Bengaluru’s housing market is in the midst of a supply boom, yet the distribution of that supply tells a troubling story. The city is building for the few, not for the many. An analysis of residential projects launched in Bengaluru shows that, since 2022, for every home priced below ₹80 lakh, developers have delivered five homes above that mark.

The ‘High-Level Task Force on Affordable Housing for All’, constituted by the government of India in 2008, sets a clear affordability benchmark: a household should spend no more than five times its annual income on purchasing a home, or no more than 30 per cent of its monthly income on EMI payment. According to the 2023-24 Economic Survey of Karnataka, Bengaluru’s average per capita income stands at ₹7.6 lakh. Assuming two earners with average incomes, a household can realistically afford a home priced at ₹76 lakh. Yet market data suggest otherwise.

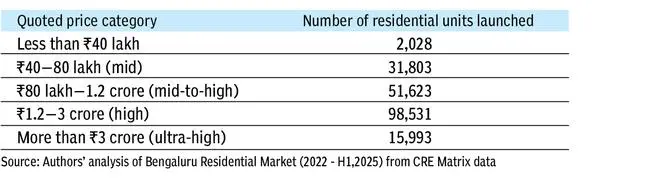

An IIHS analysis of private residential projects launched in Bengaluru since 2022, collected by real estate data aggregator, shows that only 33,831 housing units are priced below this threshold. The bulk of private supply remains concentrated above ₹80 lakh, revealing a significant gap between what households can afford and what the market delivers.

The study considered units priced between ₹40-80 lakh as affordable, while those between ₹80 lakh and ₹1.2 crore as high-end, aligning with prevailing market classifications. Most new launches since 2022 are concentrated in the ₹80 lakh to ₹3 crore range, far removed from what developers typically describe as “affordable.”

A geography of inequality

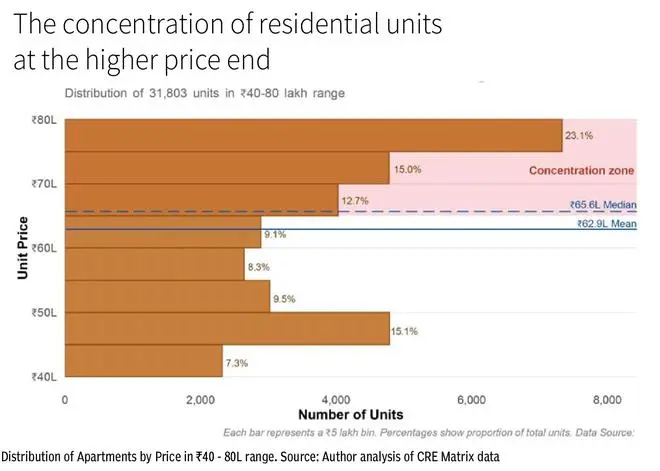

Even within the ‘affordable bracket’ the supply is further skewed. Most units are priced towards the upper end of the ₹40-80 lakh range, with a visible concentration between ₹65-80 lakh. This leaves limited options for low-income households for home ownership. More importantly, 75 per cent of the units are not yet ready for occupancy, projects remain under construction or stalled, which further exaggerate the existing rental burden on households. Until possession is handed over, households often pay EMIs on new homes while continuing to pay rent, doubling their housing costs.

