AoZaaStudio/iStock via Getty Images

At a recent investment conference, we made some baseball caps that bashfully shouted on the front: ‘ Make “Long-Term” Great Again ’. This was our brief dalliance with Trumpian ‘merch’ culture, mercifully without the red caps, rallies, or promise of instant results. Its purpose was to be an icebreaker, but at its heart, a statement of principle.

Meanwhile, another attendee at one of the snack tables had a similar idea and wore a cap that said: “Make Volatility Great Again. ” We guessed that he was working for a brokerage firm.

We can already feel your scepticism. “Long-term” is one of the oldest cards in the fund manager’s deck, usually pulled from the inside pocket as soon as performance goes awry. Sometimes it’s a philosophy; sometimes it’s just a way to launder underperformance.

We hope that by the end of this letter, you will believe that our intention was the former.

This was the second negative quarter since 2022 for the SaltLight BCI Worldwide Flexible Fund. Over the last six months, we have been deliberately harvesting profits in parts of the portfolio, particularly in AI infrastructure, and reallocating capital to better expected-value opportunities.

As fate would have it, at the same time we have experienced meaningful declines in companies such as Blu Label Unlimited, Sea Ltd (SE), and MercadoLibre. We think this sell-off has been an absolute gift, especially with a little cash on hand. In the short term, for these companies, the market has decided that we are either wrong or. . . early. For a time, those two things could look identical.

Back in the US, fast capital has flowed into what we would opine are mediocre AI infrastructure businesses, with revenue surges driven by short-term AI bottlenecks. Time will tell if great businesses are born from these shortages, but our job is not to chase every price move. We must distinguish between temporary scarcity and focus our attention on enduring advantage.

The most important question about an investment manager is not what they own today or what they think will happen next quarter. It is what game they are playing.

Some managers play the very difficult event game . They try to predict quarterly earnings, elections, wars, tariffs, interest rates, currencies, and the next macro surprise.

Others play the safer benchmark game : stay close enough to the index to avoid embarrassment, but far away enough to justify a fee.

Meanwhile, SaltLight is trying to play a different game: the waiting-and-building game. . . And at times, despite our best intentions, it can become a building-and-waiting game.

When we communicate to potential investors what we plan to do with their hard-earned capital, our goal is to convey a fairly simple idea that is hard to execute.

We are curating a portfolio of exceptional global businesses that can become materially more valuable over many years by adapting, innovating, serving customers better, expanding their opportunity set, and reinvesting intelligently.

Ideally, the best of these companies does not rely on a single product, a single market, or a short growth curve. They stack new S-curves on top of existing ones and press their differential and durable advantages. Yet few second-, third-, or tenth-act businesses succeed. Almost all companies fail to build the “next thing”, and so market participants tend to shoot first and ask questions later.

Most businesses lack the culture of innovation and management ambition required to invest in a future not yet visible in this quarter’s numbers. Pair that institutional timidity with the incentive structure of a hired CEO on a five-year contract: protect current margins, defer tomorrow’s opportunity, collect the bonus, and let someone else explain the missing growth. Before long, Long-Term and Great are no longer guiding principles. They survive as corporate folklore, stories told about a company that once knew how to build.

Here the lunacy reaches its full bloom. Shareholders say they want growth. They wail and gnash their teeth at the cost of producing it. Their pressure flows downhill from clients, consultants, ratings tables, quarterly league tables, and the endless industry of measurement that surrounds them. The result is a negative feedback loop of mutually reinforcing mediocrity, in which managers stop investing in the future, and shareholders later wonder where greatness disappeared.

Another quirk is accounting. In the industrial era, if a company built a factory to support growth, the cost was capitalised and then depreciated over many years through the income statement.

Technology businesses are different. Building a consumer habit, subsidising logistics, hiring engineers, or acquiring customers often hits the income statement immediately. Long-term investment is often conflated with an “expense” and can easily be mistaken for deteriorating economics.

But a treasured few companies get Long-Term right; and when they do, they generate incredible value for shareholders. NVIDIA (NVDA), AppLovin (APP), Sea Ltd, and Blu Label have materially grown our capital. One pattern is that, more often than not, companies run by founders tend to have a different license to operate than those run by hired guns do.

Part of the reason we chose the harder path of building SaltLight from scratch a decade ago was shaped by our own experience as entrepreneurs. We wanted to be a different kind of shareholder. We project ourselves sitting on the same side of the table as the builders in our portfolio companies. We make a concerted effort to understand their ambition behind their investments, judge whether the opportunity is real, and back those with the courage, competence, and staying power to build what comes next.

