In the 10th year of the siege of Troy, the Greeks did something unexpected. They stopped fighting. They sailed away, leaving behind a single wooden horse on the beach as an apparent offering to the Gods. The Trojans, after a decade of successfully defending the mightiest walls in the ancient world, wheeled the horse through their gates. That night, Greek soldiers, hidden inside the horse, opened the city gates from within. Troy fell, not because its defences failed, but because the threat arrived in a form its defenders never recognised as a threat.

The walls of Troy were real. They had held for 10 years against the finest army of the age. What the Trojans could not process was that the nature of the attack had changed. The horse was not a battering ram. It was not a siege tower. It was something that looked like a gift, something the Trojans brought inside themselves.

Some of the famed quality companies and consistent compounders that swelled the coffers of Indian investors in the previous decade may now be facing this ‘Trojan threat.’ In long-term investing, investors need to be alert to such inflexion points that can alter the investment case that held steady for decades. The changed circumstances need to be evaluated for making the right investment calls. We try to explain this with the example of how things played out for two famed companies.

Two of India’s most admired consumer companies are learning a version of this lesson. Not from Greek soldiers, but from Instagram ads, Myntra listings and Shark Tank episodes. While the end-game is yet to be written and unlike in the case of Troy, the companies are well positioned to fight back, this example explains how post the unrecognised inflexion points, the rules of the game changed.

Consider two unrelated shopping decisions. A 26-year-old in Bengaluru buys his first pair of premium underwear. A 31-year-old in Delhi buys a new suitcase before a work trip. Five years ago, both of them had one obvious answer: Jockey for the first, VIP for the second. Today, neither of them reaches for that default and the financial statements of two publicly-listed companies are beginning to show exactly what that means.

This is not a story about failing incumbents. Page Industries, which licenses the Jockey brand in India, generated ₹4,935 crore in revenue last year. VIP Industries is Asia’s largest luggage manufacturer. Both companies are real businesses with genuine competitive advantages. What is changing is who gets the next customer. And in a market pricing these companies at premium multiples, the next customer is the only one that matters.

The brands that caused this did not arrive with lower prices. They arrived with better stories. XYXX built its identity around a single fabric distinction and found a consumer who had been waiting for exactly that conversation. DaMENSCH named its technologies and talked about sustainability. Technosport offered performance fabrics with UV protection that Jockey’s product line simply had no answer for. bummer made underwear feel like a fashion purchase. Together, these innerwear brands have crossed ₹820 crore in combined annual revenue from zero in seven years.

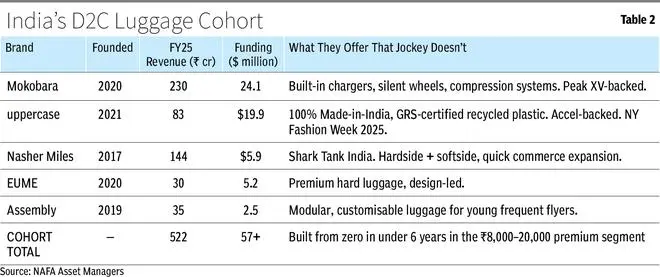

In luggage, Mokobara priced into the gap above VIP and below Samsonite, and filled it with built-in phone chargers, silent wheels and design language that made a suitcase feel like something worth owning rather than replacing. uppercase made Indian manufacturing its identity. The luggage cohort has crossed $57 million in under six years. Neither cohort undercut the incumbent. Both made it feel irrelevant to a specific, valuable consumer and that consumer was the one the incumbents were counting on for growth.

The pattern in both categories is identical. Find the premium buyer the incumbent has stopped trying to excite. Build a product story around fabric, sustainability or design, something beyond functionality. List on Myntra or Amazon, where the incumbent’s decades-built retail network is irrelevant because this consumer is scrolling, not walking into stores. Use venture capital to buy the marketing spend that would otherwise take a decade. Then expand offline but not through mass MBO chains, but through curated stores in Indiranagar and Bandra, where the product can be felt.

By the time the incumbent sees it in their own numbers, the D2C brand already owns the most valuable consumer in the category which are the young, urban, digitally-native and spending for the next 20 years.

