master1305/iStock via Getty Images

Big winners are exciting. Every investor loves to talk about their “double baggers” and home runs, but perhaps the more effective means of beating the market is the avoidance of bad investments.

At 2nd Market Capital, we emphasize digging into management teams, balance sheets, debt covenants, and any other subtle aspect that can cause a stock to implode. Avoiding disaster allows one’s winners to accrue toward steadily improving account value.

With that in mind, we built and continuously update a list of REITs to avoid. These are companies that appear opportunistic at first glance, but a deeper dive reveals significant risks to shareholder value. The full list on Portfolio Income Solutions currently consists of 14 REITs.

This article will focus specifically on Community Healthcare Trust Incorporated (CHCT).

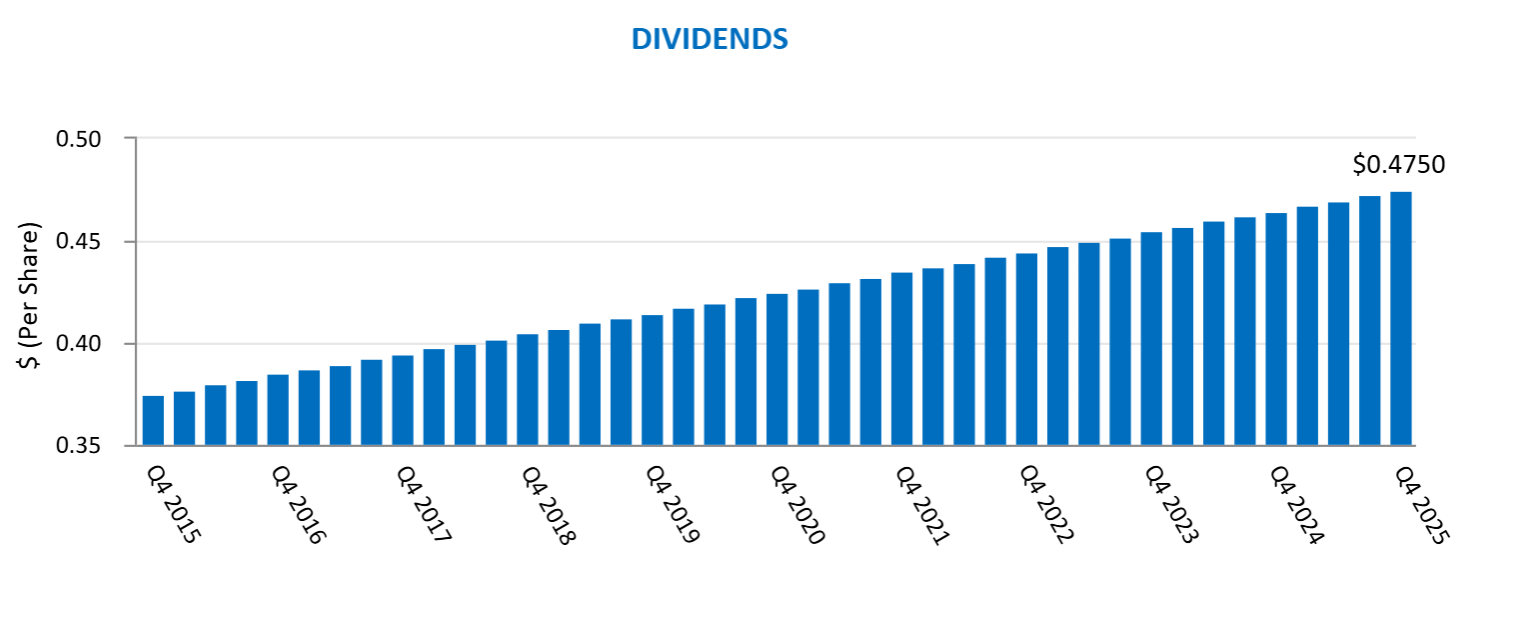

CHCT looks tantalizing with an 11.15% dividend yield. It has a nearly perfect dividend history with continuous raises.

CHCT

To top it all off, the dividend appears fully covered with an 88.4% AFFO payout ratio on 2025 AFFO.