Back to what has been going on with our portfolio. Over the last six months, we have deliberately reoriented the portfolio toward a quasi-building mode again. By our estimate, roughly 46% of the portfolio's exposure is in businesses that are either already undertaking or about to enter a multi-year investment cycle . We have chosen the lonely path to Long-Term martyrdom. It is likely to be choppy, but this is how we play our part in making Long-Term Great again.

Before you flee to the comforting arms of near-term certainty, in this letter, we want to walk through how several of our portfolio companies are investing for the future. MercadoLibre is building the financial ecosystem for Latin America. Tencent (TCEHY) is building AI services on top of one of the world's most valuable consumer and enterprise ecosystems. AppLovin is extending its advertising engine across more than one billion users. WeBuyCars is building a national scale in South Africa's fragmented second-hand vehicle market.

Let's delve into the details on MercadoLibre that demonstrate our thinking and where we differ from the market.

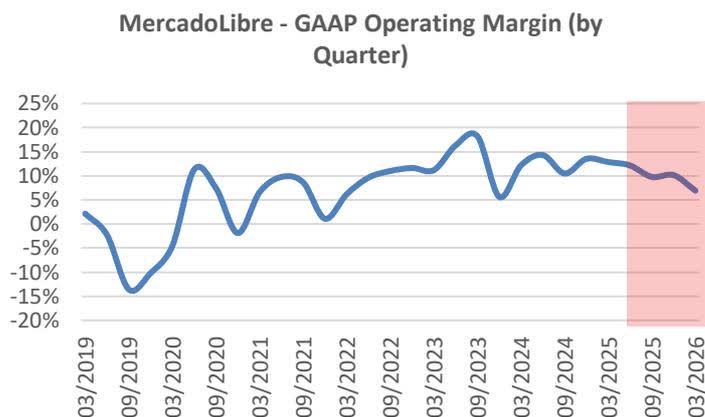

MercadoLibre (MELI) has recently made several decisions that have put pressure on short-term margins. History shows that MELI has gone through this investment cycle before and emerged significantly stronger as a result. We think that the market reaction misses some key points. It has (1) lowered free-shipping thresholds, (2) expanded its credit card offering, and (3) pushed further into cross-border commerce. Investors, without mincing words, have punished its share price.

The last time MELI cut free-shipping thresholds by a mere 20%, commerce revenues subsequently increased 3.3x over the following years. In a network-effect business like 3P e-commerce, this creates multiple layers of opportunity. The first-order benefit is that more buyers attract more sellers due to the larger customer base. The second-order benefits are the more profitable ones: MELI sells more high-margin advertising and financial services to both sides of the network.

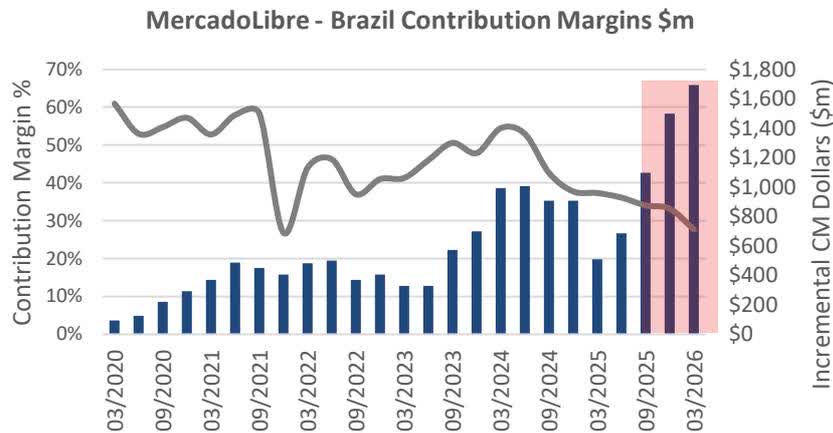

The 2025 Brazil threshold reduction is far more aggressive (~75%) and has resulted in a halving of contribution margins in the last year. But we already see early signs of a substantial increase in contribution margin dollars in the graph below ² .

Now, investors tend to focus too much on margin percentages rather than on incremental margin dollars. The truth is that we do not mind lower margin percentages when margin dollars increase, provided that fixed capital investments, such as logistics, are leveraged. Jeff Bezos understood this dynamic well when building Amazon (AMZN)'s unassailable position, because the other side of the equation is that a competitor must operate at similar gross margins, resulting in much smaller gross profit dollars – but at a lower scale. The most-scaled player (MELI, in this case) is usually the winner in the long term. We think this will play out again.

