swissmediavision/E+ via Getty Images

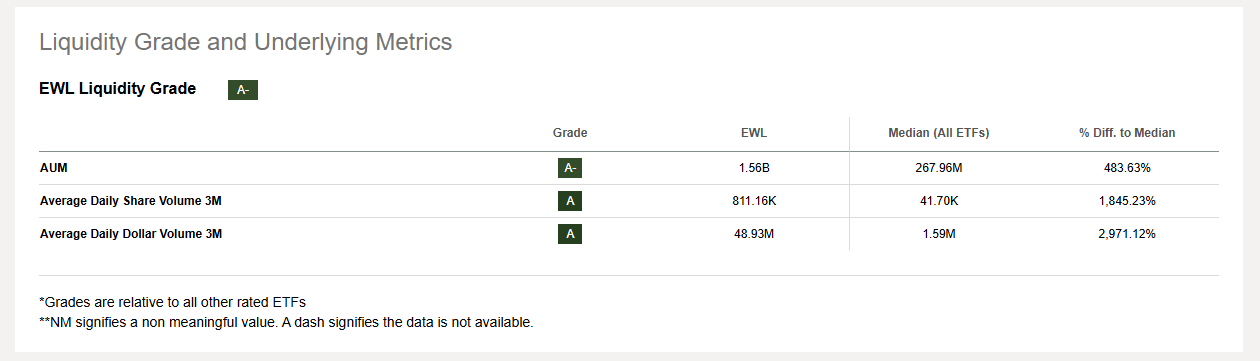

The iShares MSCI Switzerland (EWL), which is one of the oldest geographic ETFs around, completed three decades as a listed product on March 12th, 1996. Since its inception, this BlackRock, Inc. (BLK) product under its 'iShares' brand of ETFs has garnered a total AUM of over $1.56 billion by the time of writing. EWL, which has nearly $50 million trading volume on average (over 30x more than what a standard ETF has), is priced at an expense ratio that is in line with the ETF median of 0.5%.

Liquidity metrics table (Seeking Alpha)

While EWL offers exposure to around 40 stocks from Switzerland, it doesn’t actively pick these stocks but instead tracks an index (through a sampling process) that represents the movements of these stocks. The index in question is the MSCI Switzerland 25/50 Index (MS2550I) and is a variation of the MSCI Switzerland Index (MSI), which is largely seen as a barometer of the health of Swiss equities by the global fund management fraternity; after all, this index is supposed to represent the top 85% of Switzerland’s free-float market capitalization. MS25501 differs from MSI in that it seeks to impose specific caps on its holdings to prevent concentration effects. These caps include preventing any single stock from accounting for 25% of the index and preventing all stocks with individual weights of over 5% from jointly aggregating to 50% of the total index.

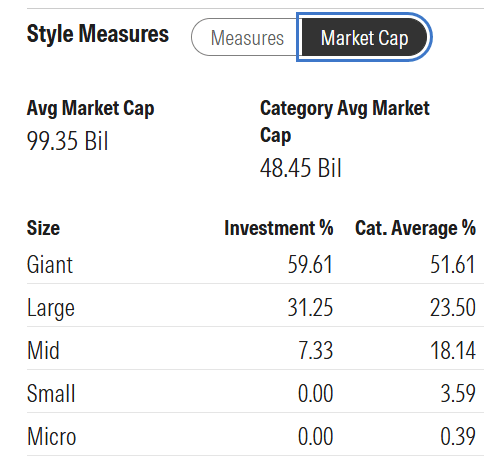

As noted earlier, EWL’s tracking index is a subset of a free-float market-cap-weighted index, which also only focuses on the top 85% of Swiss equities. This means investors won’t get any access to small caps, with giant caps accounting for the lion’s share of the portfolio (60% exposure).

