narvo vexar/iStock via Getty Images

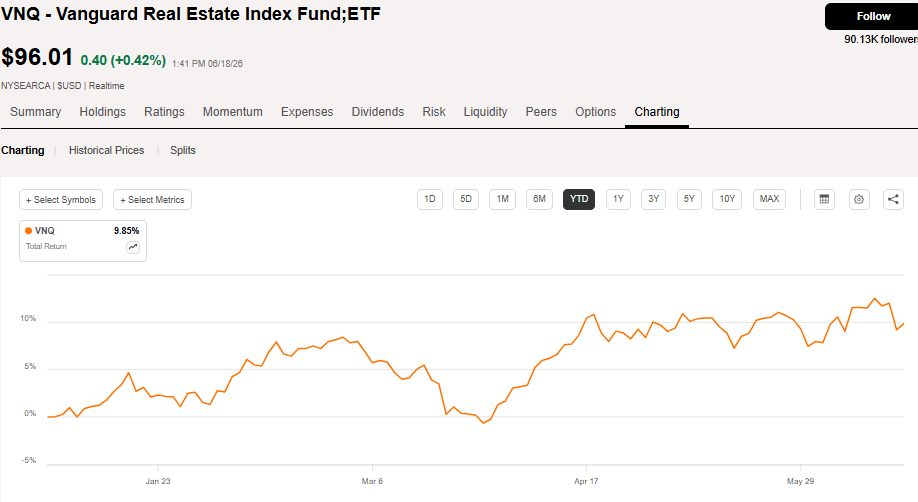

REITs have had a strong 2026 with YTD returns of +9.85 on the Vanguard Real Estate ETF (VNQ).

SA

Within any index there is usually a dispersion of performance and that is particularly true in REITs. Individual REIT performance ranges from Creative Media and Community (CMCT) down 99% to Chatham Lodging (CLDT) up 95%.

Many of the REITs that are down in 2026 are the junky, microcap companies with excessive debt loads. However, there are 2 strong companies that have been left behind and have become opportunistically cheap relative to the rest of the market.