The consequences are already written into Page Industries’ stock. Revenue stalled, distributor shelves piled up with unsold inventory, and the share price corrected from a peak of ₹53,500 to around ₹42,000. The more important number is the PE which halved from about 129x to about 55x. That compression is the market quietly revising how fast Jockey will grow from here. At 129x, investors were paying for a monopoly on the premium upgrade. At 55x, they are paying for a company that no longer has one.

The chart below makes the mechanism visible. As the D2C cohort scaled from 3.3 per cent of Page’s revenue in FY20 to 16.6 per cent in FY25, Page’s own five-year revenue CAGR which peaked at 19 per cent before these brands existed has settled into the 9-11 per cent band and stayed there. The timing is not coincidental. The growth rate step-down tracks almost precisely with the years the challengers crossed meaningful scale. The premium urban upgrade is now being split, and Page’s CAGR is the evidence the split is structural.

In luggage, the damage arrived faster and more bluntly. VIP’s net profit swung from ₹152 crore to a loss of ₹69 crore in just two years. Revenue fell even as India’s travel market recovered strongly.

The consumer who was supposed to graduate into VIP’s premium Carlton range, instead, searched ‘Mokobara’ on Instagram. That consumer was never counted in VIP’s churn data and they were never VIP’s customer to begin with. They show up instead on Mokobara’s revenue line, which went from ₹53 crore in FY23 to ₹230 crore in FY25. That is where the missing growth went.

The D2C share of VIP and Safari’s combined revenue has risen from 2.7 per cent in FY20 to 13.2 per cent in FY25 and the rate of gain is accelerating, not flattening. The CAGR panel tells the same structural story as Page’s: VIP and Safari’s combined five-year revenue CAGR ran at 14-16 per cent before the D2C brands were a meaningful force, and has settled in the 10 per cent band since the cohort began scaling seriously in FY23. The thesis is real but still being validated at scale.

Safari’s gains came from taking share from VIP in the economy and mid-market segment, not from competing in the premium tier. Safari’s stock, which peaked at about ₹3,100 in early 2024, has corrected to about ₹1,530. The D2C brands are not Safari’s present problem. They are its approaching one.

The incumbents have not been passive. VIP has launched premium sub-brands and upgraded its manufacturing. These are the right responses. They are also reactive ones, made after the D2C brands spent five years defining what premium looks like for a new generation of consumers. Jockey and VIP are now adapting to a product and brand language they did not write.

There is a more fundamental challenge that no strategic response fully resolves. Jockey means every man’s innerwear. VIP means every traveller’s luggage. That breadth is an enormous asset in tier-2 and tier-3 India, where the upgrade itself remains the aspiration. But in the premium urban segment, the highest-value, fastest-growing, most-visible slice of the market, breadth is a liability. A brand that means everything to everyone means nothing to the consumer who wants something that says something specific about them. That gap is what the D2C brands walked into, and widening it is precisely what their combined $180 million in venture funding is designed to do.

Page Industries will remain India’s dominant innerwear brand. Jockey is a category synonym in hundreds of millions of households, and no D2C challenger is within a decade of matching that scale. VIP and Safari will continue selling luggage to the vast majority of Indian travellers. None of this is existential.

But the markets that priced Page at 100x earnings and VIP as a compounder were not pricing those businesses. They were pricing the growth increment, which was the aspirational premium urban consumer who was supposed to graduate to these brands as incomes rose. That consumer, it turns out, has options now. Ten+ credible ones in innerwear. Five+ in luggage. More arriving every year.

The Greeks who hid inside the wooden horse did not need to outnumber Troy’s army. They did not need to breach its walls. They only needed to get inside and they needed the Trojans to be the ones who opened the gates.

That is what has happened here. Page and VIP built formidable businesses with real walls, real moats, real scale. But the D2C brands did not try to breach those walls. They arrived on a platform the incumbents did not control, in a language they did not speak, offering a story they had never thought to tell. And the consumer they were counting on wheeled them in.

Troy’s walls still stood the morning after it fell. They just no longer mattered. The question for investors is not whether Page and VIP will survive. They will. The question is whether the walls they built still protect the growth the market is paying for. Or whether the horse is already inside.

In understanding these factors lie answers to how today’s giants across sectors will fare as the rules of the game change.

Balaji Vaidyanath is the Head of NAFA Asset Managers and Abinash Swamenathan heads its research

Published on May 2, 2026

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。