Market cap breakdown (Morningstar)

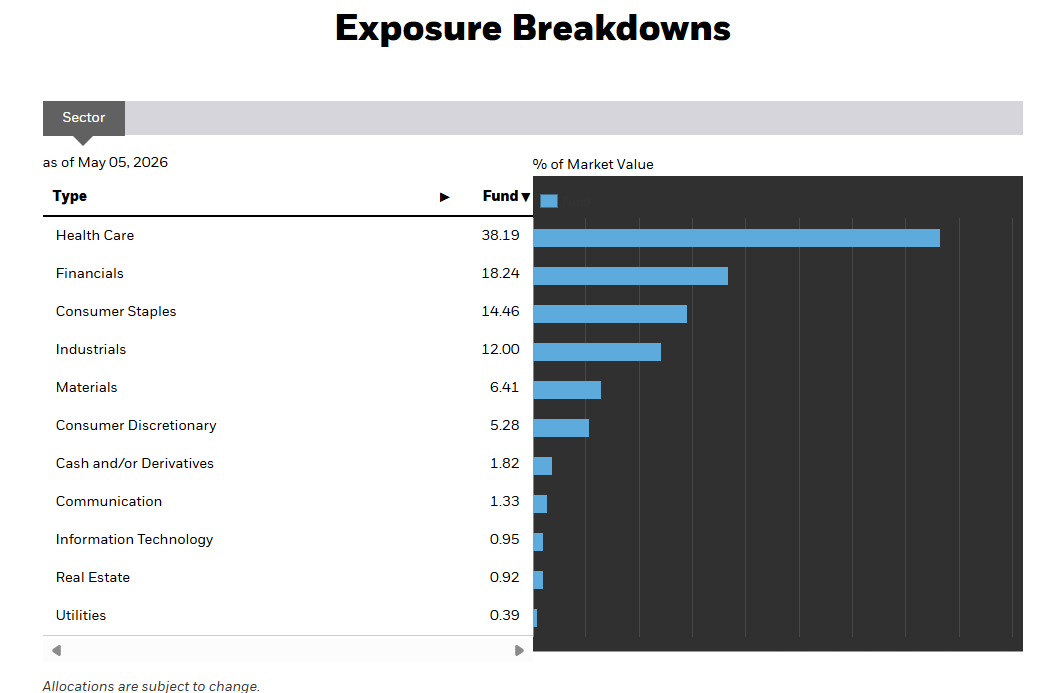

From a sector angle, EWL offers exposure to 10 different sectors (the energy sector is a notable miss), but one sector in particular stands out-healthcare (which accounts for a significant share of 38%, which is well over 2x more than the next largest sector-financials). Even so, if one looks at EWL’s next 4 sectors, they have the look of old-school industries. This, of course, would shift over time depending on the index holdings.

Sector exposure chart(iShares)

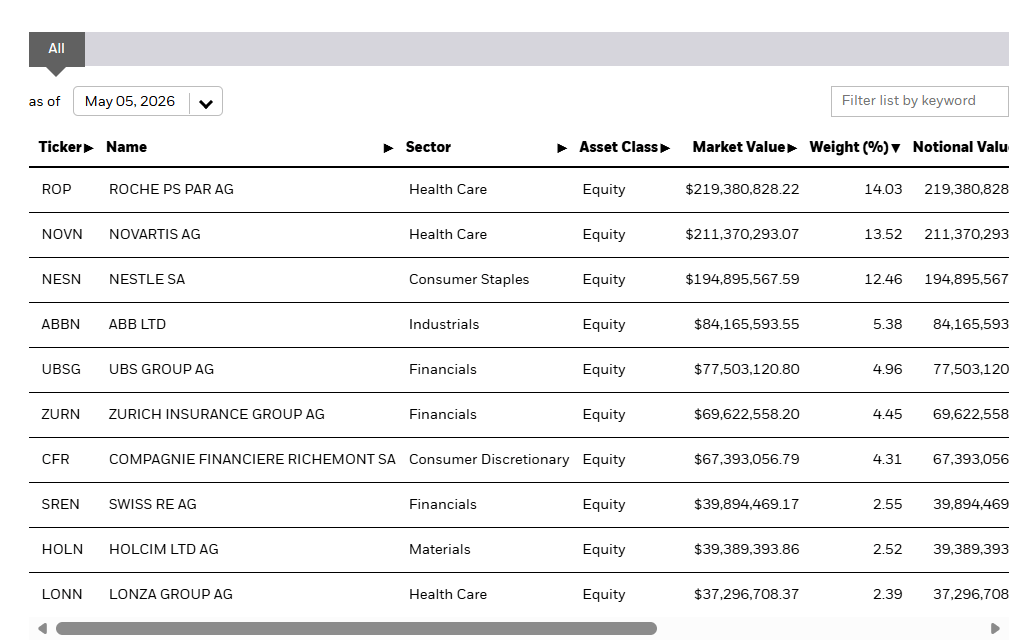

Also note that even though EWL’s tracking index imposes certain caps on its holdings, the top 3 stocks alone (which come from defensive sectors such as healthcare and staples) have quite a sizable aggregate weight of 40%.

