The year 2026 has begun on a rough note for the markets. Geopolitical tensions have resurfaced (US-Venezuela), no deal in sight to address the trade tariffs levied by the US on India and FPI outflows continue unabated. Inflation trending above target in a few developed economies and central bank rate actions are also adding to the uncertainties.

As the environment calls for a cautious approach, relatively safer equity investments may be suited for investors. Real estate investment trusts (REITs) fall in the category as they are not exposed directly to residential real estate vagaries and operate in the more sticky and reliable commercial leases space, as they collect rentals with steady prospects for periodic increases. They are also required to distribute at least 90 per cent of their net distributable cashflow. Recently REITs were re-categorized as equity from debt earlier by market regulator SEBI.

As a key player in commercial leasing space in malls across top cities in India, Nexus Select Trust is a beneficiary of increasing footfalls and consumption over the past few years in malls that it operates.

Rising footfalls in key urban consumption centres, high lease occupancies, healthy increases in rentals and relatively-long weighted average lease expiry are all positives for the trust.

At ₹159, the Nexus Select Trust (REIT) trades at 0.88 times its likely September 2026 NAV (net asset value) per unit. The distribution per unit is expected to give a yield of 5.5 per cent in FY26 and more than 6 per cent in FY27 at current unit price. Almost 72 per cent of this payout is tax free. On a post-tax basis, the yield is higher than most bank deposits, especially for those in the higher brackets. REIT payouts suffer very low taxes as these are of the nature of dividends, and interest and debt repayments.

Most other REITs are trading at or higher than their NAVs. The NAV is nothing but the per unit market value of a REIT’s properties, assets minus its liabilities.

Given reasonable dividend yield and the scope for modest capital appreciation (a little less than 10 per cent CAGR in the last two years) make Nexus Select Trust a good investment prospect for investors with perspective of three years or more.

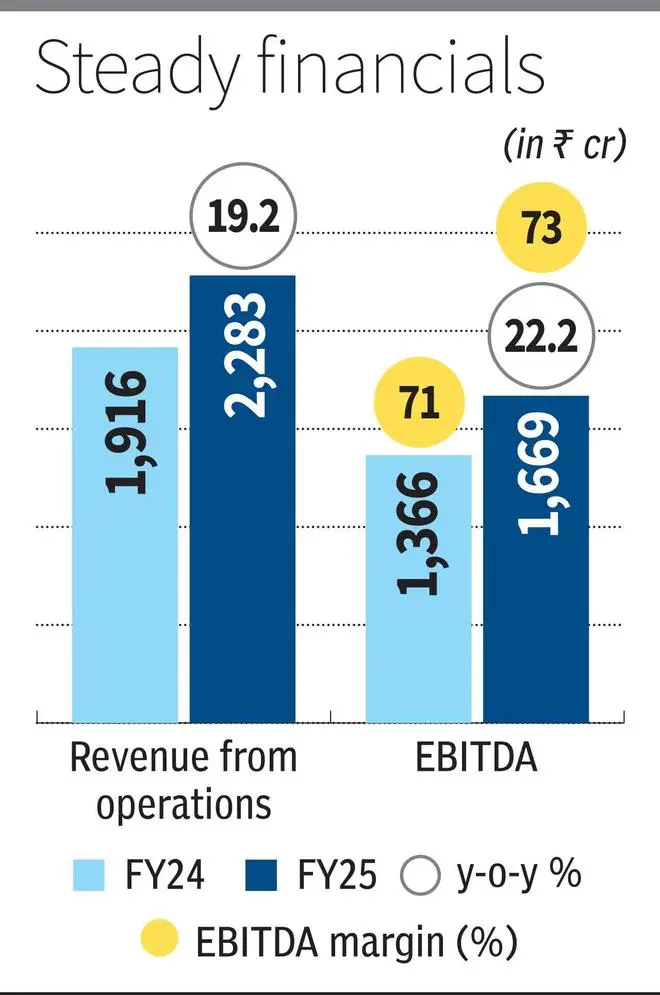

In FY25, the REIT’s revenue from operations grew 19.2 per cent over FY24 to ₹2,283 crore, while its EBITDA grew 22.2 per cent over the same period to ₹1,669 crore. In H1FY26, the REITs net revenue grew 12.3 per cent year on year to ₹1,244 crore, while EBITDA rose 12.2 per cent to ₹893 crore.

Consumption beneficiary

Nexus Select Trust operates across 15 cities in 19 consumption centres. Key cities where it has strong presence include Delhi, Navi Mumbai, Chandigarh, Ahmedabad, Hyderabad, Chennai and Bengaluru, among others.

Its retail portfolio has 10.6 million sq ft area as of September 2025. The trust’s properties had a footfall count of over 133 million in the last 12 months ending September 2025.

More than 3,000 retail stores across thousand-plus brands are part of Nexus Select Trust’s retail portfolio.

Some of the key clients at its properties across cities include PVR-Inox, Trent, Lifestyle International, Aditya Birla Fashion Retail, Reliance Luxe Beauty, Decathlon Sports, H&M, Addidas India, Max Hypermart, Shoppers Stop, Reliance Retail etc.

Recent international brand additions to its retail outlets include Gucci, Foot Locker, Nespresso, Prada Beauty and Cos.

It is important to note that the trust has a very high occupancy level across its properties.

The overall occupancy in its consumption centres was 96.9 per cent as of September 2025.

In its key assets in the top cities, the occupancy levels range from 94 per cent to as high as 99 per cent, which is among the best in the industry.

The rents at important retail properties range from ₹104 to as high as ₹457 per sq ft per month, which again compares with the highest in the segment.

Consumption revival is clearly indicated in its retail portfolio. In H1FY26, in its retail stores in categories such as fashion, jewellery, beauty & personal care, entertainment and electronics, consumption has increased 13 per cent year on year to ₹6,760 crore for its tenants.

A key metric WALE (weighted average lease expiry), which indicates the lease term remaining on an average, is strong at 4.7 years for its retail portfolio.

Around 11-17 per cent of its gross rentals are expiring over FY27-29. The re-leasing spread for the portfolio of expiring leases is expected to be as high as 20 per cent.

The trust also operates in the hospitality and office spaces, which together account for 9 per cent of its gross asset value.

Hyatt Regency in Chandigarh that it operates has 70 per cent occupancy and healthy double-digit growth in revenues and EBITDA.

Westend offices in Pune has 88 per cent occupancy and is also growing at a healthy clip and has a WALE of 3.1 years.

All these figures are as of September 2025.

Healthy financials

Nexus Select Trust has a loan to value (GAV) of just 18 per cent as of September 2025. Many peer REITs have LTV in the mid-20 or early-30 percentage. The average cost of debt has fallen from 8.3 per cent to 7.5 per cent over the past couple of years. Interest coverage ratio is strong at 4x as is net debt to EBITDA at 2.9x. The gross debt stood at ₹5,800 crore as of September 2025.

Published on January 11, 2026