photoman/iStock via Getty Images

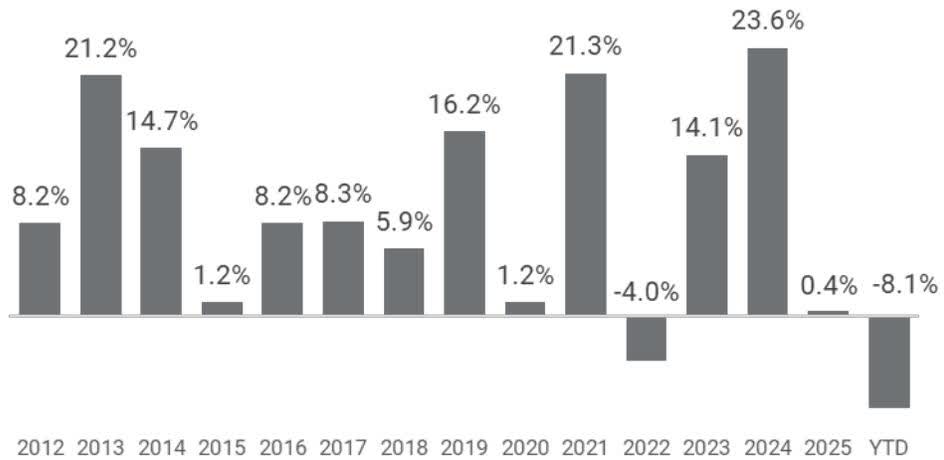

The Value Fund returned -8.1% in Q1. ⁽⁽¹⁾⁾ The outbreak of war in the Middle East caused the major benchmarks to sell off sharply.

While we cannot control geopolitical events or the market's immediate reaction to them, we remain anchored by our process. History and our long-term track record both remind us that these periods eventually pass.

Rather than remaining passive, we used the market's weakness as an opportunity to make a few changes to the portfolio. We increased our stakes in several core holdings and initiated a new position (discussed in the Portfolio Update below) after its valuation became too attractive to ignore.

A feature article in this weekend's Barron's captured the current market sentiment and the disconnect regarding our largest holding— Berkshire Hathaway (BRK.A/B) .

The stock has declined 7% year-to-date and underperformed the S&P 500 by 40% over the past year. This marks one of the worst periods of relative performance in its history. We view Berkshire as fundamentally undervalued. Management appears to share our conviction, having resumed share buybacks last month. With its $370 billion cash pile, we suspect that it will continue to retire shares. The lower the price, the more aggressively they will act and capture value for long-term shareholders.

Fellow Canadian Greg Abel is now in charge. No successor to Buffett can ever hope to replicate his stock-picking genius. But we believe Greg brings a distinct set of strengths to the CEO role. Greg is hands-on, detail-oriented, and—crucially—willing to engage in the operational friction necessary to drive efficiency. Unlike the hands-off approach of the past, we believe Abel will hold subsidiary management teams to a higher standard of accountability, driving margin expansion across Berkshire's diverse operations.

Berkshire Hathaway is positioned to grow operating earnings at a high-single-digit clip for decades. It possesses a fortress balance sheet and a collection of businesses largely insulated from AI-driven disruption. Yet, "Mr. Market" currently remains indifferent, favouring speculative AI narratives over proven cash flow.

Berkshire may not be "sexy," but it is a rock-solid compounder. We expect the tide to turn as valuations eventually reconnect with reality. When it does, our discipline and patience will be rewarded.

Our top performer in the first quarter was TVA Group (CA) (TVA.B) +103.8%. The stock benefited from a significant one-time retroactive revenue adjustment related to its specialty channels, stemming from the resolution of a longstanding carriage dispute. This allowed the company to eliminate all its outstanding debt. Management continues to execute on its restructuring plan, exiting unprofitable channels and rightsizing the cost structure. Despite the stock's appreciation this quarter, we believe TVA remains materially underpriced; its audience share in Quebec remains dominant (above 40%), and several assets—including excess property—remain undervalued on the balance sheet. We continue to believe in the merits of the controlling shareholder, Quebecor Inc. (CA) (QBR.B) , taking the company private.

Our second-best performer in the quarter was Automatic Bank Services Ltd. (ABANF) (SHVA) +22.5%. SHVA delivered strong Q4 transaction growth (+11%) despite regional geopolitical tensions. After several years of margin-compressing investments in core computing and cybersecurity, the company recently announced its intention to implement price increases this year. This highlights the inherent value of businesses with durable network effects: they possess pricing power that can be tapped. While the exact magnitude of these increases has yet to be disclosed, SHVA's current pricing remains well below international card network rates, providing significant headroom for future price increases and margin expansion.