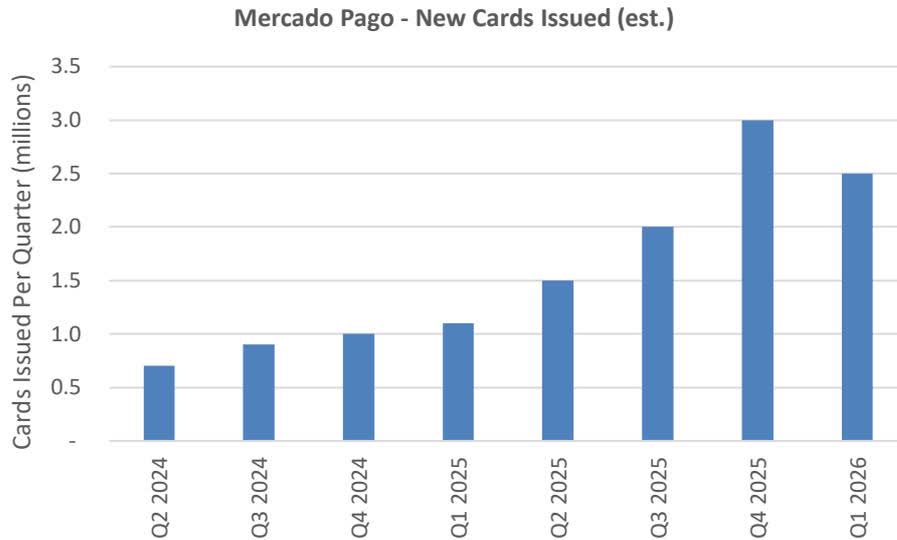

The second initiative is MELI's rapidly expanding credit card portfolio. Over the years, MELI initially focused on short-duration loans for the underbanked. More recently, it has moved upmarket, serving a higher-quality middle-income customer base and steadily laying the foundations for a broader Latin American bank.

Fast-growing loan books are a double-edged sword. When any loan is extended, MELI (or any bank in that manner) prudently recognises an upfront provision for expected credit losses rather than waiting for the default to occur. Faster growth, therefore, mechanically creates higher upfront provisions which hit the income statement immediately. With the credit book growing at roughly 87% YoY ³ , this depresses current reported profitability.

Mercado Pago - New Cards Issued ((est. ))

The obvious risk is that the book proves to be of poor credit quality and today's growth becomes tomorrow's credit problem. That is the right question to ask. However, based on our analysis today, provisioning appears adequate.

The third initiative is cross-border trade, which links MELI's consumers directly to Chinese and US suppliers. We think this is another S-curve that demonstrates the strength and optionality of the MercadoLibre ecosystem.

Consider the challenge from a supplier's perspective. A Chinese manufacturer trying to sell into Brazil, Mexico, Argentina, or Chile faces a market on the other side of the world, with different languages, payment systems, logistics infrastructure, tax regimes, customer service expectations, and returns processes.

That is a hard problem to solve alone, and so MercadoLibre is turning those multiple friction points into a product. Borrowing from models pioneered by companies such as Pinduoduo (PDD), it now offers semi-managed and fully-managed cross-border solutions. In the semi-managed model, the supplier can drop product into a MercadoLibre warehouse in China. In the fully-managed model, MercadoLibre can handle pricing, shipping, marketing, and customer fulfilment on behalf of the supplier.

This is the pattern we like to see, where it leverages existing infrastructure (an investment cycle from a decade ago) to attack adjacent opportunities. Logistics, payments, credit, advertising, and merchant services are not separate businesses bolted on. They are mutually reinforcing layers of the same ecosystem.

That is why we are less concerned by near-term margin pressure than the market appears to be. MercadoLibre is not simply spending to defend its current business. It is investing to make the next version of the business larger, harder to replicate, and more valuable.

So, where else in our portfolio are companies going into 'building mode'?

Tencent: Sacrificing 4.5 percentage points of operating margin to invest in new AI initiatives that sit atop one of the most formidable distribution systems in China.

We Buy Cars: Increased its footprint by 23% over the last two years. The investment is impacting margins and free cash flow today, but if returns on capital follow previous locations, we anticipate a substantial earnings lift next year as these new locations mature.

Roblox (RBLX): Took the difficult but welcome decision to improve age identification using AI. Predictably, bookings have suffered, but we believe this will vastly improve network effects and safety for all users.

Karooooo (KARO): has invested significantly in its sales organisation to accelerate its business in South-East Asia. Cartrack has one of the most enviable unit economics in the sector and is unlikely to be disrupted by AI.

