The ₹1,907-crore IPO of 10-year-old third-party logistics (3PL) provider Shadowfax Technologies opens on January 20 and closes on January 22, with the upper end of the price-band fixed at ₹124/share.

The fund-raise comprises a fresh issue and offer-for-sale (OFS). The fresh issue of ₹1,000 crore (up to 8.06 crore shares) will be used in capex for network infrastructure (₹423.4 crore), funding of lease payments (₹138.6 crore), branding, marketing and communication costs (₹89 crore) etc.

The OFS of ₹907 crore (up to 7.32 crore shares) is by early backers such as Flipkart Internet, Eight Roads, IFC, Qualcomm etc.

Post-issue, the company’s implied market cap will be around ₹7,169 crore. On a post-issue basis (adjusting for the cash raised), EV/sales (last 12 months) works out to 1.8x versus larger and more profitable peers such as Blue Dart (2.3x) and Delhivery (3.2x). Shadowfax’s EV/adjusted EBITDA multiple of 77x vs. Delhivery’s 68x and Blue Dart’s 14.8x is expensive because of slim current profitability.

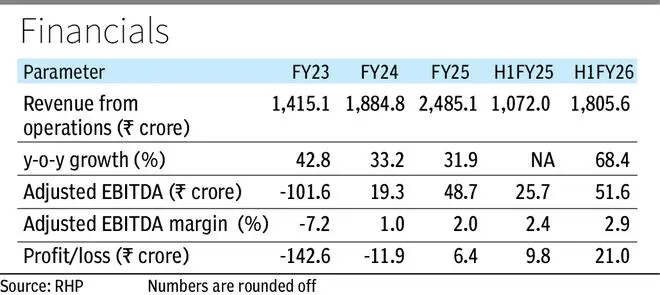

Shadowfax sits in a sweet spot between e-commerce and hyperlocal delivery, but profitability remains thin. After losses in FY23 and FY24, it turned profitable in FY25. But its operating leverage is tentative and not yet durable.

With mid- and small-cap stocks under pressure, the environment favours caution over aggression. Shadowfax is better treated as a watch-list candidate for long-term investors, tracking whether profitability sustains before considering entry later.

Previous post-listing experiences in the broader logistics sector shows that TVS Supply Chain (2023), Delhivery (2022) and Mahindra Logistics (2017) are all trading about 20-40 per cent below their respective IPO price.

Business

Say, a customer in Chennai orders a product from a seller in Srinagar on an e-commerce platform. If Shadowfax is the logistics partner, it can handle the first-mile by picking up the parcel from the seller and taking it to a local sorting hub in Srinagar. The mid-mile is the movement from Kashmir to Tamil Nadu through its line-haul network and destination hubs. The last-mile is the doorstep delivery in Chennai through local delivery partners. Last-mile is typically the costliest leg, given the tight delivery timelines, failed deliveries, returns and cash-on-delivery handling.

On-demand hyperlocal delivery runs on tight service pacts. Economics hinge on batching, peak-hour surge, rider utilisation, cancellations, incentives and refunds or returns handling.

Shadowfax straddles e-commerce express orders (68.6 per cent of H1FY26 revenue) and hyperlocal orders (quick commerce / food delivery: 19.9 per cent) and other logistics services such as critical logistics and dark-store operations (11.5 per cent). It is a blend designed to cross-utilise riders and fleet between platforms. It has over 2.05 lakh average quarterly unique transacting delivery partners.

Average revenue/yield per order in ‘express’ rose from ₹49 to ₹54 (10+ per cent), whereas ‘hyperlocal’ stayed flat (₹54). That hints at pricing or mix improvement in ‘express’.

The business model is asset-light in form (doesn’t own a lot of hard assets) but network-heavy in cost. As of September 30, 2025, Shadowfax had 4,472 permanent employees and 17,182 contractual staff.

Shadowfax handled about 29.4 crore shipments in H1FY26, up 50 per cent from the year-ago period. Its pin-code reach (14,750+) is still narrower than larger peers, reflecting a network still expanding.

According to Redseer, the company’s share in India’s 3PL e-commerce shipments surged from 8 per cent in FY22 to 23 per cent by H1FY26. It also has India’s largest crowd-sourced last-mile delivery fleet and is the leading player in same-day and reverse-pickup segments, as per the report.

Costs & risks

Shadowfax’s scale is impressive, but dependence is steep. Revenue generated from the largest client (Meesho) was nearly 49 per cent and top-10 customers accounted for 84 per cent of revenue. It discloses Meesho, Flipkart, Myntra, Swiggy, Bigbasket, Zepto, Nykaa, Blinkit, Kartrocket, Zomato, Uber, Pincode, Purplle, Licious, ONDC, Magicpin as clients. Any slowdown or renegotiation by these platforms can meaningfully dent both volumes and yields. Many of these clients are themselves loss-making.

The critical investor question is whether fast growth is producing any operating leverage. Total expenses (up 67 per cent) grew almost in step with revenue (up 68 per cent) in H1FY26. Partner payouts plus transport charges stayed around 71 per cent of revenue (vs 72.6 per cent in H1FY25). A mild efficiency gain is visible but offset elsewhere: “Lost shipments” expenses almost doubled to 8.2 per cent of revenue from 4.4 per cent. The combination implies logistics density is improving, yet service leakage is eroding that benefit; this is a classic early-scale stress.

Adjusted EBITDA is calculated from EBITDA (excluding other income) after deducting rent expense in lieu of Ind AS 116 leases, and adding back share-based payment expense and one-time return to seller (RTS) cancellation fees. That number for H1FY26 was ₹51.56 crore (2.86 per cent margin) against ₹25.67 crore (2.39 per cent) a year ago. However, this includes a one-time RTS cancellation fee. Excluding that fee, the adjusted EBITDA margin is about 2.47 per cent, implying the year-on-year margin uptick is marginal.

For context, asset-heavy Blue Dart runs adjusted EBITDA margin of 15 per cent, enterprise-focused TCI Express 9-10 per cent and asset-light peer Delhivery (4-5 per cent), which recently acquired Ecom Express. This shows how narrow the realistic ceiling is for new-age 3PLs.

Cash conversion has improved. Net operating cash flow was ₹141 crore in H1FY26 (vs ₹57 crore a year ago), aided largely by an increase in payables and other liabilities. The company still needs to show this is durable cash discipline, not just working-capital timing.

Delhivery is about 2.9 times larger by revenue, but its adjusted EBITDA margins are only twice as high, showing how long the path to solid profitability could be.

Even if Shadowfax’s revenue grows 40 per cent for full FY26 and 30 per cent in FY27, expanding adjusted EBITDA margins from about 2 per cent (FY25) to 3 per cent is tough work in logistics. At an EV of about ₹5,759 crore, the company valuation will still imply roughly 42x EV to FY27-adjusted EBITDA.

With current margins in a low range, even a 0.5 percentage-point cost swing can shave roughly 15-25 per cent off EBITDA. Hence, ‘lost shipment’ expenses and returns management need tightening for margin expansion to hold.

The growth runway is real for India’s 3PL market. Per Redseer, quick commerce is forecast to grow by 50-62 per cent CAGR till FY30. E-commerce’s projected run-rate is 15-20 per cent CAGR.

Shadowfax has shown it can capture share quickly and has execution credibility in same-day delivery and reverse logistics. But the business is smaller than larger peers, has thinner margins and nascent operating leverage. Solid and durable profitability will take several quarters of tight execution, and any disappointment will not be overlooked by markets.

Published on January 17, 2026