The insurance sector is in the spotlight with the Parliament clearing a Bill which allows 100 per cent FDI. Adding to the tailwind, the recent GST exemption on individual life policies has also lifted sentiment for the segment. However, listed private-sector life insurers have been a tad weak in the past week in sync with the overall broader market trend.

In this backdrop, we remain positive on ICICI Prudential Life Insurance, promoted by ICICI Bank and Prudential Corporation Holdings. bl.portfolio had recommended subscribing to its IPO (offer price ₹334) in September 2016, and reiterated a positive view in August 2020 when the stock was around ₹460.

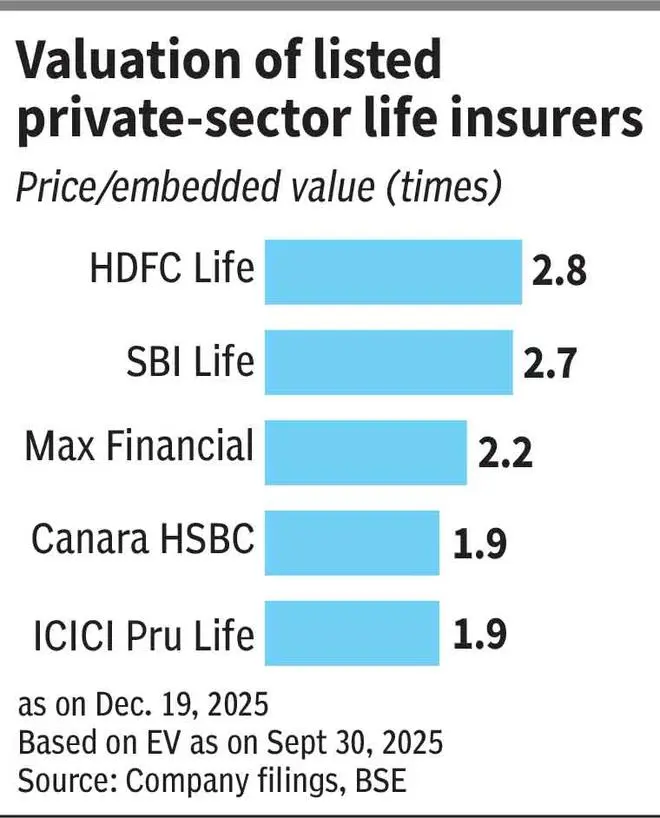

ICICI Prudential Life is best judged on price-to-embedded value (P/EV), which captures the insurer’s net worth plus the present value of profits expected from its existing book. At CMP of ₹651, the stock trades at about 1.9x P/EV, well below HDFC Life and SBI Life’s 2.7-2.8x (see valuation table), but the discount is partly earned: Growth has been uneven at times, the mix has carried a higher share of market-linked business in some phases and costs have remained relatively elevated, limiting operating leverage. Even so, if execution improves and embedded value compounds steadily, a partial narrowing of the valuation gap can be on the cards.

In the last one-year period, the stock has trended down, lagging decent jumps in SBI Life and HDFC Life. This leaves ICICI Prudential Life priced for pessimism even as the operating narrative is slowly improving: the mix is shifting toward steadier, higher-margin segments and cost actions appear more durable than a one-quarter clean-up. If growth revives without margin slippage, a gradual re-rating is possible. Thus, investors can accumulate on dips.

What needs to go right

Our positive stance on ICICI Pru Life is conditional on three levers that need to go right.