Top holdings (iShares)

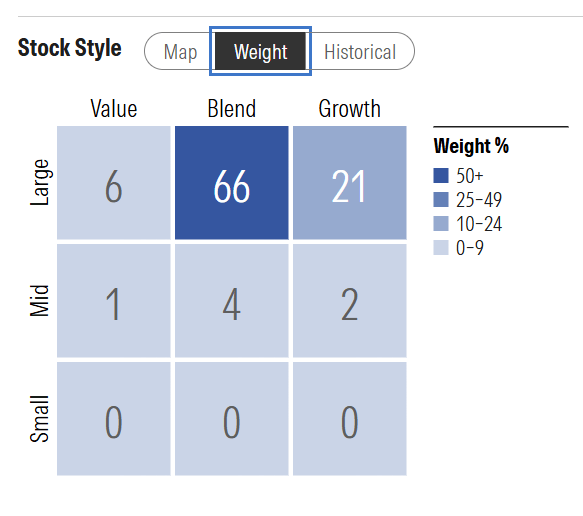

Stylistically, investors who want the best of both worlds from growth (strong sales and earnings growth, strong price momentum) and value-style investing (cheap valuations, strong payouts) will be interested to note that EWL mainly tilts towards hybrid stocks, which account for 70% of this portfolio.

Style breakup (Morningstar)

EWL is currently dominated by stocks from defensive sectors, or those that focus on products and services that are deemed as necessities, which tend to benefit from constant demand. This helps bring a degree of stability, which would appeal to conservative investors. CHF-based assets also typically tend to see a spike in interest from global investors during periods of geopolitical strife, global tensions, and general risk aversion in the financial markets. This would also make EWL suitable for those who want to bring a global defensive component to their portfolios, which may perhaps already be inundated with growth-heavy products or high-beta products (products that move at a greater than 1x factor than the equity benchmark).

Regardless of the particular sector mix at any given time, EWL is suitable for investors who want exposure to Swiss companies without a currency hedge.

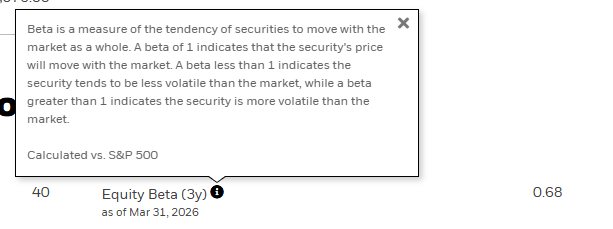

It’s worth noting that EWL’s beta against the S&P500 itself is quite moderate at only 0.68x, suggesting that during downturns for US stocks, EWL will likely drop by a lesser cadence.

Beta (iShares)