However, we think a dividend cut is quite likely due to 5 key problems:

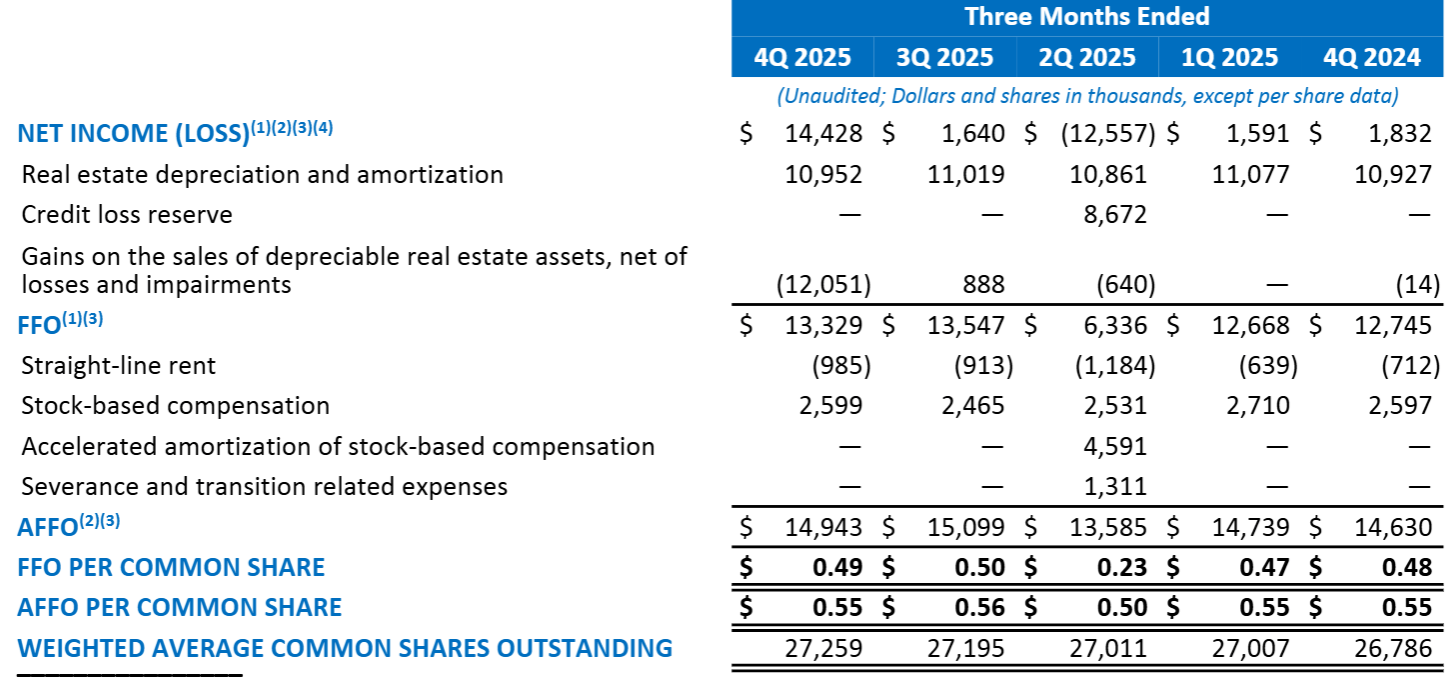

2025 G&A was $25.095 million.

CHCT

This is a company with a market cap of $460 million, so G&A in a single year was 5.4% of market cap. 2025 rental revenue was $121.351 million, so G&A was almost 21% of revenue.