Blu Label Unlimited (BLU): Restructuring and simplification are ongoing, and we anticipate this process will take about 18 more months. We remain hopeful for a repurchase announcement with the 2H26 results. Additionally, BLU plans to launch a unified voucher within the next six months, which will significantly change the company's working capital dynamics.

2022 was an exceptionally tough year for us, and yet it was the most fruitful time to deploy capital. That sounds odd, but it is often how long-term investing works. The best sowing rarely feels good at the time. It happens when prices are falling, confidence is scarce, and the temptation to optimise for reported comfort is strongest.

Since then, market participants have had to contend with sharply higher interest rates, the Russia-Ukraine war, Trump 2.0, tariffs, China decoupling, and now the war in Iran. The headlines have not lacked for drama.

The more important question is: what did the companies do?

A few examples from that 2022 vintage:

The common thread is that these companies had to go through an investment cycle, and the market hated it. Their management teams played the right game. They invested, adapted, endured, and compounded through a period when the market was far more interested in near-term discomfort than long-term potential.

Over time, investment returns are ultimately driven by revenue growth, earnings growth, and the durability of the opportunity set. Narratives matter in the short run. Fundamentals matter in the end.

In aggregate, we believe our portfolio of builders is now available at attractive valuations. Individually, they are not all the same bet. They have different risks, different time horizons, and different failure modes. Some will work, and a few, where we are wrong, will not.

But this is the game we are playing.

Let's Make "Long-Term" Great Again! (Thank you for your attention to this matter).

Once again, we remind co-investors that our personal and family wealth is in the very same funds as yours. We inherently have a multi-decade perspective on how to grow our capital alongside yours.

P. S. The SaltLight Global Opportunity Fund , our USD-denominated global portfolio, is now operational and is approved under section 65 of the Collective Investment Schemes Control Act, 2002, for solicitation of South African investors. Please reach out if you are interested in learning more*.

David Eborall

Portfolio Manager

Boutique Collective Investments (RF) (PTY) ("BCI") Ltd is part of the Apex Group Ltd. BCI is a registered Manager of the Boutique Collective Investments Scheme, approved in terms of the Collective Investments Schemes Control Act, No 45 of 2002 and is a full member of ASISA. Collective Investment Schemes in securities are generally medium to long-term investments. The value of participatory interests may go up or down and past performance is not necessarily an indication of future performance. BCI does not guarantee the capital or the return of a portfolio. Collective Investments are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees, charges and maximum commissions is available on request. BCI reserves the right to close the portfolio to new investors and reopen certain portfolios from time to time to manage them more efficiently. Additional information, including application forms and annual or quarterly reports, can be obtained from BCI, free of charge. Actual annual figures are available to the investor on request. Performance fees are calculated and accrued on a daily basis based upon the daily outperformance, in excess of the benchmark, multiplied by the share rate and paid over to the manager monthly. Performance figures quoted for the portfolio are from Morningstar, as at the date of this document for a lump sum investment, using NAV-NAV with income reinvested and do not take any upfront manager's charge into account. Income distributions are declared on the ex-dividend date. Actual investment performance will differ based on the initial fees charge applicable, the actual investment date, the date of reinvestment and dividend withholding tax. BCI retains full legal responsibility for the third party named portfolio. Although reasonable steps have been taken to ensure the validity and accuracy of the information in this document, BCI does not accept any responsibility for any claim, damages, loss or expense, however it arises, out of or in connection with the information in this document, whether by a client, investor or intermediary. This document should not be seen as an offer to purchase any specific product and is not to be construed as advice or guidance in any form whatsoever. Investors are encouraged to obtain independent professional investment and taxation advice before investing with or in any of BCI's products. Access the BCI Privacy Policy and the BCI Terms and Conditions on the BCI website ( www. bcis. co. za ). Full details and basis of the awards is available from the manager. SaltLight Capital Management (PTY) Ltd (FSP no 48286), is authorised under the Financial Advisory and Intermediary Services Act 37 of 2002 Trustee: Standard Bank Custody and Trustee Services Division is the appointed trustee. *The SaltLight Global Opportunity Fund is a separate portfolio from the SaltLight BCI Worldwide Flexible Fund: while it draws on the same investment philosophy and research process, its mandate, currency, fees, tax treatment and risk profile may differ, and the performance of one fund is not indicative of the other. For the Minimum Disclosure Document, fee schedule, prospectus, and details of the South African representative appointed under section 66 of the Act, please reach out.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。