An epochal change of guard was triggered in motion last week with Kevin Warsh getting Senate confirmation of his appointment as the next Chairman of the US Fed’s Board of Governors and Jerome Powell stepping down. As the most influential central bank in the world, the actions of the US Fed have had anywhere between moderate-to-significant impact on investors across the world. As Powell hands over the baton after eight years at the helm, Warsh takes charge at one of the most tumultuous times in US Fed’s history, with the added pressure of a President constantly trying to influence the Fed’s independence.

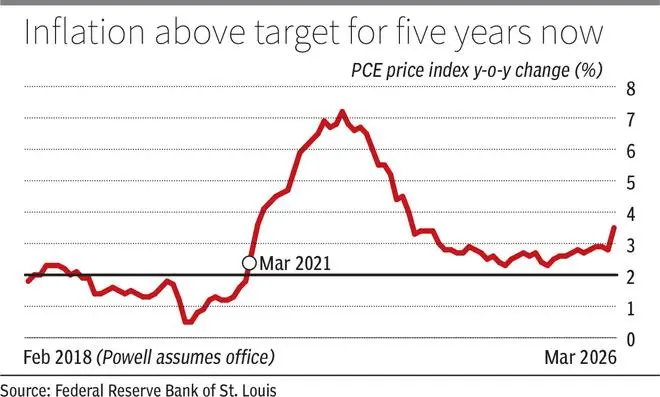

Warsh has his work cut out, especially on the inflation front. The PCE (personal consumption expenditure) price index, which the Fed targets to keep under 2 per cent, has now remained above the target level for 61 months straight—the longest since such targeting was started in 2012. It has recently crept substantially to 3.5 per cent in March — the index’s latest reading, from 2.8 per cent in February. Higher energy prices are starting to show up in the inflation print. Long-term yields have gone up by about 100 bps since September 2024 despite a 175-bps cut in the Fed Funds Rate (FFR) in the same period. On Friday alone, Powell’s last day in office, US 10-year yields spiked a considerable 12 bps. How about that for a send off!

And if this wasn’t enough, as Powell departs, the Fed’s Open Market Committee is the most divided (apparently driven by politics too) in 34 years with the recent FOMC decision receiving four dissents — the highest since 1992.

Taming inflation rather eliciting the perception thereof would be crucial for Warsh and investors alike, going forward. Here we look back at an episode in history where failure to rein inflation meant investors benefitted by buying gold over equities and why investors need to pay heed to the Fed’s actions closely from here. For equities to outperform gold, Warsh has to get the house in order.

Before hopping on the time machine, here’s an interesting stat. In Powell’s term which spanned eight years (two terms of four years each), gold has outperformed equities. While a 13-per cent CAGR for equities is no bad thing, gold has beaten equities by a comfortable margin with a CAGR of 16 per cent. This puts Powell in the bottom half of the table of Fed Chairs in the last five decades under whose term gold outperformed equities.

Occupying the bottom half alongside Powell is Arthur Burns, under whose term gold trounced equities. When he assumed office in February 1970, inflation (PCE price index) was as high as 5 per cent, driven up primarily by expansive spending on the war in Vietnam and social welfare programmes funded by government debt. The FFR was also commensurately high at 9.75 per cent (positive real returns). Inflation did cool to about 3 per cent. However, ahead of the Presidential election in 1972, the Fed apparently succumbed to political pressure from the incumbent Nixon administration, thereby prematurely lowering the FFR to as low as 3.5 per cent by February 1971. An artificial short-term boom, consequently, handed Nixon a win but not so much for the US economy. Inflation soared to a peak of around 12 per cent by 1974-end, coupled with the 1973 oil shock, giving rise to a cost-of-living crisis. The economy tumbled into a stagflation — a period of weak economic growth and high inflation. Basically, no one wants to consume in such times. The Fed eventually played catch up to quell inflation by raising the FFR to 13 per cent. As an inflation hedge, gold soared but equities faltered.

That wasn’t all. Burns believed the inflation was caused by transient supply-side concerns and it did not have a lot to do with monetary policy or extravagant government spending. He even disregarded ‘volatile’ food and fuel from the inflation basket and only targeted the other constituents (core inflation) — thus getting back to pumping liquidity and lowering the FFR to around 5 per cent by 1976-end. Inflation also declined to an equivalent 5 per cent by then. But Burns did not realise it was only artificial and that inflation would come back with a vengeance in the start of the 1980s.

William Miller took charge as the next Fed Chair as Burns’ term expired. He, too, had similar beliefs to Burns on inflation and continued to have a dovish stance. Inflation, which had settled at around 6 per cent when he assumed office, quickly spiralled out of control towards 9 per cent by July 1979. FFR was taken upward to over 10.5 per cent — but it was too late, too little and the damage had been done already. While Burns poured gasoline on inflation, Miller lit the match. Dollar started plummeting and markets had completely lost faith in the Fed by then, leading the Carter government to replace Miller with Paul Volcker.

When Volcker took charge, he pulled a masterstroke. Shortly after assuming office, he cranked the FFR to an unprecedented 20 per cent by March 1980 and shocked the markets. This while inflation was still around the 12 per cent mark, driving massive real returns. More than the numbers, it restored faith in the Fed that inflation will be defeated. The perception mattered.

However, this meant the economy underwent couple of recessions—a short one in 1980 and a longer one in 1981-82. These were bitter pills for the economy to swallow to correct the monetary excesses infused over a decade-and-a-half. By early 1982, inflation had cooled rapidly to around 5.5 per cent and then it went on a gradual decline to 3.3 per cent when Volcker’s second term expired. A notable feature of Volcker’s term is that even after the FFR was lowered from 20 per cent, it was always maintained at a substantial margin over the inflation rate (average of 5.3 per cent and a minimum of about 3.4 per cent), encouraging savings and thus removing liquidity excesses. Equities outperformed gold in his tenure (see table).

What’s more important is that Volcker set up a perfect stage for his successor Alan Greenspan, nicknamed the ‘Maestro’ (due to his roots in music) who ‘conducted’ the economy through a golden period of growth with controlled inflation. Markets liked him and he went on to serve the second longest term as the Fed Chair spanning 18.5 years across five presidents (both Democratic and Republican). Nevertheless, he became a bit too market-friendly towards the end of his final term, laying down the foundations of the 2008 sub-prime mortgage crisis. His consistent dovish inclinations after the recession in 2001 was one of the causes of the housing bubble, which eventually culminated in the global financial crisis of 2007-08.

Warsh is about to take over when the world is going through turbulent times. History suggests that a delayed or inadequate response to inflation can prove costly for equities. The recent rise in bond yields reflects the market’s scepticism over the Fed’s ability to keep inflation expectations anchored.

Warsh, therefore, has a rough road ahead to navigate. The key questions now are whether the Fed will remain independent, will prices rise, whether inflation will be managed effectively, and which asset classes will fare best over the medium term. For investors across the world too, this matters whenever they revisit their asset allocation between gold and equities.

Powell himself reveres Volcker and has admired him as the ‘greatest public servant in the economic arena’. However, given the Fed’s failure to tame inflation under 2 per cent for five years now, the jury is still out on Powell’s legacy and might risk being written alongside that of Burns and Miller, rather than that of Volcker.

Published on May 16, 2026

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。