The Hershey Company (HSY) performed well during the quarter, gaining +14.2% as cocoa costs finally retreated, reversing the extreme inflationary pressures of the past two years. As this lower-cost inventory works its way through the balance sheet, we expect input-cost pressures to ease significantly. Crucially, consumer demand has proven resilient; volumes remain above management's original expectations despite the price hikes taken to defend margins. This reinforces our original thesis: Hershey's brand equity is robust enough to withstand significant macro shocks without compromising its long-term competitive position. Furthermore, the company's expansion into salty snacks continues to diversify the earnings stream and support consistent profit growth.

Rounding out our top performers in the first quarter were our defense holdings: Lockheed Martin (LMT) +25% and General Dynamics (GD) +2%. Ongoing global conflicts and the fraying of the NATO alliance continue to underscore the critical need for sustained investment in national defense. Beyond their defense segments, both companies reached a historic milestone this quarter with the successful Artemis II mission—the first crewed flight around the moon since 1972. Lockheed Martin was responsible for the Orion crew module and the spacecraft's complex flight software, while General Dynamics provided the essential emergency radios and transponders that linked the astronauts to mission control. With the crew now safely home, we can officially declare: "mission accomplished."

ICON Plc (ICLR) -39.3% was our primary detractor this quarter following the February announcement of an internal Audit Committee investigation into revenue recognition practices from 2023 through 2025. While the market's reaction was severe, we believe it was an overreaction. Management anticipates the revenue restatement will be less than 2% for each affected year. While disappointing, we believe this issue was an internal matter and will not have any material long-term impact on ICLR's ability to serve its customers. It is also unlikely to have a material impact on the company's $1 billion of free cash flow. We used the selloff as an opportunity to increase our position, and the stock has already begun to rebound. As the pharmaceutical environment continues to improve, we remain confident that the company will capture its fair share of clinical trial activity. With the stock trading at roughly 10x trailing earnings, we believe that the shares remain materially undervalued.

Our second-worst performer in the quarter was Visa Inc. (V) -13.8%. Visa's fundamentals remain exceptional, with 2025 global payment volumes rising 8% and driving double-digit growth in both revenue and earnings. However, the stock has been pressured by macro concerns, specifically the risk of a global slowdown and rising oil prices stemming from the conflict in the Middle East. Higher fuel costs typically dampen cross-border travel—one of Visa's highest-margin revenue streams. Despite these near-term headwinds, Visa remains one of the highest-quality businesses we have ever encountered. We remain confident that its long-term earnings power will compound at attractive rates for many, many years.

We added to several core positions during the quarter that were unfairly caught up in the broader narrative that AI will disrupt every software company. We also initiated a new position during the quarter: Amadeus IT Group (AMADY) . Headquartered in Madrid, Amadeus holds a dominant duopoly position in each of its two major business segments.

The company was originally formed by a consortium of European airlines to create a global distribution system (GDS) that connects airline inventory to travel agency booking systems worldwide. Over decades, Amadeus has strengthened its competitive position and today holds roughly 50% share of all GDS air bookings, with the remainder split between Sabre Corp. (SABR) and privately held Travelport .

While airlines have attempted to bypass GDS providers through "New Distribution Capabilities" (NDC) to save on fees, to date, their efforts have been largely futile. Travel management companies require a centralized, aggregated platform to function efficiently. The sheer complexity of thousands of agencies connecting to hundreds of individual airline APIs creates a powerful network effect. Network effects, once firmly established, are very difficult to disrupt.

The other half of Amadeus' business is its Airline IT segment, which provides mission-critical software that manages everything from passenger service systems to boarding and reservations to roughly 200 major airlines worldwide. Amadeus' software holds about 45% market share among large carriers, and contracts often last for a decade. These platforms are deeply embedded in airline operations, creating massive switching costs and multi-year implementation hurdles for any competitor trying to replace the incumbent. This "stickiness" is reflected in the segment's extraordinary 70%+ EBITDA margins. In our view, the fear that AI will displace this type of critical infrastructure is unfounded; Amadeus remains the backbone of global air travel.

While recent spikes in jet fuel prices—driven by the war in the Middle East—will likely pressure Amadeus’ near-term revenues, we recognize that this is a cyclical headwind rather than a structural one. Because both major business lines are tied to booking volumes, the market has sold off the shares in anticipation of this temporary lull. The selloff provided us with a rare opportunity to acquire a dominant, growing franchise at an attractive price. We remain constructive on the long-term growth of global travel and believe these tailwinds will drive significant long-term value for Amadeus shareholders.

