For decades, efforts to reduce emissions in the built environment have focused on operational carbon, which covers emissions stemming from how buildings are powered, cooled and used.

Unlike operational emissions, which can be gradually reduced as energy grids decarbonize, the carbon locked into building materials is determined at the procurement stage, when materials are specified.

This raises a critical question: how do we decarbonize building materials at scale, while still meeting development needs?

Singapore’s experience of decarbonizing the built environment offers a compelling answer: rather than a single technology, the solution lies in aligning entire ecosystems.

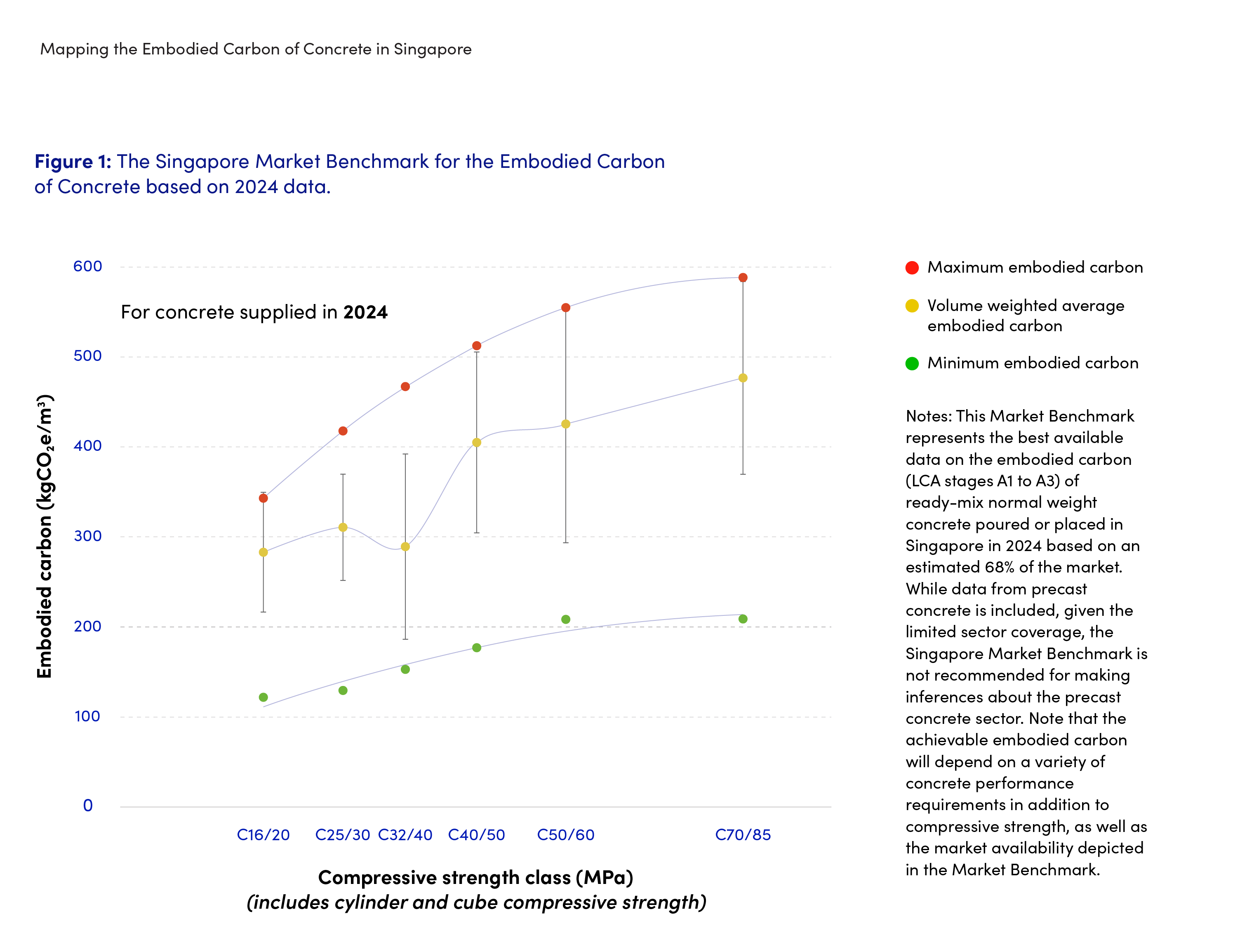

Applying this logic to materials, a multi-stakeholder collaboration has developed one of the first global market benchmarks for the embodied carbon of concrete. The benchmark provides a snapshot of carbon intensity across the national concrete market, covering 68% of supply, and was launched in February 2026 at a joint event with the World Economic Forum's First Movers Coalition.

Loading...

The collaboration’s central finding shows that lower-carbon concrete is already commercially available, with a near-term opportunity to shift towards lower-carbon solutions.

In Singapore, concrete’s upstream emissions are estimated at 3.7 million tonnes of CO₂e – around 6% of national emissions –, yet most occur outside its borders, in imported materials and regional supply chains. Demand is driven locally, while emissions occur globally.

Bridging that gap requires coordination across the entire value chain.

The benchmark for concrete's embodied carbon represents a shift from ambition to implementation. It reveals current performance and the full range between minimum, average and maximum values.

This variation shows that lower-carbon solutions are already available, but adoption remains uneven across the four stakeholder groups and the following actions are key to drive decarbonization in the built environment.

Developers, designers and contractors define material specifications and procurement criteria, making them the primary drivers of change.

In this context, developers and financiers engaged suppliers and the wider construction ecosystem to encourage participation and contribution of data to establish the benchmark. Banks and financial institutions have supported the benchmark, which can provide a stronger business case for them to invest in low-carbon solutions.

Demand-driven initiatives for low-carbon materials, such as the First Movers Coalition and the Climate Group’s ConcreteZero initiative, aggregate demand for low-carbon concrete into credible signals to help build the business case for scaling low-carbon supply, thereby making such projects financeable. These initiatives ultimately seek to create a global market for lower-carbon concrete.

The benchmark was developed by CapitaLand and ConcreteZero. ConcreteZero members, spanning developers, contractors and asset managers across multiple markets, have moved from data transparency to collective implementation commitments, demonstrating demand-side coordination at scale.

This approach has precedent: the UK's Low Carbon Concrete Group has published an annual market benchmark since 2022, which now covers over half of the nation's ready-mixed concrete production.

Singapore's benchmark applies the same logic to a market with its distinct characteristics: import dependency, tropical durability demands, and a unique mix of projects under development.

A key barrier is the lack of consistent environmental data and common definitions of “low-carbon” materials, which limits comparability and increases the risk of misaligned claims.

Market benchmarks are most effective when used alongside certification systems – including the Global Cement & Concrete Association's global rating system for concrete – enabling stakeholders to move from static labels to dynamic, data-driven decision-making.

The result was a rare trifecta: reduced embodied carbon, lower import dependency and a practical solution to waste disposal. Singapore is now recognized as a global leader in circular construction.

Moving forward, the question is not whether lower-carbon building materials exist but whether the systems that govern how infrastructure is built – the specifications, procurement frameworks, financial incentives and certification schemes – enable their demand and deployment alongside necessary urban development.

Singapore's benchmark on decarbonization of concrete is an early answer. Now, the harder work starts on making it the norm.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。