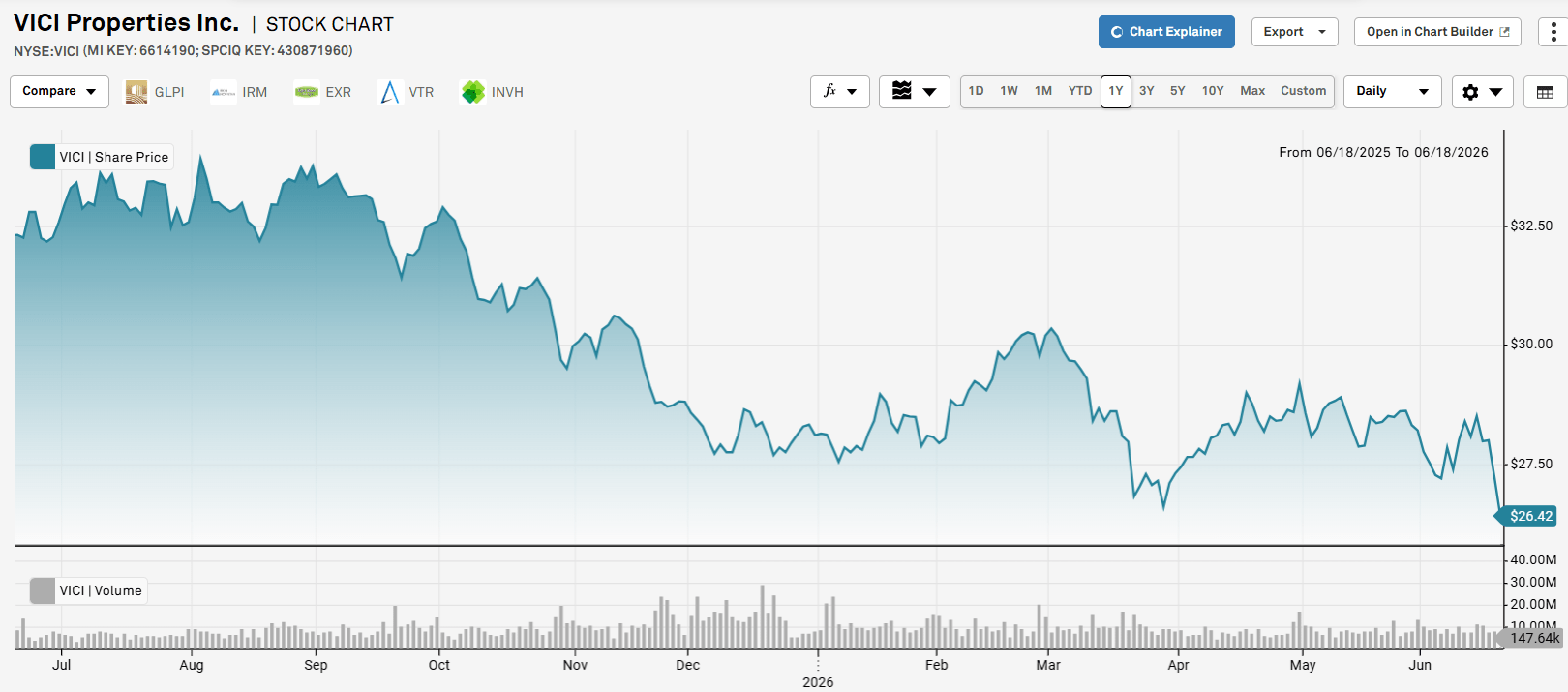

Left behind opportunity #1: VICI Properties

VICI’s stock price has fallen in a precipitous fashion.

S&P Global Market Intelligence

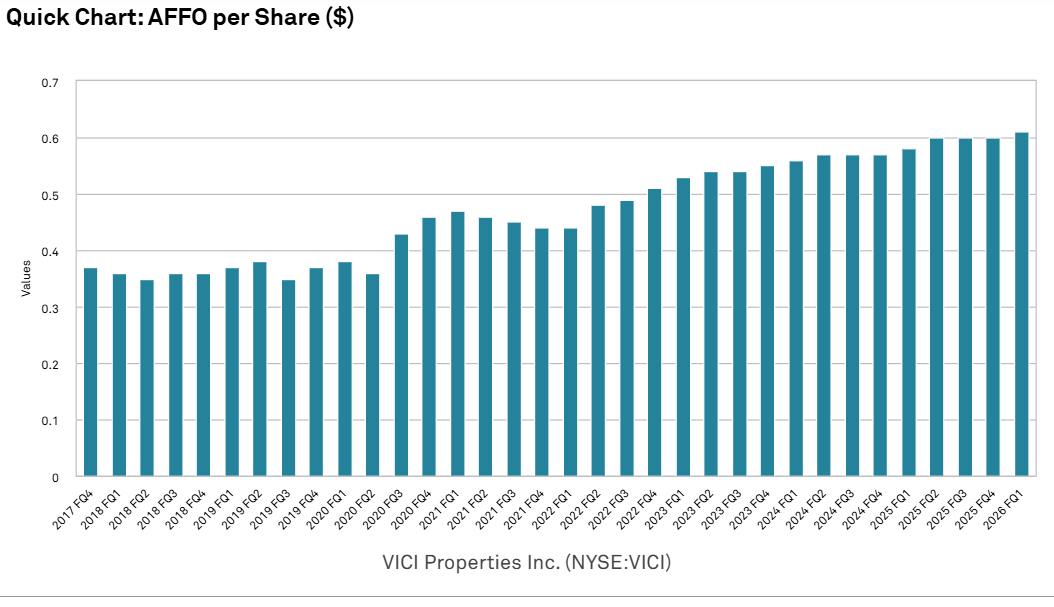

Its individual company performance has been excellent. AFFO per share has grown steadily from 3 key drivers

These factors resulted in healthy and predictable growth.

S&P Global Market Intelligence

Thus, the market’s selling of VICI is likely not related to company level numbers.

Instead, there are a series of related big ticket news items:

To get a sense for how these could affect VICI, recall that Caesars is 38% of VICI’s rental revenues and MGM Resorts is 32% of revenue.

S&P Global Market Intelligence

Thus, in a matter of a months, 70% of VICI’s tenant base is changing hands.

