Well over $2.5 trillion in investor wealth has been wiped out over the past week if one considers the major global equity indices alone. Wars are destructive, yet some pundits might sell the case today that wars are good for the economy and stock markets—as in the case of how the second world war helped the US drag itself out of an economic slump after the great depression. Government spending boosted economic activity, and the workforce was absorbed into well-paid military roles, keeping unemployment in check.

But not all wars are the same and at this juncture, nobody knows how the ongoing US-Iran war will play out. That said, can investors take cues from past wars and take portfolio decisions? We say, “No, Context matters.” For many reasons, this war needs to be viewed through a different prism versus other wars of the 21st century.

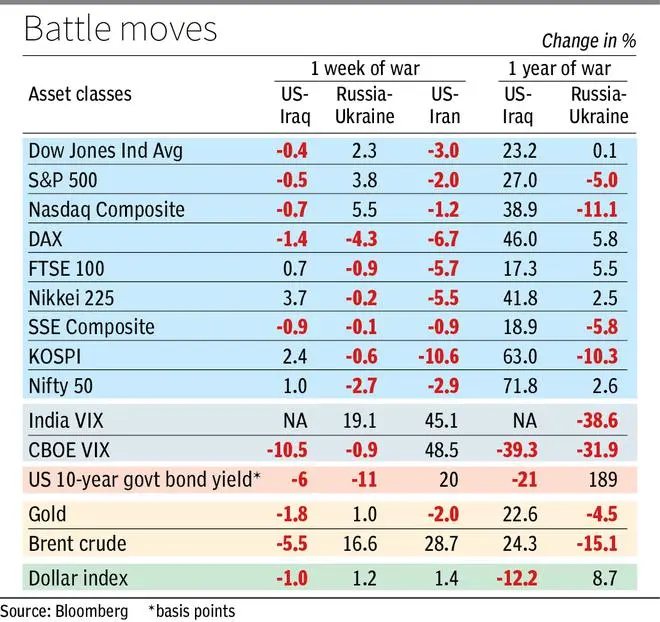

Week after war

Much analysis can be done to compare how stocks and other assets reacted to wars, but sometimes the most important indicator might lie in subtler movements. For example, the accompanying table compares how asset classes performed in the first week (five trading days) of war and how they evolved over the next year. We analysed this in the context of two major wars in the 21st century that involved crude oil spiking severely—the US-Iraq war of 2003 and the Russia-Ukraine war of 2022.

In the short term (one-week), if your guess is: oil and dollar gain while equities plunge, you would be largely right. As you can see from the table, equities have, broadly, taken the hit. In 2022 though, US indices ended the week oddly in the green, as the market saw the US to be impacted less relative to Europe (Europe was more dependent on Russian petroleum than the US was). As crude raced to $115 a barrel from $95, the US government announced release of strategic oil reserves, which could have comforted the market. This time around, all indices have closed the week in the red. Notably, Korean KOSPI saw the worst single-day decline (12.1 per cent) in its history—a record even the Asian financial crisis, dotcom bust, global financial crisis and the pandemic do not have.

Crude is up this time (29 per cent) as it did after Russia struck Ukraine (17 per cent). However, it fell 5.5 per cent in the week after the US-Iraq war began. Oil had hit a peak of $35 a barrel a few days before US invaded Iraq and had increased 52 per cent in the four months leading till then—a general strike in Venezuela to force the resignation of Hugo Chavez, being one of the key reasons. The market expected a quick success for the US in Iraq, explaining the 5.5 per cent drop in oil price. Oil then bottomed at about $23 before setting off on ascent to its all-time high of $148 by mid-July 2008.

While everyone may have noted all such big moves, today, probably the most important indicator lies in how the US’ 10-year bond yields have moved in the first week. In the previous two wars, the 10-year bond yields actually declined by 6 basis points (bps) and 11 bps in the first week after the war—a typical reaction when fear increases and investors take comfort in risk-free treasury bonds. However, this time, it has actually increased by 20 bps. With markets and bonds declining, investors fear uncertainty and inflation at the same time—there could be impact to the economy and jobs due to war, while at the same time, inflation too may increase and place the US Federal Reserve in a quandary.

Why it’s different now

One can argue that even after the start of the Russia-Ukraine war, inflation was high and US Fed was raising policy rates. So why should we be more cautious this time? Here are a few reasons.

For one, when the US Fed increased interest rates in 2022, while inflation was high, the impact of Covid stimulus was still providing support to consumption, jobs and the economy. This time, it is the opposite and if inflation were to increase due to higher oil prices now, it will be a double whammy. In fact, the US jobs data released last Friday revealed a weakening job market.

Two, in the past wars, oil-rich West Asian countries could profiteer by exporting crude at elevated prices. Petrodollars, in one way or the other, flowed back into the global economy either through their spending or sovereign wealth investments—driving some of the growth and market performance. This time, it’s different. Though prices are high, some of their refineries have been hit and it has become practically challenging to move crude out of the Persian Gulf due to the situation at the Strait of Hormuz. . Thus, the high prices are not of much benefit to them or to the global economy. If the war persists, they may even be forced to consider selling some of their global investments across markets and asset classes, to meet their budgets.

Three, valuations, as always, make a difference, especially when things are as uncertain as now. If you look at the one-year performance after the previous two wars, the one-year market performance is amazing at best (after US-Iraq war) and not scary at worst (after Russia-Ukraine war). But here are a few things to note.

The period 2002-03 was when the global economy bottomed out after the bursting of the dotcom bubble and slipped into a subsequent recession. Government debt to GDP was under control (US’ at 56 per cent by 2002 versus 125 per cent by 2025), central banks’ policy rates were low. At the start of the 2003 war, the P/E multiples were low—S&P 500’s at 18x and the Nifty’s at 14x.

In the year after the start of the Russia-Ukraine war, equities have given negative to marginally positive returns. When the war started, the P/E of S&P 500 and Nifty were 21x and 24x. This explains the weaker performance as compared to 2003-04.

Cut to today, the situation is complicated. Equities don’t exactly have a low base to build on. P/E multiples of S&P 500 and Nifty are at 26x and 23x respectively and are expensive. AI euphoria dominates US and Korean equities, while there is no clear idea how big AI disruption can get. Geopolitics is the hardest in decades. Global trade is in a flux (due to tariffs) and is yet to settle down.

To summarise: As the US-Iraq war began, markets were coming off low valuations and laying the foundation for a new bull run. In contrast, the Russia-Ukraine war erupted during an ongoing bull market. The current US-Iran conflict, however, has emerged at a time when markets are already showing signs of fatigue and valuations are expensive.

So, howsoever optimistic an investor might be, these are times to wait and watch and follow the news before making investing decisions. As Steve Eisman of ‘Big Short’ fame says, ‘there is no need to be a hero’—applies well when it comes to markets in today’s context.

Published on March 8, 2026