Global Health, which operates the premium hospital chain Medanta, is well-positioned for growth over the next three-four years, supported by its established hospitals and upcoming capacity additions. The stock is currently trading at 46x one-year forward earnings, in line with its five-year historical average and broadly comparable with peers. While the valuations are not cheap, corrections can provide opportunities at lower valuation levels. This is given the fact that the sector has many structural drivers of strong demand, a modest pricing lever and underpenetrated market. Hence we recommend that investors accumulate the stock on dips based on three key factors: Sustained growth in the hospital industry, driven by volume and pricing; limited impact of global uncertainties on operations and expansion plans; and Medanta’s ability to drive growth through improved efficiencies and network expansion.

The company has its flagship hospital in Gurugram (1,440 beds), and later expanded to Indore (175), Ranchi (310), Lucknow (950), Patna (650), and Noida (550) — operationalised in November 2025.

The portfolio can be viewed as mature hospitals: Gurugram, Indore and Ranchi – the ones with more than six years of operations, and developing hospitals: Lucknow, Patna and Noida.

The company plans to increase bed capacity by 13 per cent in FY27 through additional beds at Indore, Lucknow, Noida and Patna. The Indore expansion will be supported by an acquired unit located near Medanta Indore, while the other three, being relatively newer facilities, will continue to scale within their existing infrastructure. Medanta will also introduce the remaining departments across these units. For instance, departments such as Pediatrics, Obstetrics, Liver Transplant and Oncology in Noida . Importantly, the FY27 bed addition is neither a greenfield nor a conventional brownfield expansion, but rather an expansion of services within existing infrastructure, with support and clinical staff already in place. Consequently, this capacity addition is expected to accelerate volume growth faster than a new unit and support margin improvement through better asset utilisation.

The company can supplement the low double-digit volume growth expected in near term with 4-6 per cent year-on-year growth in realisations or ARPOB (average revenue per bed). Recently, CGHS (Central Government Health Scheme) has revised rates and this will imply upward revisions in other government or PSU-sponsored schemes, which together (CHGHS/ECHS/Railways and PSUs) account for 36 per cent of FY26 revenues for Medanta. The improved product mix in new hospitals, private insurance periodic revisions, improving international patient mix (7 per cent of FY26 revenues) are other levers to support modest growth in ARPOBs.

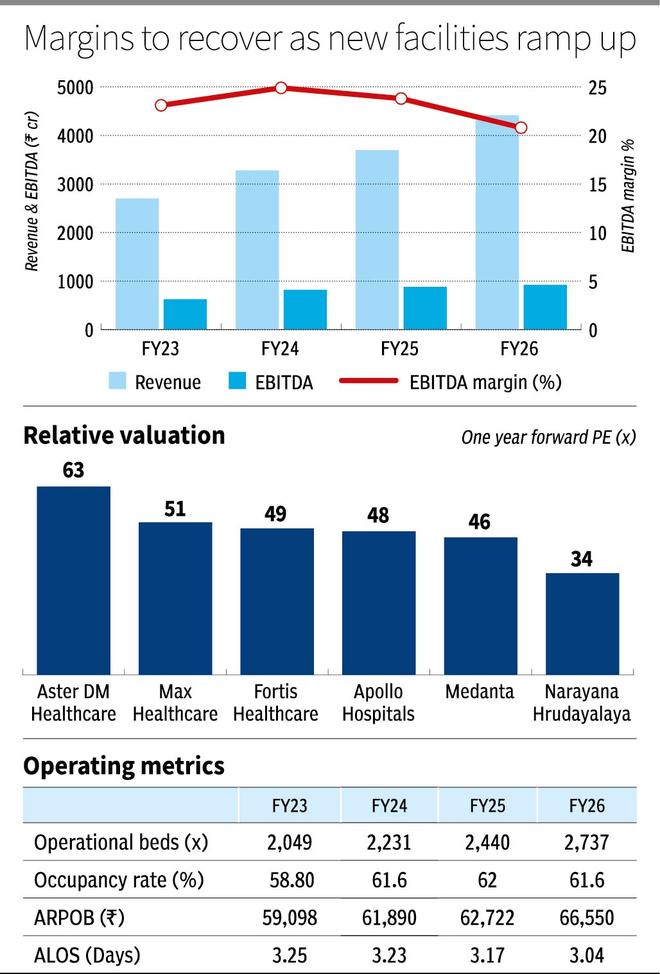

On the profitability front, while Noida is expected to break-even in FY27, the profitability of developing and mature units is expected to improve. Medanta improved its ALOS (average length of stay) from 3.8 days in FY22 to three in FY26. A shorter stay has a strong impact on financials. Asset utilisation improves, as also ARPOB. The latter benefits as bulk of the revenue are front-loaded. ALOS can further improve as the low-hanging fruit — developing hospitals improve their efficiency. Even in mature or developing units, a higher employment of robotic minimally-invasive surgeries are driving a shorter stay across the hospital industry, which will benefit Medanta as well. As shown in the figure, EBITDA margins of the company have been impacted by losses from Noida and other units, but can improve on higher utilisation.

For FY30, Medanta is targeting a bed capacity of 6,855 compared to 3,665 in FY26. This is an accelerated target compared to FY24-26 — bed capacity growth of 13 per cent CAGR compared to 17 per cent CAGR growth by FY30. This includes 400 beds in South Delhi in partnership with DLF. A 750-bed unit in Pitampura, Delhi, which is jointly developed, and a 400-bed unit in Varanasi under a lease agreement with a partner. Medanta will be independently developing a 750-bed unit in Mumbai and a 400-bed unit in Guwahati, Assam. The projects are in early stages of development and will take three-four years to commercialise. The company has estimated a capex plan of ₹4,500 crore for the next five years. Medanta has a current net cash position of around ₹600 crore, with reported operating cash flow of ₹573 crore in FY26. It should finance most projects largely from internal accruals, while it has also indicated debt for some.

The company reported revenue of ₹4,410 crore in FY26, a 18 per cent CAGR growth in revenues in FY23-26, as shown in the figure. But EBITDA growth in the period at 14 per cent CAGR was lower. With the addition of developing facilities, especially Noida, the EBITDA margin declined from 24 per cent in FY25 to 21 per cent in FY26. But with a strong RoE of 15 per cent, the company should add value from its unit additions in the long term.

Medanta’s growth outlook employs existing infrastructure and new capacity expansion. It has experienced strong growth in Lucknow and Patna facilities, which should be evident for Noida unit as well. The long-term development plan also balances own and partnered projects for a relatively-derisked expansion plan.

Published on May 23, 2026

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。