These buyouts are not inherently positive or negative. Potential benefits to VICI would be that their leases are now tied to larger entities.

Some would argue that Caesars was struggling a bit and there was some concern about their lease with VICI. In the hands of Fertitta, Caesars is now better capitalized and potentially a more solid credit for the very long remaining lease term. The same could be said of MGM, although it was in better shape than Caesars.

Both Barry Diller (of People Inc) and Fertitta are known as empire builders within the entertainment industry. As such, these potential buyouts are not likely to be a standard private equity LBO gut job. I think it is more likely that these iconic casino assets will be seen as key pieces of their entertainment empires. Therefore, we believe VICI’s long term leases remain a stable and growing source of cashflow.

The trickier piece to analyze is the explosion of gambling outside of casinos. Online sports betting is out of control and seems to still be accelerating with betting volume on the New York Knick’s finals setting records.

Pseudo-gambling predictions markets like Kalshi or PolyMarket are growing rapidly and at least for now are able to evade the heavier regulation of things that are officially classified as gambling.

Bears suggest that online and off-site gambling quenches people’s thirst for risk, thereby reducing future demand for casino visits. Bulls suggest that sports betting serves as a gateway drug that will later entice people to come to Vegas for the real thing.

Overall it is just a lot of moving pieces. I don’t think these major news items harm VICI, but it makes it a much more active stock to analyze which might not sit well with its investor base.

Triple net REITs are meant to be slow moving vehicles that pay out large dividends that slowly increase over time. They are supposed to be the tortoise, not the hare. VICI was, until recently, the king of triple net REITs with leases locked in for as long as 30 years. It likely attracted an investor base that wanted to just hold it and collect steady dividends forever.

While VICI’s revenues still look quite steady, the sheer volume of high impact news makes it feel a lot less like a sleepy triple net REIT. I suspect this has chased off a portion of investors who just wanted to park their money somewhere and not have to actively analyze.

The stock drop has left VICI as a deep value REIT. It is still well positioned for steady AFFO/share growth.

S&P Global Market Intelligence

It just now trades at 11X forward AFFO which I view as opportunistic.

