We had originally given an ‘accumulate’ call on HDFC Bank in July 2024 when the stock was trading at ₹809 (adjusted for bonus issue). Till date, on a point-to-point basis, it has underperformed Nifty Bank with a return of -5.3 per cent while the benchmark’s return measures 6.2 per cent during the same period. This is despite the bank’s resilient performance in FY25-26, having maintained industry-leading asset quality.

Part-time Chairman Atanu Chakraborty’s unexpected resignation in mid-March, citing a cryptic cause — certain practices of the bank had not been in congruence with his personal values and ethics, came as a shocker, given the bank’s systemic importance. Since then, HDFC veteran Keki Mistry has stepped into the role, though temporarily, while the bank has appointed law firms to review the former Chairman’s resignation letter. These developments, among other factors, have weighed on the stock despite the RBI assuring stakeholders that there are no material concerns. Uncertainty over the appointment of the next Chairman and the successor to the current MD & CEO Sashidhar Jagdishan, whose term ends in October 2026, remains an overhang on the stock.

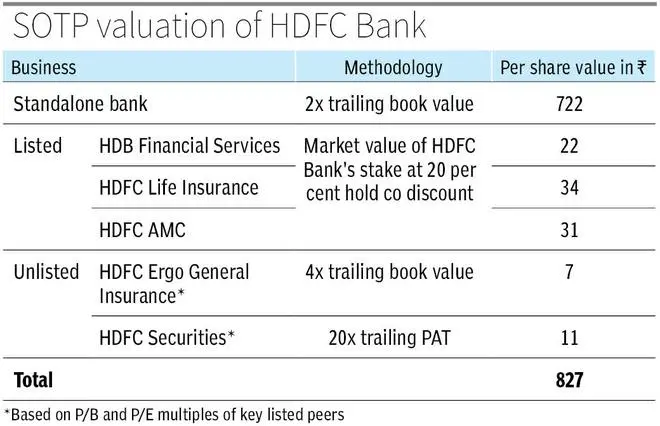

Nevertheless, the bank’s solid fundamentals (FY26 RoA at 1.9 per cent) and the RBI’s reassurance make the recent weakness an opportunity for long-term investors to accumulate the stock at current levels. At ₹766, HDFC Bank trades at about 2x trailing consolidated net worth, a sharp discount to the 2.6x multiple in July 2024 (FY24 RoA at 2 per cent) and 3.9x five years ago. Our conservative sum-of-the-parts valuation is around ₹830, implying an 8 per cent margin of safety. Even without a rerating, growth in book value should support returns. For context, in FY26, the group’s net worth rose 12.3 per cent. With the macro environment likely to remain weak and banks set to directly bear the brunt of any stress, quality large banks are positioned to fare better.

In FY25, the standalone bank (accounts for about 93 per cent of group net worth) recorded a profit growth of 10.7 per cent. Deposits grew 14.1 per cent, while gross advances grew 5.4 per cent. The bank moderated loan growth to reduce its elevated credit-deposit (CD) ratio, a legacy of the merger with erstwhile HDFC Ltd. The ratio was brought to 97 per cent as of March 2025 from 108 per cent, a quarter after the merger (Q2 FY24).

With the CD ratio easing, the bank shifted back into growth mode in FY26. Advances rose 12 per cent to ₹29.6 lakh crore, while deposits increased 14.4 per cent to ₹31 lakh crore, bringing the CD ratio further down to 95 per cent. While deposit growth exceeded that of the system’s (all commercial banks combined) 13.5 per cent, loan growth trailed the system’s 16 per cent. The management remained cautious on loan growth, viewing the system growth as disproportionate to a likely nominal GDP growth of 9-10 per cent (for FY26), making the bank potentially vulnerable to future delinquencies, if it were to pursue aggressive growth. System credit growth generally happens to be 1-1.2x nominal GDP growth.

Going forward, the bank may not strictly target the CD ratio for advances growth, but may rather let the LCR (liquidity coverage ratio: measures whether the bank has enough liquid assets to survive a 30-day stress scenario; regulatory minimum of 100 per cent), NSFR (net stable funding ratio: simply put, measures whether the bank has enough long-term funds (including deposits, bonds and equity; maturing after one year or beyond) to fund long-term assets of equivalent tenor; regulatory minimum of 100 per cent) and CAR (capital adequacy ratio; regulatory minimum of 11.7 per cent) to guide its strategy. The relevance of these ratios over the CD ratio was echoed by the RBI Governor in a recent press conference as well. As of March 2026, HDFC’s LCR, NSFR and CAR stood at healthy levels of 114 per cent, 118 per cent and 19.7 per cent respectively.

Profit, in FY26, grew 10.9 per cent leading to an RoA (return on assets) of 1.9 per cent — as high as in FY25. Asset-quality metrics do not signal any near-term stress. Gross and net NPA ratios are at 1.2 per cent and 0.4 per cent. Credit cost and slippage ratio are contained under 50 bps and around 100 bps respectively. The bank’s standard assets provisions and other contingency provisions stand at around 1.7 per cent of the loan book.

HDFC’s listed subsidiaries (see table) recorded mid-teen profit growth for the year, while HDFC Ergo posted 62-per cent growth. That of HDFC Securities declined 18 per cent.

While the bank’s fundamentals remain strong, it may not be smooth sailing in FY27, and investors need to watch out for the following near-term headwinds.

Corporate loan (27 per cent of the loan book) growth, which has been muted for a few quarters, picked up in H2 FY26. The segment grew 13 per cent in FY26 against a 3.6 per cent decline in FY25. Corporates, which earlier found bank rates expensive, are now tapping bank loans again. Further, the business banking segment (loans to MSMEs; 15 per cent of the loan book) has been a key engine of growth in recent quarters. In FY26, the segment grew 20 per cent. Given macros could turn challenging in FY27, the management has expressed its cautious stance on these segments. This can impact loan growth and thus trickle down to lower earnings. It is also prudent to factor in some degree of rise in defaults and credit cost, especially driven by MSME, agri and commercial vehicles segments, as they are more vulnerable to macro jitters. However, if the past is any guide, the bank got through the pandemic quarters without any meaningful spike in gross NPA ratio.

Moving on to margin, NIM (net interest margin) stood at 3.5 per cent for Q4 FY26 — only at a 10-bps discount to that for Q3 FY25, the quarter before the RBI started cutting rates. Both yield on assets and cost of funds have undergone an equal 50-bps cut between these two quarters, implying that the repricing cycle on both advances and deposits may be largely over. Deposit repricing may still have some legs, probably continuing into FY27, going by the management’s assessment. If that be the case, NIM could improve a bit. However, one has to consider this.

Deposit mobilisation has been challenging in the last few months, brought about by system credit growth outpacing deposit growth, among other causes. Rates have hardened to stay competitive. This is evident from the system-level weighted average domestic term deposit rate for fresh deposits having undergone a mere 50-bps drop since the RBI’s rate cuts (125 bps cumulatively) started in February 2025 as against a 100-bps drop in weighted average lending rate on fresh loans. Things could get complicated if the RBI raises policy rates in one of the upcoming MPC meetings. However, if that were to happen, about 60 per cent of the HDFC’s loan book linked to external benchmarks (repo rate, T-bill rate) would reprice immediately, padding the margin. The net impact of these opposing forces on margins remains to be seen.

Published on May 23, 2026

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。