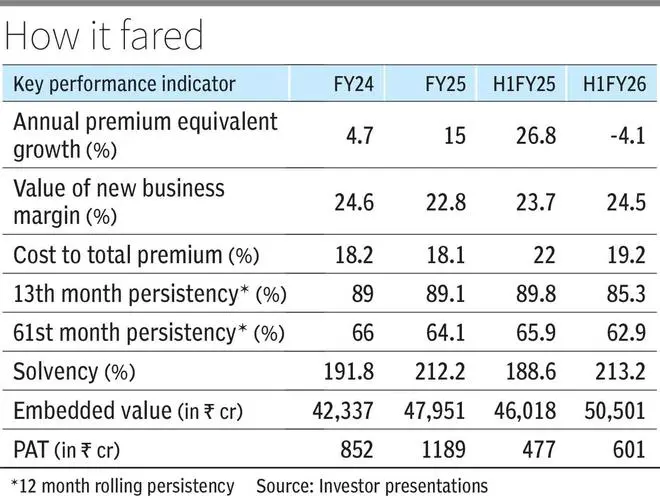

Mix upgrade: The company’s mix appears to be moving towards non-linked / steadier products. This matters because of the improvement in margin stability and embedded value compounding. As on H1FY26, the product mix had 48 per cent in linked products, 22 per cent in non-linked products, 19 per cent in protection (non-linked), 6 per cent in group funds and 5 per cent in annuity (non-linked). In comparison, the linked business accounted for 52 per cent in H1FY25.

The non-linked savings business grew 11.9 per cent year on year in Q2FY26 and 15.6 per cent in H1FY26, as customers preferred to invest in non-par products to lock in high yields in the declining interest rate scenario. Linked business declined 8.6 per cent in Q2 and 10.7 per cent year on year in H1 this year.

Overall protection business was almost flat year on year in Q2FY26 and for H1FY26 the business grew 6.7 per cent year on year, with retail segment rising at a faster clip.

Cost discipline: The company’s cost/total premium has declined 280 basis points (bps) to 19.2 per cent in H1FY26 from 22 per cent in the year-ago period. Cost to premium for savings line of business also reduced 280 bps to 12.7 per cent in the same period.

Apart from digitalisation, ICICI Pru Life has been undertaking various cost optimisation initiatives to make its cost structure leaner and aligned to the product mix. With IRDAI expected to tighten commission caps under the new regulations, ICICI Pru Life’s distribution costs could ease.

Note that while GST input tax credit being disallowed might have some short-term impact on profitability, the opportunity arising from the same in terms of market expansion is quite large, as per the management.

The company has no internal preference for product mix and usually follows customer demand. When ULIPs are in favour, they lean into it; when markets turn volatile, they can pivot to guaranteed offerings. Because savings products form a large share of business, cost discipline is the main profitability lever and this keeps expense ratios aligned to the mix.

Growth revival with quality: The weak spot for ICICI Pru Life is that growth has been patchy. Though sector demand has improved post the GST exemption, but ICICI Pru’s growth still needs to prove consistency. For instance, annual premium equivalent for H1FY26 saw a decline of 4.1 per cent on a high base of 26.8 per cent growth in previous year H1. The two-year APE CAGR stood at 10.3 per cent.

In November 2025, while its retail-weighted received premium grew 13.2 per cent year on year, its APE was virtually flat at 0.5 per cent. This kind of month-to-month unevenness has shown up before. This is why the stock still trades at a discount, as the market wants evidence of sustained, profitable new business growth, not just better sentiment. Quality growth, in this context, means improving persistency, a healthier product mix and cost discipline, not just pushing volumes.

Investors should track a simple scoreboard (see table below for numbers so far): APE growth, the direction of VNB (value of new business) margin, cost/premium ratio, persistency (13-month and 61-month) and the solvency ratios.

Risks

The key risk is that ICICI Pru Life’s growth revives only by “buying” business — higher commissions, distribution payouts or marketing spend that push cost ratios back up and dilute profitability.

A second risk is mix reversal: In strong equity markets, ULIPs can regain dominance, making margins and earnings more cycle-dependent and weakening the case for a steadier, non-linked tilt.

Third, if persistency does not improve meaningfully, embedded value growth will remain slow, keeping the valuation discount intact. Persistency softened as on H1FY26.

Finally, sector tailwinds may not translate quickly. For instance, GST and FDI headlines can lift sentiment, but do not automatically raise near-term earnings.

Published on December 20, 2025