Young Indians looking to make a start on retirement savings often get a rude shock when they learn the amount of money they need to save to retire. Financial planners and online calculators come up with eye-popping numbers when you seek estimates of a target corpus.

For instance, a 30-year-old looking to retire at 60 may find that she needs a ₹20-crore or ₹21-crore corpus to retire. To get to this sum, SIP (systematic investment plan) calculators show, she will need to invest ₹58,038 a month in equity SIPs for the next 30 years. Such targets look so outlandish to some folks, that they completely give up on thinking about retirement and put off investing indefinitely.

But not thinking about retirement, or not saving for it, are the worst personal finance decisions you can make. Therefore, we decided to look at how you can trim those retirement targets and make them more achievable.

Built on assumptions

Before taking a dive into the numbers, it is important to understand that the retirement targets thrown up by financial planners or calculators are not cast in stone. They are guesstimates built on several assumptions.

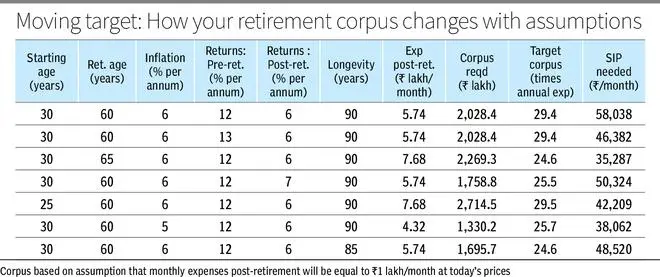

Usually, to arrive at a retirement target, calculators use six variables — your starting age, your retirement age, your longevity, inflation rate, portfolio returns before retirement and portfolio returns after retirement. In deciding the size of corpus you need, some variables have more influence than others.

For instance, 30-year-old Sarala with expenses of ₹1 lakh a month at today’s prices, wants to retire at 60. To estimate her target corpus, the calculator assumes a 12 per cent return on her investments from now until 60, a 6 per cent return from age 60 to 90 (because you can’t take a lot of risk post-retirement), a 6 per cent inflation rate and a longevity of 90 years.

The target corpus it throws up is ₹20.28 crore, about 29 times her annual expenses (₹5.74 lakh) at 60. To get to this number with a fixed monthly SIP, it says, she will need to put aside a massive sum of ₹58,038 monthly for the next 30 years. Now, this looks positively scary and may prompt Sarala to lose all hope of ever retiring.

Trimming the target

But in reality, even small tweaks in some of these assumptions can substantially trim the corpus she needs to build. Let’s say Sarala gets lucky and faces only 5 per cent inflation instead of 6 per cent. In that case, her required corpus drops dramatically to ₹13.3 crore from ₹20.28 crore. Retail inflation in India has averaged 6 per cent over a 30-year period, but in recent years inflation has been much lower, as monetary policy has been more effective. As the Indian economy matures, it is quite possible that inflation rates will trend down. That will substantially trim the retirement goals we’re all targeting.

Or let’s stick with 6 per cent inflation. If Sarala decides to take on slightly more risk after retirement and earns 7 per cent on her post-retirement portfolio instead of 6 per cent, she can get by with a retirement kitty of ₹17.6 crore instead of ₹20.3 crore. If she trims her longevity assumption and sets it at 85 and not 90, that sharply reduces her target corpus to ₹16.9 crore too.

However, in financial planning it pays to be conservative. Therefore, it would make sense for Sarala to budget for higher inflation and longevity rather than underestimate these assumptions and struggle later.

The one variable she can tweak is her returns post-retirement. By switching from a fully debt portfolio to one that has about 20 per cent equities, she may be able to bump up her returns from 6 per cent to 7 per cent, thus reducing her target corpus by a cool 14 per cent.

Trimming your investments

If Sarala is clever, she can choose to leave the target corpus unchanged and play around with the size of SIPs she needs to invest. Here, when she starts investing and her retirement age make a big difference.

For instance, if she wakes up to the retirement problem at 25 instead of 30 and starts her SIPs immediately, she can get to ₹27.1 crore by age 60 with a SIP of ₹42,209. If she decides to postpone her retirement by five years to 65, she can manage with SIPs of ₹35,287 a month.

While postponing your retirement age may not be wholly in your hands, making an early start certainly is. Many young people delay their first investment interminably because they believe that they don’t have “enough” and must have a fat pay cheque before they invest. Or they keep waiting for a great investment opportunity to knock on their doors. But in the compounding formula, time is the most powerful force, not the amount invested or returns! Did you know that advancing your SIP start from 30 to 25, can boost up your final corpus by 86 per cent? If Sarala starts five years early, the SIP she needs drops by 27 per cent. If she delays her investments from 30 to 40, the SIP she needs nearly doubles!

Similarly, if Sarala manages better returns during her working life, 13 per cent instead of 12 per cent, that trims her SIP amount by 21 per cent.

This goes to show that the other way to make your retirement target more achievable is to start early and take professional advice on your portfolio to earn better returns.

Step up your SIP

Finally, even those “lower” SIPs mentioned above look pretty daunting to most. However, do remember that the above calculations assume that your SIP will remain flat over the next 30 years. Starting with an affordable number and stepping up your SIPs as your income rises over the years, can help you reach very tall targets.

A ₹30,000-SIP started at 30 in an equity fund with a 12 per cent return, will get you to just ₹9.96 crore by 60, if you stick with a flat SIP through your working life. But if you increase your ₹30,000-SIP by 10 per cent every year, you get to a neat corpus of ₹23.95 crore in the same time.

Increasing your investments by 10 per cent a year may seem like an unrealistic ask in your 20s. But in your 30s and 40s, your income often expands far faster than your spending as your career progresses, sharply boosting your saving ability. All you need to do is to ensure that you don’t upgrade your lifestyle faster than your income!

The most important lesson from all this number-crunching is: Don’t let tall retirement targets daunt you. Get started early on equity investments. Make a start with a small sum, keep stepping it up as your career takes off, and you will certainly get there.

The author is a Contributing Editor

Published on February 28, 2026