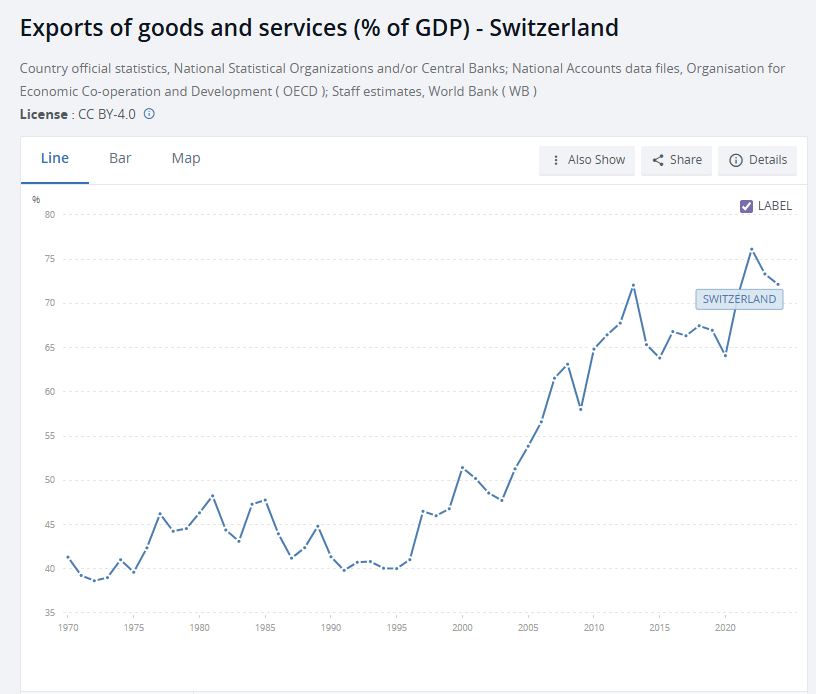

Switzerland will also appeal to those who like trade-heavy economies that have a resilient export component as part of their overall growth story (these investors are also generally bullish on the prospect of increased globalization with reduced trade barriers, particularly in the fields of healthcare and pharmaceuticals). Note that exports, which accounted for less than half of Swiss GDP three decades ago, now account for almost three-quarters of its GDP.

Export as a % of GDP (World Bank)

Switzerland’s reliance on exports could also be detrimental in an environment where global trade barriers are likely to be lifted and major importers like the US (Switzerland’s largest foreign market) start imposing tariffs.

Since EWL’s NAV (Net asset value) is denominated in USD but its holdings are denominated in CHF (Swiss Franc), a depreciation of the CHF against the USD could prove to be detrimental from a return angle, even if EWL’s holdings don’t move in CHF terms.

As implied earlier, EWL is not necessarily a well-diversified ETF, with just 3 holdings accounting for over 40% of the total weight of the portfolio, making this product quite sensitive to the prospects of just a handful of names. Also, since the top 3 belong to defensive sectors such as healthcare and staples, bullish conditions for developed market stocks or an increase in risk appetite for equities won’t be well captured by these defensive stocks, which are likely to see a more muted performance.

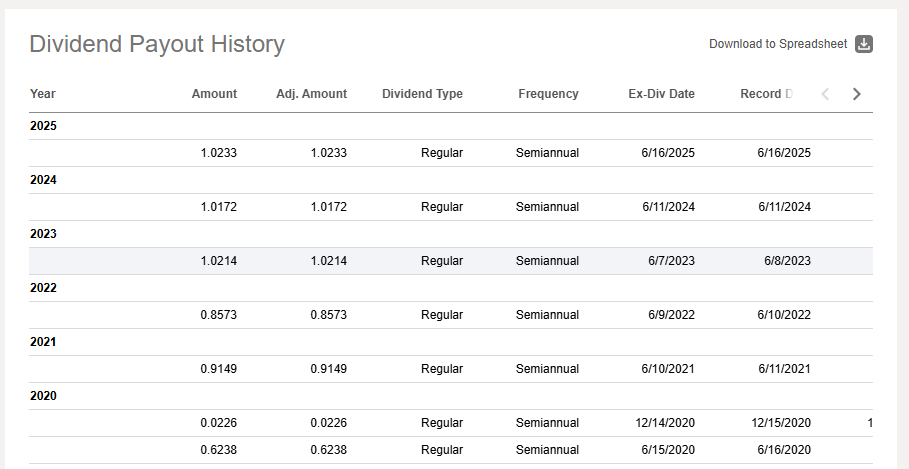

Those who’d like to see their ETFs pay regular dividends ought to be wary of a product like EWL. Since 2008, it pivoted to a semi-annual distribution policy, but those distributions have proved to be quite erratic over the years; in fact, it’s worth noting that even though the ETF prospectus still points to semi-annual distributions, since 2021, EWL has only been paying dividends once a year (in June).