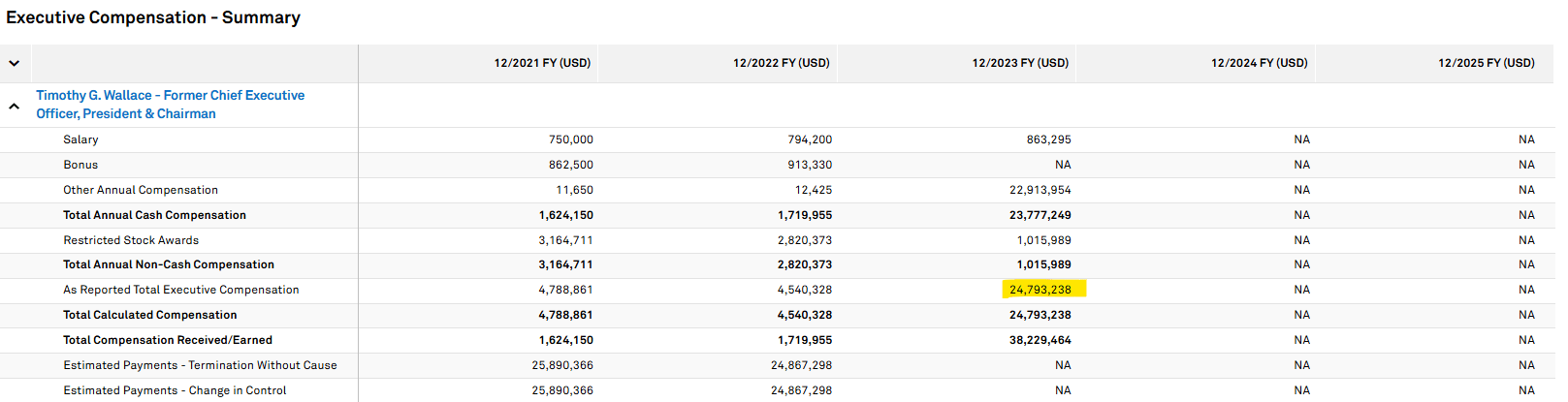

That level of overhead expense is so hard to overcome. It is imperative that small REITs operate with extreme efficiency. CHCT fails to do this, instead electing to pay executives large salaries and bonuses. We had hoped the company learned its lesson after the egregious $24.7 million former CEO Timothy Wallace received in 2023.

S&P Global Market Intelligence

Unfortunately, really high G&A resurfaced in 2025.

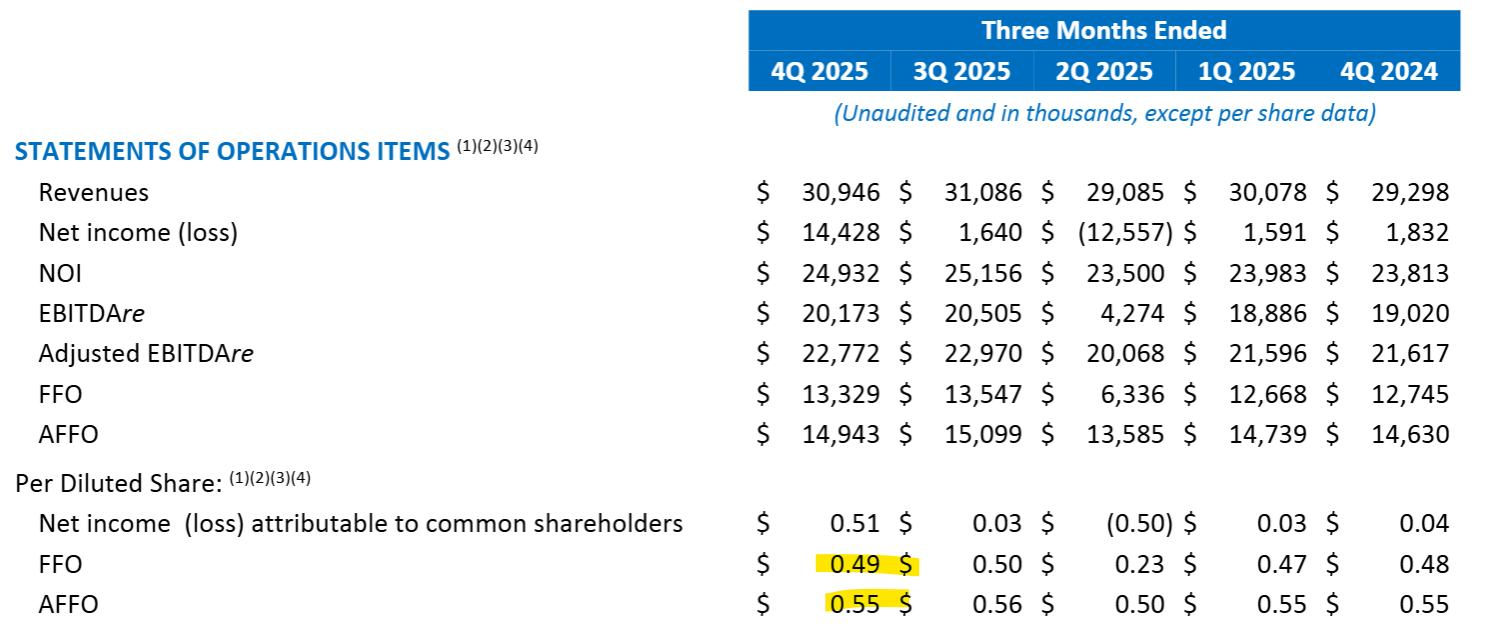

CHCT’s reported AFFO is consistently higher than its FFO.

