

Increased risk weights on bank lending to NBFCs by 25 percentage points (if the existing weight was below 100 per cent).

Mandated banks and NBFCs to set board-approved limits on unsecured sub-segments, with top-up loans on existing assets treated as unsecured.

Highlighted concerns regarding unsustainable credit growth, asset-liability mismatches from short-term deposits, potential NBFC-bank contagion risks, usurious lending by MFIs, and weaknesses in algorithm-based underwriting models.

To curb evergreening of NPAs through Alternative Investment Funds (AIFs), mandated banks to liquidate exposures to debtor companies within 30 days, failing which 100 per cent provisioning would be required.

The December 2023 Financial Stability Report highlighted rising delinquencies, including: 8.2 per cent vintage default rate in personal loans; 42.7 per cent of borrowers with three or more accounts (multiple borrowings); increasing overdue loans in small-ticket borrower segments.

Key easing measures under Governor Malhotra:

Reduced risk weights for microfinance loans from 125 per cent back to 100 per cent.

Lowered risk weights for NBFC infrastructure lending to 75 per cent or 50 per cent (depending on performance and stage), effective April 2026.

Reduced risk weights on credit card transactors (full re-payers) to 100 per cent.

Scrapped the Investment Fluctuation Reserve buffer, which was previously required to cover mark-to-market depreciation.

Removed the 25 per cent cap on NPA provision deviations from the quarterly average for the purpose of including quarterly profits in CRAR calculations.

This pivot from Shaktikanta Das’s risk-mitigation approach — which successfully stabilized GNPA ratios at around 1.9 per cent — to Sanjay Malhotra’s growth-oriented stance (with over 80 regulatory changes in 2025) reflects a deliberate shift towards boosting lending, especially in cyclical sectors. Since assuming office in late 2024, Governor Malhotra has focused on regulatory easing to support economic revival and reduce compliance burdens, in contrast to Das’s (2018-2024) emphasis on tightening norms to curb risks from rapid unsecured lending. However, this easing carries the risk of excessive forbearance amid weak corporate cash flows and rising external challenges.

The writer is CEO and Co-Head of Equities & Head of Research, Systematix Group. Views are personal

Published on April 14, 2026