Left behind opportunity #2: NexPoint Residential Trust

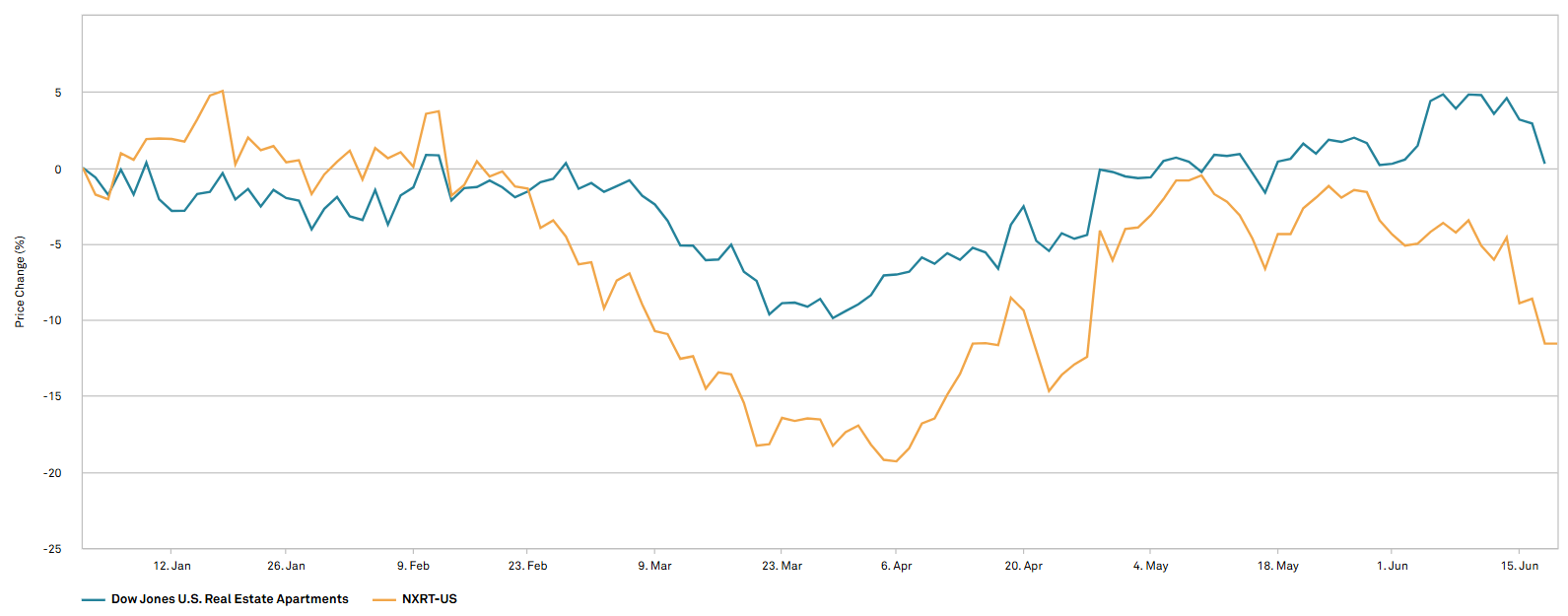

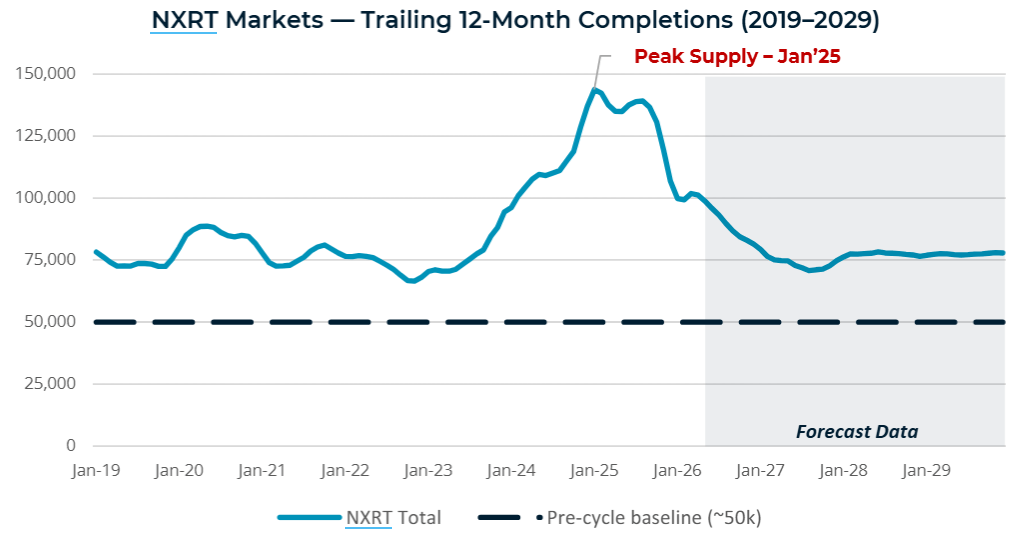

Apartments are facing a wave of deliveries from developments that were started years ago. By now, this is common knowledge and the sector has lagged as the market anticipates a difficult leasing year.

NXRT dropped more than the sector because it is located in sunbelt markets that are the epicenters of the supply.

