With two innovative medicine launches underway in the US and a third expected in the next one year along with generic Semaglutide launch in India, Sun Pharma is positioned well across geographic segments. The company has gradually strengthened its innovative portfolio, which now accounts for 25 per cent of Q3FY26 sales. Detailed primer on pharma products can be read here. This has supported an EBITDA margin expansion of 450 basis points in the last five years. With a pipeline of assets, the segment should support the improved margin profile, cash-flow prospects and pricing power, compared to Indian peers. This is captured in the valuations at 31 times one-year forward earnings compared to Nifty Pharma at 28.5 times or Sun Pharma’s own last five-year average of 28.5 times.

In January 2025, we had recommended that investors accumulate the stock. From the previous call, the stock has returned -4 per cent. We believe for long-term investors, the stock can add value as a defensive stock as part of a diversified portfolio. Hence, investors can accumulate the stock on dips. One potential risk can be from tariff announcement by the US on innovative medicine (generics have been spared) which the company must navigate.

Innovative medicine

The company has named the segment Global Innovative Medicines from speciality segment earlier. As the new name suggests, the segment generates revenues from patented medicines and not from generics.

The segment, with more than $1 billion in annual revenues ($368 million in Q3FY26 after adjusting for one-time sales) and a Q3FY26 exit growth rate of 13.3 per cent year on year, is now a mature, self-sustained value generator. This implies that the segment has commercialised assets in the US, Europe and the rest of the world, that can fund a future pipeline and keep adding assets.

The leading asset, Ilumya, for plaque psoriasis, an autoimmune disease, reported sales of $680 million in FY25 globally. Sun Pharma applied for a supplemental application in Psoriatic Arthritis after completing Phase-3 trials. On approval, and with the subsequent launch expected in the next one year, the Psoriatic Arthritis indication should generate 10-15 per cent more sales apart from organic growth of the molecule.

Sun Pharma has launched two more products in the US in the last one year, which should generate sales comparable to Ilumya. In July 2025, it launched Leqselvi (deuruxolitinib) in the US for severe alopecia areata. The company will initially target new patients, backed by a strong clinical trial data to compete with Pfizer’s ritlecitinib (Litfulo) and Eli Lilly’s baricitinib (Olumiant); these competing products were launched in 2022 and 2023 respectively.

In January 2026, Sun Pharma launched Unloxcyt (cosibelimab) for advanced Cutaneous Squamous Cell Carcinoma (aCSCC). This adds a checkpoint inhibitor (anti–PD-L1 antibody) to the portfolio, which belongs to the leading therapy in cancer treatment. Pembrolizumab (Keytruda - from Merck) and Cemiplimab (Libtayo - from Regeneron) are the other approved drugs in the class. Sun Pharma has delayed the launch of the molecule to include long-term efficacy data in the label, which should improve its chances against Merck and Regeneron. But aCSCC is a smaller indication compared to lung cancer. Sun Pharma will explore life-cycle management for the drugs (which could imply other therapies) and holds large potential, especially for Unloxcyt.

Ramp-up in Unloxcyt and Leqselvi in the early phase, continued growth of Ilumya and other assets, approval and commercialisation of Ilumya for Psoriatic Arthritis will continue to drive Sun Pharma in the medium term.

Pipeline assets include Fibromun (Sun Pharma has a 55 per cent partnership with Philogen) in Phase-II and Phase-III trials for glioblastoma and soft tissue sarcoma and GL0034, a product in early trials for type-2 diabetes. With close to $3 billion in cash, Sun Pharma can look for acquisitions too, which it has executed well in the past.

India and others

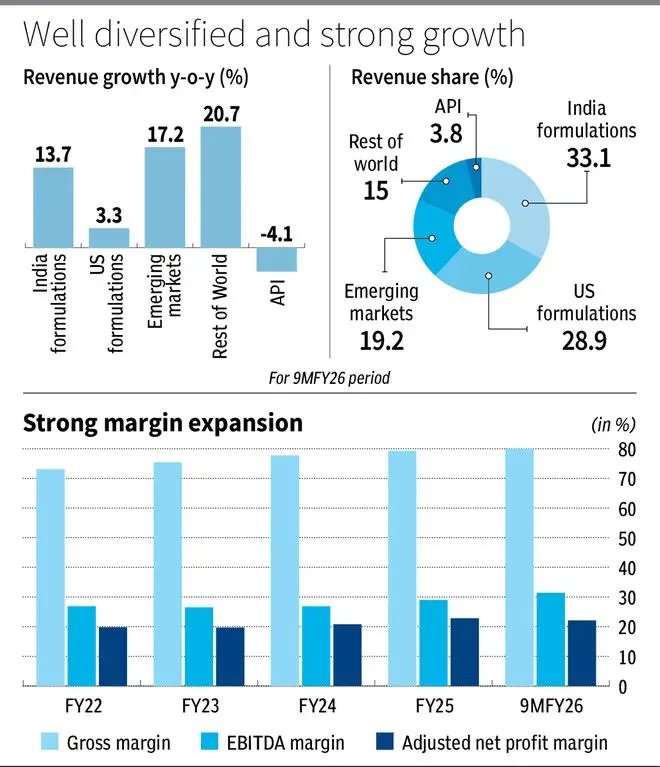

Sun Pharma is the industry leader in the Indian Pharma market and has expanded its share and grown faster than industry at 13 per cent CAGR growth in FY21-25 and 14 per cent year-on-year growth in 9MFY26 as well. The company has benefited from expanded field force supporting such growth and product launches. It is the leader in diabetes segment in India and will participate in the first wave of launches of generic Semaglutide. Sun Pharma has secured approvals for both weight loss and diabetes under two brands.

Rest of the World and Emerging Markets combined accounted for 34 per cent of 9MFY26 revenues and reported growth of 17-20 per cent. The company has launched Ilumya in 35 countries; in some markets, the launch was in the last one year. Apart from generic launches, innovative medicine has also supported such high growth in these countries, as per the company. While it has not announced Semaglutide launches in other markets apart from India, innovative medicine and generic semaglutide should be expected to feature in these regions’ growth drivers.

Sun Pharma gross margins and EBITDA margins have expanded as shown in the table, benefitting from innovative medicine. It has reported revenue growth of 11 per cent in 9MFY26 and margin expansion, as shown in the figure. The margin expansion will face headwinds in the next one year owing to launch costs of the two products amounting to $100 million, as per the company. These will be part of the cost structure initially, while sales growth will be gradual. Consensus estimates place revenue and earnings growth of 11 per cent/12 per cent in FY27 after 11 per cent/9 per cent year-on-year growth in FY26.

Published on February 14, 2026