With the IMD’s forecasts for below normal rainfall, the debate on retail food inflation has begun. This year’s situation is more critical, with a heatwave, energy price shocks and issues related to fertilisers also expected to play a key role in food prices. However, economic research appears to be divided on the impact of lower-than-normal rainfall on food inflation.

While the Indian Metrological Department (IMD) has pegged the 2026 monsoon at 92 per cent of the Long Period Average (LPA), with a model error margin of ±5 per cent, private forecaster Skymet has projected rainfall at 94 per cent of LPA, also with a ±5 per cent margin. This places the season firmly in the “below-normal” category; a normal monsoon is defined as rainfall between 96 per cent and 104 per cent of the LPA. As Indian farmers are largely dependent on the South-West Monsoon for irrigation, a below normal monsoon has added to the worries.

The possibility of lower productivity due to various factors, including a below normal monsoon, will have an impact on food inflation and that will, in turn, push headline inflation. While the share of Food & Beverages has declined in the new series (base year 2024), it remains the largest component of the CPI basket. The share in the previous series (base year 2012) was 45.86 per cent, against 36.75 per cent now.

In its note CRISIL said that in the coming months, while a low base will perk up food inflation, the adverse impact of heatwaves and increased risk from a below-normal South-West monsoon assign an upside to food inflation.

Nomura said while inflation has a patchy relationship with monsoon levels, an overly hot summer and sub-normal rains could impact agricultural output and pose an upside risk to food prices.

“In addition, potential shortages of fertilisers could increase input costs for farmers, even as prices are considerably subsidised by the government. Rising commodity prices could further add to imported food inflation, especially in items such as edible oils, where India is a net importer,” the agency said, while adding that lower demand from restaurants and households coping with LPG shortages could temper some of the inflationary pressures. “We expect a gradual uptick in food & beverage inflation from 3 per cent in Q1 to close to 6 per cent by Q4,” it said.

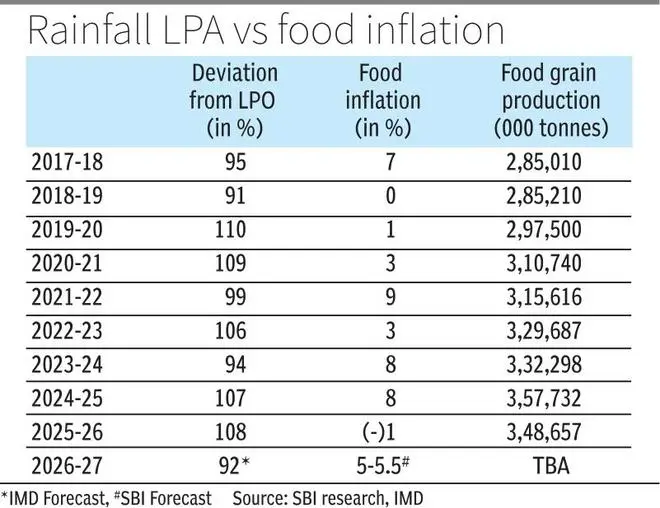

However, SBI Research has a slightly different take. Historical patterns suggest that the relationship (below normal monsoon and food inflation) is not linear. “Years with relatively comfortable rainfall have witnessed elevated food inflation such as 98 per cent rainfall with 8.43 per cent food inflation in FY09, 102 per cent with 15.2 per cent in FY11, while weaker rainfall years such as 93 per cent (FY13) and 91 per cent (FY19) were associated with much lower food inflation of 6.3 per cent and 0.09 per cent, respectively,” it said.

Further, it imphasised that the implication is that the all-India monsoon average, by itself, is an insufficient guide to the food price outlook. What matters more is the spatial distribution of rainfall across major crop-producing regions and its timing during the sowing and crop-development phases. Further, parts of the North-East, North-West and South Peninsula may still receive normal to above-normal rainfall. Hence, “even if the monsoon settles near 92 per cent of LPA, the food inflation implications are likely to remain limited unless rainfall deficiency becomes concentrated in key kharif-producing belts,” it said.

Published on April 14, 2026