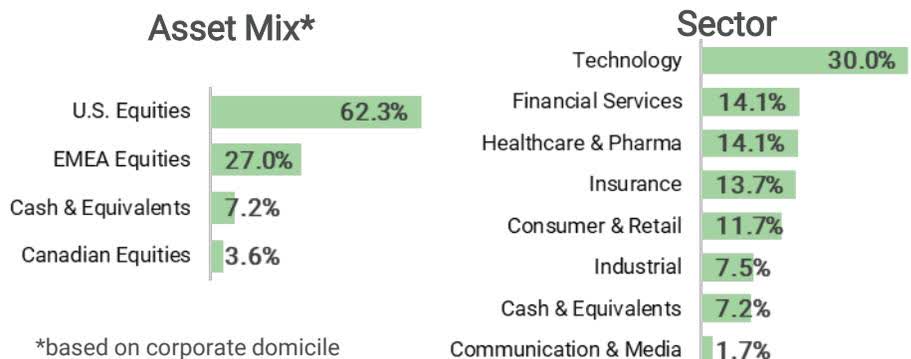

Our top 10 holdings as of the end of Q1 are listed below. We recently released our 2025 Annual Report, which provides more detailed information about the portfolio and is available here .

* As of March 31, 2026. The Value Fund's holdings are subject to change and are not recommendations to buy or sell any security.

Top 10 Holdings * Sector Alphabet Inc. (GOOGL) Technology American Express Company (AXP) Financial Services Automatic Bank Services Limited Technology Berkshire Hathaway Inc. Insurance Compagnie Financière Richemont SA (CFRUY) Consumer & Retail Elevance Health, Inc. (ELV) Healthcare & Pharma ICON Public Limited Company Healthcare & Pharma Intercontinental Exchange, Inc. (ICE) Financial Services S&P Global Inc. (SPGI) Financial Services Visa Inc. Technology

Mark Your Calendars: GreensKeeper's Annual Meeting will be held on Tuesday, June 2, at 7:00 pm at the Mississauga Golf & Country Club . Further details and formal invitations will follow shortly. We look forward to seeing you again at our annual gathering.

Michael Van Loon and I continue to scour the investable universe for high-quality companies trading at attractive valuations. In the current market environment, we are finding an abundance of quality, but a scarcity of "cheap." Consequently, we simply add those names to our growing watchlist, wait for our buy price to be on offer, and move on to the next opportunity.

Investing is rarely easy, but as history has shown, having the discipline, patience and grit required to stay the course during periods of underperformance are what successful long-term value investing demands.

Thank you for your continued trust and for the opportunity to grow your wealth alongside our own.