S&P Global Market Intelligence

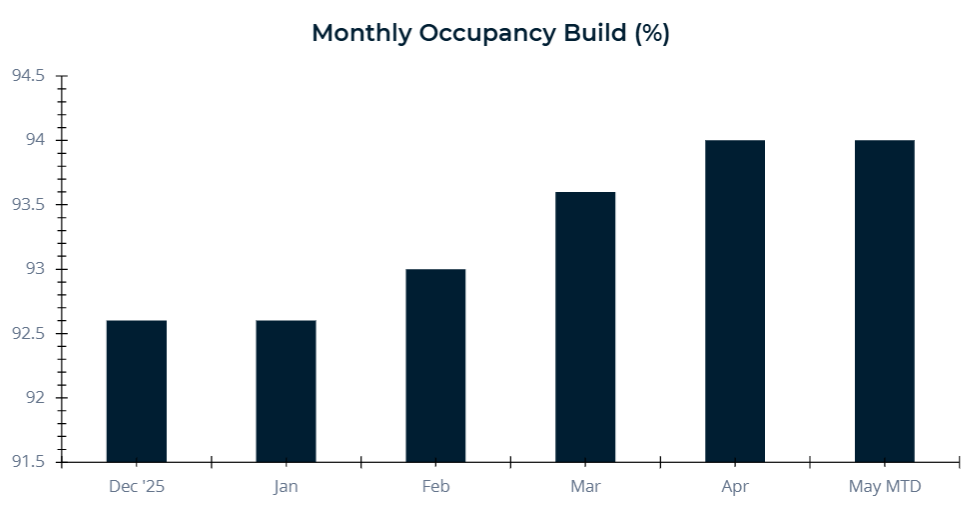

However, there was a substantial turnaround in 2Q26. There were 3 factors driving the revival:

NXRT

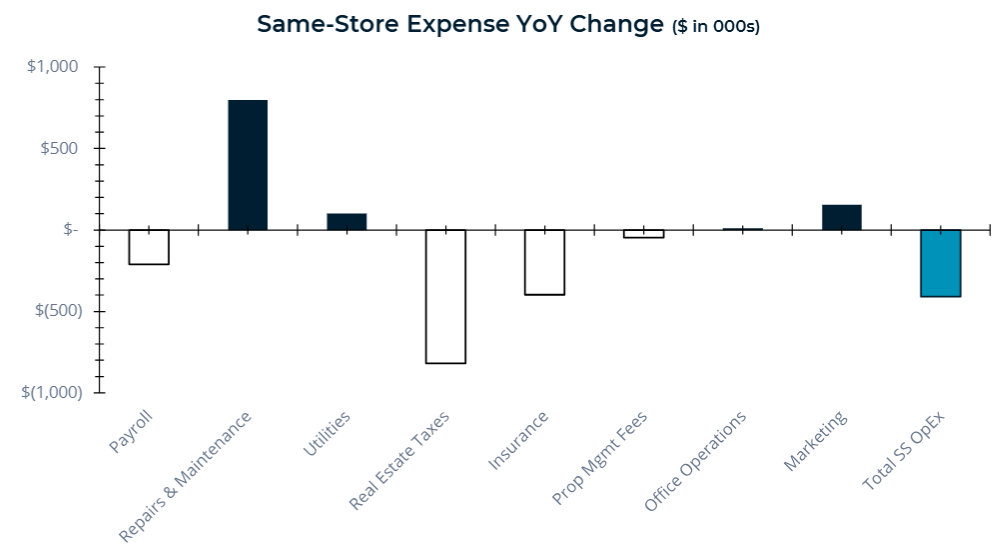

2) Earnings came in significantly ahead of expectations. In addition to the better-than-expected leasing, big ticket expense items like Insurance and taxes came in light.

NXRT

3) The end of supply is in sight. Both NXRT and CPT had commentary suggesting early 2026 was the trough for the sector with a return to earnings growth ahead.

NXRT

While new supply is slowing, demand growth remains strong for sunbelt markets. Houses remain quite unaffordable relative to apartments which is raising retention rates and keeping a higher percentage of the population in rental.

While the sector fundamentals improved materially, NXRT stock took another drop in June as the Fed started to be perceived as increasingly hawkish. Since NXRT is a bit higher leverage than peers, it feels greater impact from Fed trajectory.

So that is how NXRT got cheap relative to the market. It is now deeply discounted, trading at 65% of net asset value and 11X forward AFFO.

A discount of this magnitude was supported by sector level headwinds. Those are presently clearing up and NXRT is on the cusp of returning to healthy AFFO per share growth. As forward guidance starts to show AFFO/share growth I think the multiple will rerate substantially higher. 11X AFFO does not make sense for a growing company when REITs are trading at 17X, and the broader market is trading well north of there.

The bottom line

The stock market is trading at extremely high multiples but there are still pockets of value. To the extent the value is attached to high quality companies with strong property portfolios, I think it will significantly outperform going forward. VICI and NXRT both have healthy fundamental outlooks and are trading well below fair value.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。