CHCT

AFFO is generally going to be lower than FFO, especially in a high-capex asset class like healthcare. AFFO being higher should immediately raise red flags and encourage digging into the accounting.

Here is the reconciliation of FFO to AFFO.

CHCT

A whopping $14.896 million stock comp was added back to AFFO in 2025. With 27.259 million shares outstanding, that is fully $0.54 per share of stock comp add-backs.

So while the reported $2.16 AFFO in 2025 appears to cover the $1.91 dividend, true AFFO was only $1.62.

True AFFO payout ratio is 118%.

A tenant occupying 6 behavioral health facilities stopped paying full rent, resulting in significant impairment as described in an Earnings Report:

“During the three months ended June 30, 2025, the Company recorded a credit loss reserve on its notes related to a geriatric behavioral hospital tenant totaling approximately $8.7 million. During the three months ended June 30, 2024, the Company recorded an $11.0 million credit loss reserve related to its notes receivable with this geriatric behavioral hospital tenant. Because these notes are incidental to the Company's main business, the Company added back these reserves in its calculations of FFO and AFFO.”

This $8.7 million impairment was added back into FFO and AFFO. Inclusive of the impairment, AFFO would have been another $0.32 per share lower.

As described in our previous article on CHCT, they operate in a high-risk segment, so tenant problems are a higher-than-normal risk. The tradeoff inherent to their business model is that CHCT gets to acquire properties at very high cap rates (the positive) in exchange for the properties being higher risk due to some combination of location, tenant, type, and size.

CHCT was previously able to acquire in a highly accretive fashion as they traded at a very high multiple, which gave them cheap equity capital. The stock price has since collapsed, eliminating the opportunity to issue equity accretively.

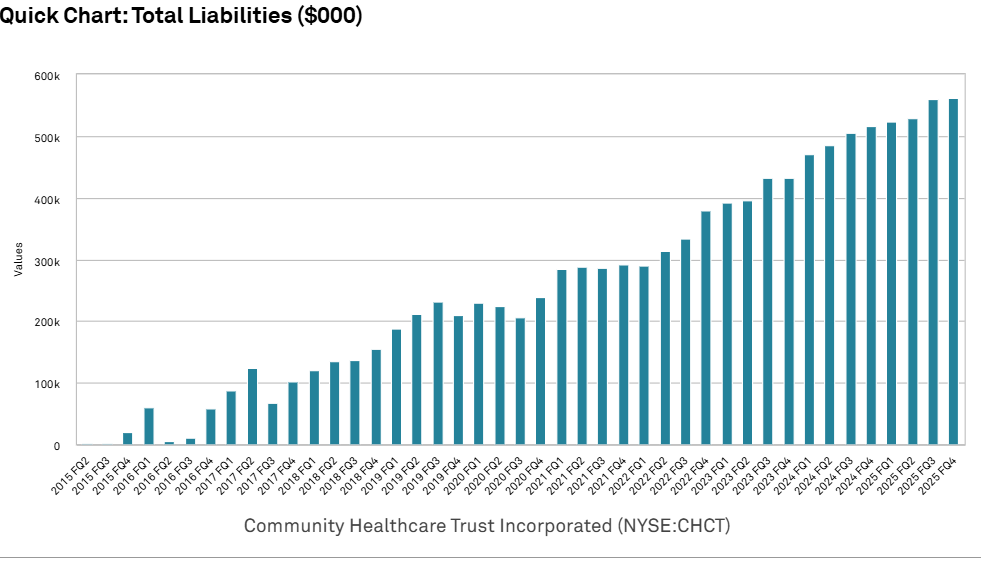

With the equity faucet cut off, CHCT has had to shift to funding acquisitions with some combination of asset sales and debt.

Asset sales have high cap rates, making spreads on new acquisitions less accretive. To preserve accretion, CHCT seems to have engaged in significant debt issuance.