Michael P. McCloskey, President, Founder & Chief Investment Officer

Michael Van Loon, Associate Portfolio Manager

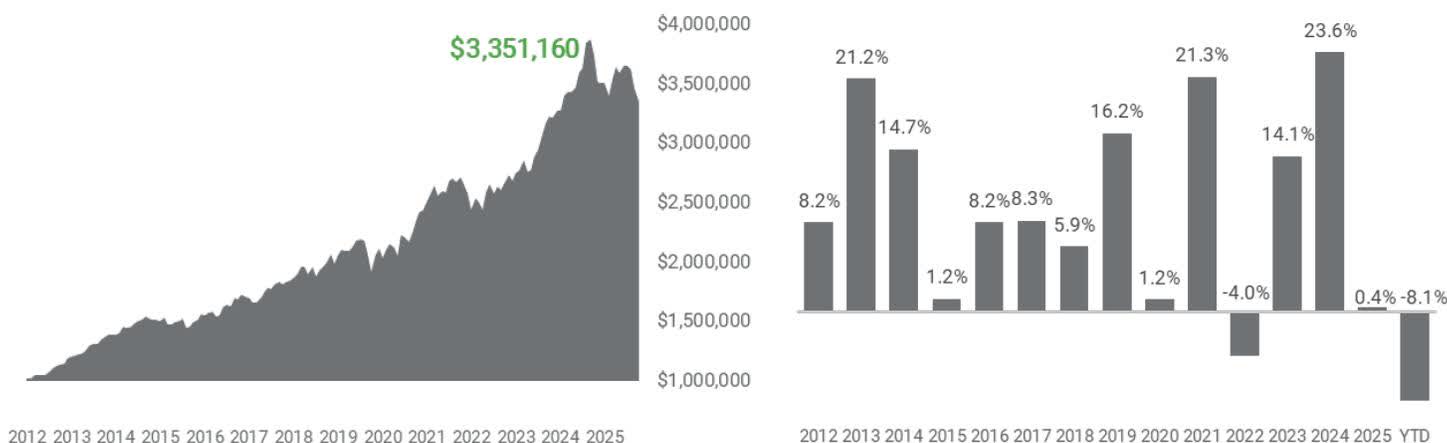

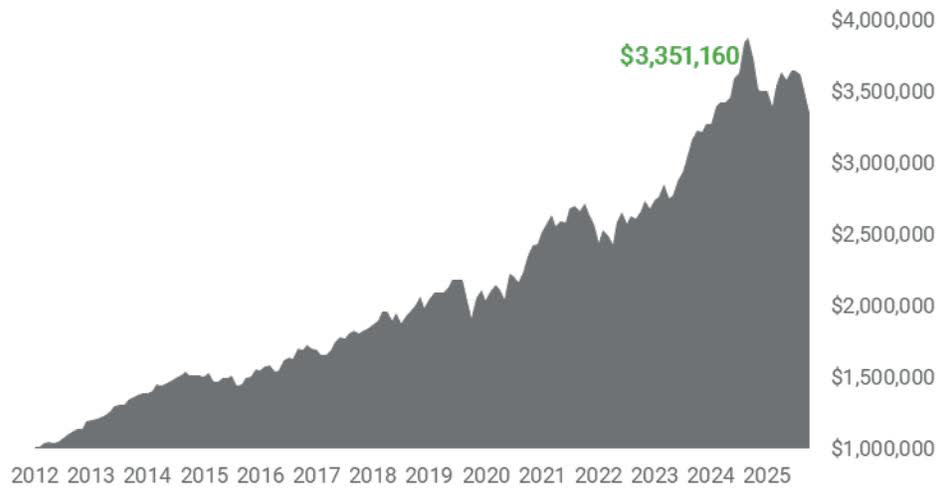

Fund Overview The fund invests in a concentrated portfolio (15-20 stocks), primarily in equities from any sector and market capitalization. Fund Details Fund Distributions ($/Unit Class A) Service Providers Portfolio Performance (Class F) Growth of $1,000,000 Calendar Year Returns Annualized Compound Returns Portfolio Allocations *based on corporate domicile Testimonials Don't just take our word for it. See what our clients are saying: "My wife and I began investing in GreensKeeper in 2023 after decades in mediocre mutual funds. After hearing Michael on a podcast, we were intrigued by his Value Investing strategy, and we like that our investments are in the same ones he puts his own family investments in. Michael and his team are very customer-focused and communicative. We are very glad to be a part of the GreensKeeper family and its growth and success." Doug S.Vice President "My family has known Michael for over 20 years, and we have invested in the Value Fund. He has a track record of success, and we sleep soundly at night knowing that he is growing our investments safely." Dr. Erin R.*Anesthesiologist "We began investing with GreensKeeper in 2013. A large portion of our three grandchildren's education money is guided by Michael McCloskey and his patient advice. We have a long-term view towards investing and trust in the fund's risk aversion strategy for preservation of capital. I recommend GreensKeeper to my friends and family." Timothy B.President & CEO The GreensKeeper Team Michael McCloskey, Founder & CIO Michael Van Loon, Analyst & Assoc. Advising Rep. James McCloskey, Private Client Sales Michelle Tait, Executive Assistant Disciplined Value Investing is simple, but not easy. At GreensKeeper, we put in the work and have the proper temperament to succeed in the stock market. Alignment of Interests Our founder is among our largest investors and has most of his family's net worth invested alongside our clients. Does your IA have their own money invested alongside yours? Owner Managed Our clients deal directly with the people making the investment decisions. Do you know who is managing your money? Disclosures All returns are as of March 31, 2026, for Class F Units (measured in Canadian dollars). GreensKeeper Asset Management Inc. (GKAM) assumed the investment management responsibilities of the Value Fund on January 17, 2014. Before that date, the Value Fund was managed by Lightwater Partners Ltd., while Mr. McCloskey was employed by that firm. Where applicable, all figures are annualized and based on Class F monthly returns since inception. The risk-free rate was calculated using the 90-day CDN T-bill rate. Class F Units are available to purchasers participating in fee-based programs through eligible registered dealers. Class G Units are for purchasers who have over $1 million managed by GreensKeeper and enter into a Class G Agreement with us. Class G Units are not charged a management or performance fee by the Fund as Fees are paid directly to the Manager under the Class G Agreement. The Funds are offered by GKAM and distributed through authorized dealers. Trailing commissions, management fees, performance fees, and expenses may all be associated with an investment in the Funds. The fees and expenses charged with this investment may be higher than the fees and expenses of other investment alternatives and may reduce returns. There is no guarantee that the investment objective will be achieved. Past performance should not be mistaken for, and should not be construed as, an indicator of future performance.