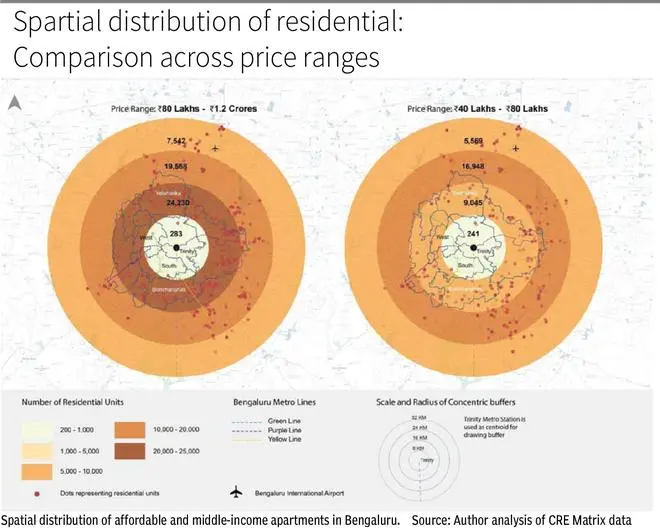

Spatial patterns further deepen the divide. Housing units priced between ₹80 lakh and ₹1.2 crore are largely located within an 8-16 km radius of the city core, where access to infrastructure, public transport and employment hubs is stronger, reducing everyday commuting and service costs. In contrast, units priced below ₹80 lakh are systematically pushed beyond the 16-km radial radius from the city centre, pushing affordability to the urban periphery.

These peripheral locations are typically characterised by inadequate infrastructure. Many lack access to municipal water supply and underground sewerage systems, forcing households to depend on off-grid arrangements, which are often unreliable and expensive. Public transport connectivity remains fragmented, while access to social infrastructure such as schools, healthcare facilities and neighbourhood amenities is uneven.

Once the hidden costs of inadequate infrastructure, longer commutes, and poor connectivity are taken into account, the very premise of “affordable” housing begins to unravel. Premium housing closer to the city core, by contrast, benefits from location advantages, metro connectivity, and better access to hospitals, schools, and civic services.

Policy levers for a failing market

The analysis shows that houses priced below ₹80 lakh remain severely under-supplied and are largely confined to poorly connected peripheral locations. As a result, even affordable units often become practically unaffordable due to high commuting and infrastructural costs, and weak access to jobs and services. Private developers face higher upfront costs, longer sales cycles, and greater demand risk in these projects. This pushes them towards the high-end segment, where returns are faster, margins are higher, and infrastructure costs can be internalised within pricing. Consequently, the market continues to prioritise luxury and ultra-luxury housing, reinforcing spatial and income inequalities. Expecting market forces alone to address this imbalance ignores the structural realities driving the supply.

Expanding the supply of affordable housing requires deliberate state intervention. The government has three primary levers to expand the supply of affordable housing: government-led development of housing stock, partnerships with private developers, and regulatory frameworks that incentivise or mandate private sector participation. Each, however, faces significant implementation challenges.

Government-led housing projects often struggle with execution and market alignment resulting in high vacancy rates, driven by poor location choices and limited understanding of demand dynamics. The Seventeenth Report (2023) of the Standing Committee on Housing and Urban Affairs, which evaluated the implementation of Pradhan Mantri Awas Yojana (Urban), notes that Karnataka has a substantial stock of vacant government-built affordable housing under PMAY-U. Many such projects continue to see low uptake and high vacancies.

Public-private partnership models have been undermined by weak deal structuring and administrative delays. Affordable housing projects operate on thin margins where timely execution is critical. Approval bottlenecks increase costs and erode viability, discouraging private players. Regulatory mechanisms are limited at the state-level. While PMAY-U offers financial incentives to developers, it falls short of resolving the underlying supply-side constraints.

Effective policy intervention requires the state to move beyond voluntary incentives and adopt enforceable mandates, such as zoning and land allocation, particularly in high-demand and well-connected areas to prevent the housing landscape to be determined almost exclusively by market dynamics.

Bengaluru’s housing challenge is not just a question of supply, it is an urban equity crisis with serious implications for the city’s long term economic competitiveness. A city that cannot house its essential workforce ultimately undermines its own economic base. As the private sector continues to gravitate towards luxury and ultra-luxury housing, decisive government intervention can no longer be delayed. Policy must therefore move beyond intent and create flexible instruments that bring private players into affordable housing or mandate their participation outright.

The writers are with Indian Institute for Human Settlements (IIHS), Bengaluru. Data Visualisation: Yashita Singh, IIHS

Published on March 31, 2026