S&P Global Market Intelligence

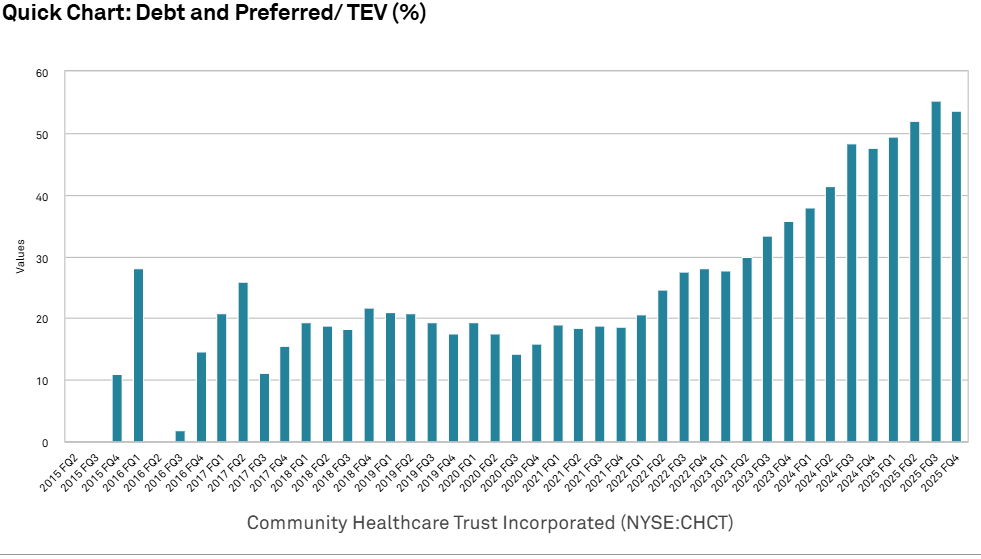

Debt ratios have increased considerably, with debt to enterprise value jumping to over 50%.

S&P Global Market Intelligence

This alone would not be concerning.

REITs can change their debt level as a basic capital allocation decision. To the extent debt is measured to be the most effective source of capital, it can sometimes be the correct decision to lever up.

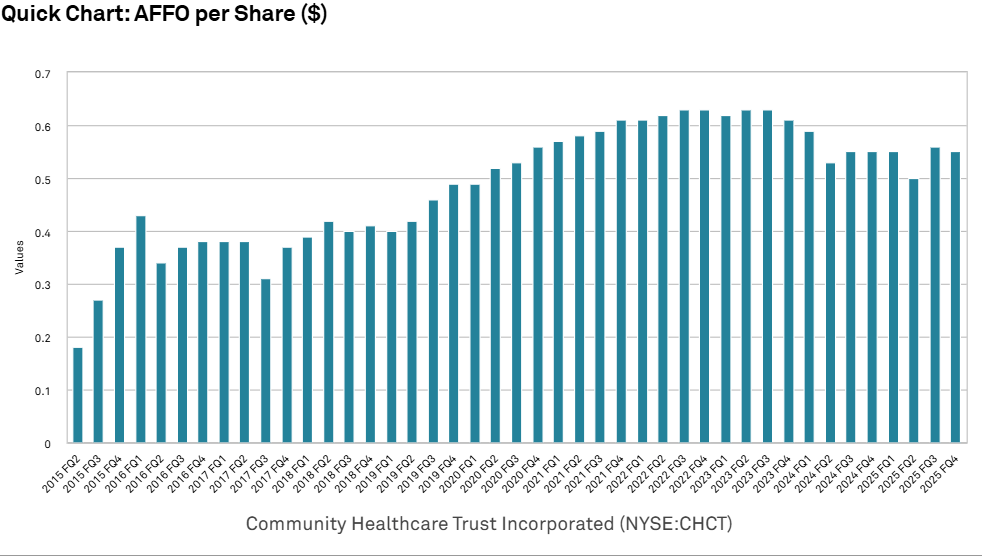

However, when a REIT levers up, it should result in significant AFFO/share accretion.

This is not the case for CHCT, which saw its AFFO/share falter at the same time debt ratios increased.

S&P Global Market Intelligence

Higher debt and lower AFFO/share is a bad trajectory.

If one properly adjusts for capex, impairments, and G&A, the dividend is not even close to being covered. CHCT can elect to keep paying it, but doing so would be financed by more debt, which is already becoming a problem.

Thus, I don’t know when the dividend cut will happen, but it seems inevitable to me unless there is a remarkable fundamental turnaround in which CHCT can suddenly lease up its vacant space.

When a company’s board signs off on massive pay packages for management while shareholders suffer, it is probably not a good place to invest. Operating efficiency remains one of the most important aspects of REIT profitability, especially for small caps. Don’t forget to do due diligence management before buying.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。