Load Structure No Load Perf. Fee 20% over 6.0% annual hurdle. High-water mark (perpetual). Registered Plan Status 100% Eligible (RRSPs, TFSAs, RESPs, RDSPs, LIRAs, RIFs, etc.) Inception Date November 1, 2011 Type of Fund Long equity, Long-term capital appreciation Fund Category Global Equity Currency CAD Valuations Monthly Redemption Monthly on 30 days' notice Distribution Frequency Annually (DecemBer) Class A Class F Class G Fund Codes GRN 101 GRN 105 GRN 107 NAV $23.86 $25.42 $19.33 MER (%) 1.8% 1.3% < 1.8% Min. Initial Investment $150,000 $150,000 $1 million

2016 - $0.5416 2017 - $0.0000 2018 - $0.5752 2019 - $0.5626 2020 - $0.0000 2021 - $0.0000 2022 - $0.1440 2023 - $0.0000 2024 - $0.0000 2025 - $2.3899

Investment Manager GreensKeeperASSET MANAGEMENT Admin. and Registrar SGGGFUND SERVICES INC. Auditor MNP Custodian National BankINDEPENDENT NETWORK Legal Counsel BLGBorden Ladner Gervais

1 MO YTD 1 YR 3 YR 5 YR 10 YR Inception Value Fund -3.3% -8.1% -10.4% 8.0% 7.4% 8.4% 8.8%

The preceding testimonials are from current GreensKeeper client households with no compensation provided and may not be representative of the views of all people or investors. Certain testimonials were provided unsolicited, and others were provided by request. * Client household includes a GreensKeeper shareholder.

This document is intended for informational and/or educational purposes and should not be construed as an offering or the solicitation of an offer to purchase an interest in the GreensKeeper Value Fund or any other GreensKeeper Funds (collectively, the "Funds"). Any such offer or solicitation will be made to qualified investors only by means of an offering memorandum and only in those jurisdictions where permitted by law. The Value Fund is not intended for US Persons. GKAM is registered in the provinces of Ontario and Quebec, Canada under the categories of Portfolio Manager, Investment Fund Manager, and Exempt Market Dealer and in Alberta under the categories of Portfolio Manager and Exempt Market Dealer. GKAM is also a Registered Investment Advisor with the United States Securities and Exchange Commission ("SEC"). Registration as an investment advisor does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the SEC or by any state securities authority. An investment in the GreensKeeper Value Fund is speculative and involves a high degree of risk. Investing in the GreensKeeper Value Fund is speculative and involves a high degree of risk. Opportunities for withdrawal, redemption and transferability of interests are restricted, so investors may not have access to capital when it is needed. There is no secondary market for the interests, and none is expected to develop. Investments should be evaluated relative to an individual's investment objectives. The information contained in this document is not and should not be construed as legal, accounting, investment or tax advice. You should not act or rely on the information contained in this document without seeking the advice of an appropriate professional advisor. Please read the Fund offering memorandum before investing.

The performance figures for the GreensKeeper Value Fund include actual or estimated performance or management fees and are presented for information purposes only. GKAM has compiled this document from sources believed to be reliable, but no representations or warranty, express or implied, are made as to its accuracy, completeness or correctness. All opinions and estimates constitute GKAM's judgment as of the date of this document and are subject to change without notice. GKAM and its clients may have a position in the securities or assets discussed. Securities mentioned may not be representative of GKAM's current or future investments. GKAM may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice. GKAM assumes no responsibility for any losses, whether direct, special or consequential, that arise out of the use of this information. Certain statements in this presentation are based on, inter alia , forward-looking information that is subject to risks and uncertainties. All statements herein, other than statements of historical fact, are to be considered forward-looking. Such forward-looking information and statements are based on current expectations, estimates and projections about global and regional economic conditions. There can be no assurance that such statements will prove accurate; therefore, readers are advised to rely on their own evaluation of such uncertainties. Further, to the best of GKAM's knowledge, the information throughout the presentation is current as of the date of the presentation, but we expressly disclaim any duty to update any forward-looking information. The GreensKeeper Value Fund strategy in no way attempts to mirror the S&P/TSX or the S&P500. The S&P/TSX Composite Index and the S&P500 Index are provided for information purposes only as widely followed indices and have different compositions and risk profiles than the GreensKeeper Value Fund.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。