We had given a ‘hold’ call on the stock of Tamilnad Mercantile Bank (TMB) in late-July 2024. The price then was ₹463. Ever since, the stock broadly traded in a range until late-October last year. Fuelled by the management’s optimistic commentary after Q2 FY26 results in late-October, the stock started to climb to mark an all-time high of ₹720 by February 23, 2026—a return of 56 per cent in about one-and-a-half years at this point. Today, TMB shares trade 10 per cent lower than this all-time high. The bank’s financials have largely remained stable during this period, maintaining a healthy RoA at around 1.9 per cent.

Though delivering an RoA of a similar 1.8 per cent for FY24 and trading at an inexpensive valuation of 0.9x book value, we had given a conservative ‘hold’ call back then due to three reasons. One, the bank was being run without an MD at the helm and was instead run by a committee of executives. Two, loan growth was lacklustre relative to the banking system. Three, we had lower clarity on the financial impact of certain penalties imposed by the ED (Enforcement Directorate). These relate to a legacy case involving the bank’s issuance of bonus shares on holdings of certain non‑resident shareholders—the underlying transfer through which such shareholders acquired the original shares being alleged to contravene the Foreign Exchange Management (FEMA) law.

Now, there is improvement on all three aspects. The incumbent MD, a former SBI banker, was appointed late-August 2024 for three years. How things are looking up now on growth and the penalties is discussed in detail below.

However, the overhang from legacy litigations relating to shareholdings (as to who is the rightful owner) still remains. Today, the bank classifies about 9 per cent of outstanding shares as subject matters of court cases, in its shareholding pattern. When these cases are decided in the future, while they may affect the shareholders involved, they may not necessarily impact the bank’s financials. TMB is otherwise a professionally-run bank with no identifiable promoter. About 92 per cent of the shares are held by the public, with no investor’s stake surpassing 5 per cent individually.

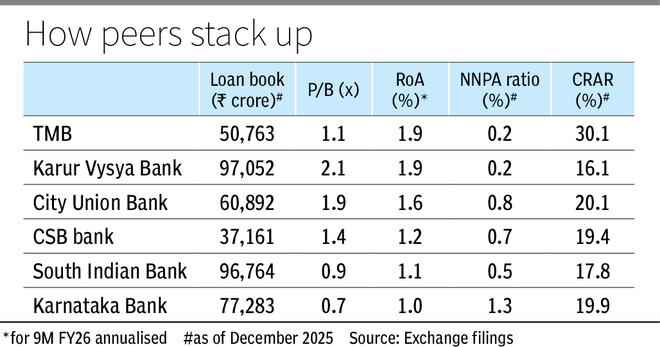

That said, at 1.1x book value and having delivered an RoA of 1.9 per cent (9M FY26 annualised), it still trades cheap relative to its regional private banking peers (see table). For instance, City Union Bank trades at 1.9x book value, but its RoA is a lower 1.6 per cent. Larger peer Karur Vysya trades at twice TMB’s multiple for an identical RoA and net NPA ratio. With growth back on track in the second half of FY26 and expected to continue into FY27, the risk-reward equation in our view, is favourable for an entry at current valuation. Hence long-term investors can accumulate the stock.

Before discussing growth, here is some context. TMB’s loan book amounts to ₹50,673 crore. Retail, agriculture, MSME and corporate segments share it in a 28:36:29:6 ratio. Almost 90 per cent of agri loans are jewel loans and about half of the retail loans are jewel loans as well. Thus, gold loans make about 46 per cent of the loan book (current loan-to-value ratio of 54 per cent). The other loans are backed by collateral too, as unsecured loans make a negligible 0.1 per cent of the book.

In FY24, credit growth was just 6.4 per cent against a system loan growth of over 20 per cent. It improved to 11 per cent in FY25, at par with the system (though a higher rate is desirable for its smaller size). Even in H1 FY26, credit grew at a slower 10.3 per cent vs the system’s 11.4 per cent. This is primarily due to a transformation exercise the bank is going through, with substantial upgrades to systems. Traditionally, the bank has been underwriting loans manually at the branch and this became an impediment to scale. Branch staff couldn’t focus on gathering deposits either. Deposit growth in FY24 and FY25 were mere 3.7 per cent and 8.4 per cent.

Now, the bank has set up region-wise credit management centres to handle the underwriting function. Branches would merely generate leads. However, underwriting of simpler gold loans and loans against deposits will still be with the branches. TMB is also modernising its software suite including loan origination and loan management (appraisal through post-disbursement stages) systems. These upgrades have largely come online, with residual implementation expected in FY27.

This meant, by 9M FY26, loans, deposits and net profit grew 16.3 per cent, 12.5 per cent and 18 per cent (adjusted for one-time recoveries from written-off accounts in 9M FY25). Profit growth in FY24 and FY25 were 4.2 per cent and 10.3 per cent, for context. Per its provisional figures for Q4 FY26, loans and deposit growth have further improved to 20.3 per cent and 14.9 per cent.

So far, the management’s guidance for FY27 stand as follows: Loan growth of 16-17 per cent, net interest margin to hold up between 3.8 per cent and 4 per cent (Q3 FY26 margin at 4 per cent; higher gold loan share and deposit repricing to aid) and a profit growth of about 20 per cent (plus or minus 3 per cent on either side). Given TMB’s 30 per cent concentration to MSME segment and the segment’s likely vulnerability to the ongoing West Asia conflict, investors need to track any changes to the guidance in the upcoming results for Q4 FY26.

With only secured exposure, the bank is otherwise stable with a capital adequacy ratio of 30.1 per cent, gross and net NPA ratios at 0.9 per cent and 0.2 per cent, with contained slippages and credit cost. With MSME loans ramping up, the segment’s slippages might rise but not too much to move the GNPA ratio beyond 1.25 per cent, per the management. Further, the bank is also not likely to be materially impacted by the upcoming expected credit loss and liquidity coverage norms.

The genesis of the penalties traces back to 1994, when shareholders holding two-thirds of the bank’s shares had sold their shares to the Essar group. The RBI declined to recognise this transfer, as it disfavoured links between banks and industrial houses. Hence, the Nadar Mahajana Bank Share Investors Forum was floated to identify willing investors to buy the stake back. In 2007, about half of such shares were transferred to 216 investors, which include seven non-resident entities. Transfer of shares to these seven entities was in contravention of FEMA and thus, forms the bone of contention.

In FY17, the bank decided to issue bonus shares (1:500 ratio), as the book value per share reached close to ₹1 lakh. Since bonus shares were issued against those whose transfers were in contravention of law, the ED shot notices to the bank with penalties totalling to ₹1,037 crore in FY18. An appeal has been lodged against this, and the case is still pending. The penalties work out to about 10 per cent of net worth. However, the bank has obtained legal opinion and according to it, the maximum penalty applicable if the alleged offence is established is ₹2 lakh. This is because the matter involves only the issuance of bonus shares, with no actual funds received against their allotment.

Published on April 26, 2026

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。