Gold loans have been growing at a healthy pace even in the phase when the yellow metal’s prices weren’t surging sharply. With the rise in gold prices in the past couple of years, the rise in gold loan business has grown even more strongly for banks and NBFCs.

In just the past one year to the December quarter of 2025, gold loan disbursements grew 94 per cent on-year to ₹8.16 lakh crore. Within this, the gold loan disbursements for NBFCs rose a whopping 189 per cent on-year to ₹2.53 lakh crore.

The relatively secure nature of gold disbursements, higher yields for lenders and relatively shorter tenors of loans have made these a focus for many banks and specialised NBFCs.

In this regard, Muthoot Fincorp, a leading NBFC in the space is coming out with an NCD (non-convertible debenture) issue with varied tenors and coupons. The company is looking to raise ₹200 crore, with a greenshoe option to retain a further ₹400 crore (aggregating to ₹600 crore in overall).

The issue is rated AA-/Positive by CRISIL, indicating very low credit risk and a high degree of safety in servicing interest and principal obligations.

In a situation where the war in West Asia shows no sign of an end and equities look shaky in light of the energy, business and supply chain disruptions the conflict has brought about, attractive bond issues may be worthwhile for investors.

Given the slow rise in inflation and with escalating global energy prices likely to translate to higher prices for domestic consumers eventually, it is likely that the bottom of the downward interest rate cycle may have been touched already.

Bonds and fixed-income instruments offering safety and higher-than-FD returns may be suitable for investors with moderate risk appetites.

Higher payouts

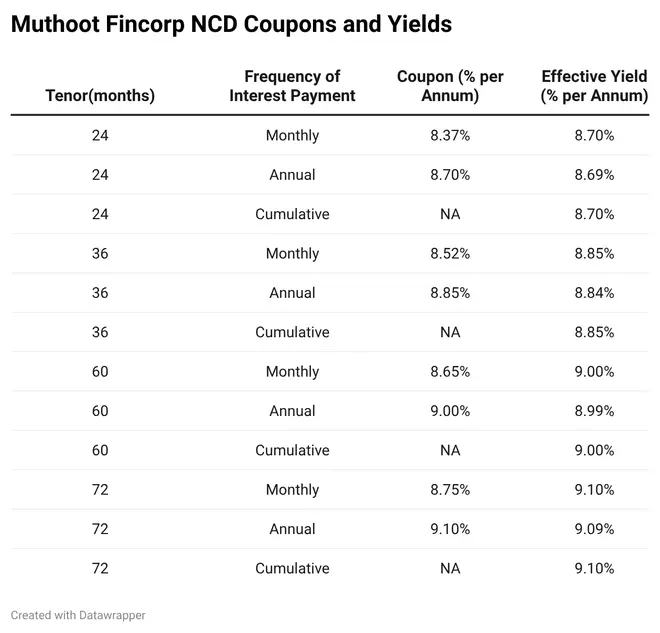

The Muthoot Fincorp NCD offers multiple tenors and payout options for investors. There are 24-month, 36-month, 60-month and 72-month tenors available.

Multiple coupon payment options exist. For each of these options there are monthly and annual interest payment choices and cumulative options as well.

The coupons for the monthly payout range from 8.37 per cent to 8.75 per cent, translating to yields of 8.7-9.1 per cent. The annual payout option gives similar yields as does the cumulative option.

Data from Kotak MF (Refinitiv) as on March 17, 2026 indicates that 1-year, 3-year, 5-year and 10-year AA-rated corporate bonds trade with a spread of 171 basis points, 146 basis points, 123 basis points and 77 basis points over corresponding g-secs of same tenor.

The Muthoot Fincorp NCD issue offers even higher spreads. The 3-year tranche (with annual payouts) offers 8.84 per cent yield (spread of 266 basis points), while the 5-year tranche offers 8.99 per cent yield (spread of 257 basis points).

For fixed income investors, these NCDs offer higher yields than the 5-year NSC with 7.7 per cent interest and cumulative payout and the 7-year RBI Taxable Bonds with 8.05 per cent interest (semi-annual payouts). Of course, NSC and RBI bonds must be accorded a much higher weightage in your debt portfolio.

The Muthoot Fincorp NCD issue is suitable for investors looking for higher yields with a tad more risk. However, it must only take a small portion of your fixed-income holdings as a diversifier.

Investors can consider the 24-month or 36-month option in this issue as they ensure reasonable payoffs. Longer lock-ins are best avoided, especially as we have dynamic interest rate scenario with interest rate rising and the possibility of rate reductions evaporating.

The monthly or annual coupon payout choices can be taken as those would ensure regular cash flows for investors rather than the cumulative option.

Sturdy financials

Muthoot Fincorp operates across 25 States in India including Union Territories. As of December 2025, the company had 3,757 branches.

The NBFC is mostly into disbursing gold loans, which account for almost 85 per cent of its lending book as of December 2025. Other products offered by the company include business loans to small businesses, loans against property and the like.

From the limited financials made available in the prospectus, the company does appear to have reasonably sound financial parameters.

While the loan book size grew at over 20 per cent over the past few fiscal years, the rise has been strong in 9MFY26. From March 2025 to December 2025, the loan book has grown 43.2 per cent, with gold loans leading the charge.

Despite the growth, the company has improved its asset quality steadily over the past few years.

The gross non-performing assets (GNPA) ratio has fallen from 2.11 per cent in FY23 (March 2023) to 1.34 per cent as of 9MFY26 (December 2025).

Muthoot Fincorp’s capital adequacy ratio is also healthy at 18.17 per cent as of December 2025, as against RBI’s mandate of 15 per cent for such NBFCs.

Overall, the company has been able to balance growth and asset quality reasonably well.

The issue is open till March 23. As of March 18, it is subscribed 112.64 per cent. With the green shoe option it is allowed to go up to 300 per cent.

Published on March 19, 2026