Dividend payout (Seeking Alpha)

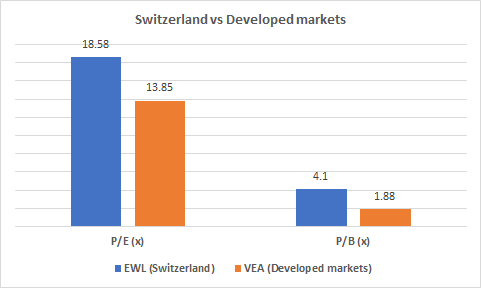

Even though EWL largely focuses on hybrid-style stocks, the valuation quotient of this portfolio isn’t particularly alluring, making this an unfavorable prospect for value-conscious investors. To elaborate, EWL is priced at an earnings multiple of close to 19x at the time of writing, which translates to a 35% premium over other developed markets; on a book value multiple basis (over 4x), the premium is even more pronounced at over 100%. This, of course, can change over time.

Valuations (Morningstar)

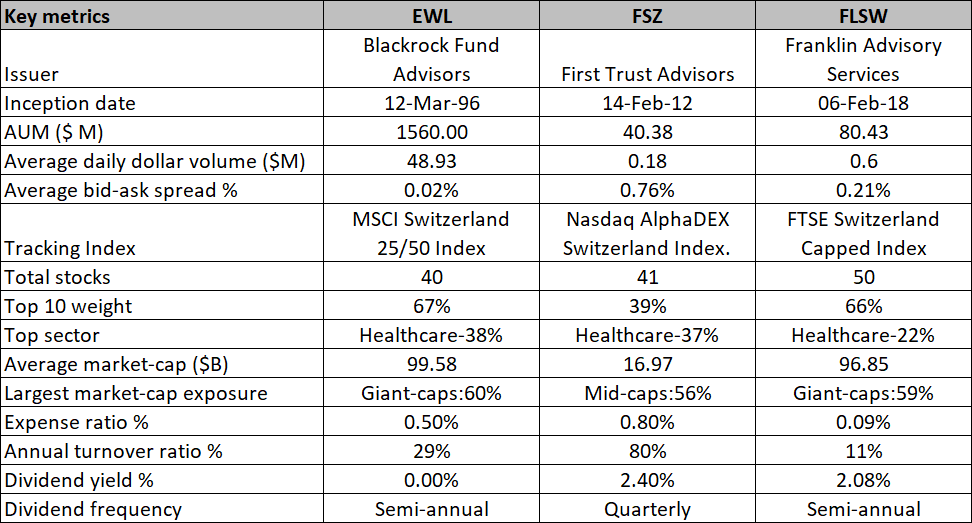

EWL isn’t the only US-listed ETF that offers pure-play coverage to Swiss stocks. Alternatives come in the shape of younger, passively managed options such as the Franklin FTSE Switzerland ETF (FLSW) and the First Trust Switzerland AlphaDEX Fund ETF (FSZ), both of which have under $100 million in AUM, a fraction of what EWL's. Failure to attract meaningful investor attention is also reflected in the degree of dollar volumes seen per day (not even $1 million). The drawback of this is that it tends to translate to wide differences between these products' bids and asks, resulting in the prospect of slippages (while EWL’s spreads are very tight at 0.02%, FLSW’s are over 10x wider, and FSZ’s are very concerning at 0.76%).

So why then should investors consider these alternatives?

Well, FLSW is suggested because it is by far the most cost-efficient (an expense ratio of just 9bps, which is not even a fifth of what it costs to own EWL). It also offers wider exposure (10 more stocks than FLSW) and isn’t as big on healthcare as the other two (basically more diversified). It is also the most stable ETF out of this lot, with annual churn of just 11%, likely resulting in minimal transaction costs.

FSZ follows a smart-beta index that seeks Swiss stocks with relatively high growth and value scores. While it also covers only a similar number of stocks as FSZ, the concentration effects of its top holdings are not too pronounced. Note also that unlike the other two that mainly focus on giant caps from Switzerland, FSZ emphasizes stocks from the mid-cap bucket. FSZ also pays distributions more frequently and offers the best yield. However, it's quite expensive to own (expense ratio of 0.8%), and besides the wide bid-ask, its smart-beta index also drives a lot of churn (80% per year), which will trigger a lot of transaction costs.

Key stats (Seeking Alpha, Morningstar)

EWL comes across as a highly liquid but pricey (from a valuation standpoint) and top-heavy developed market ETF for those seeking a defensively themed international product to help hedge one’s portfolio. EWL has a history of erratic distributions and could be vulnerable to an adverse global trade environment.

This article answers these three main questions about EWL:

Editor's note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。