Klaus Vedfelt/DigitalVision via Getty Images

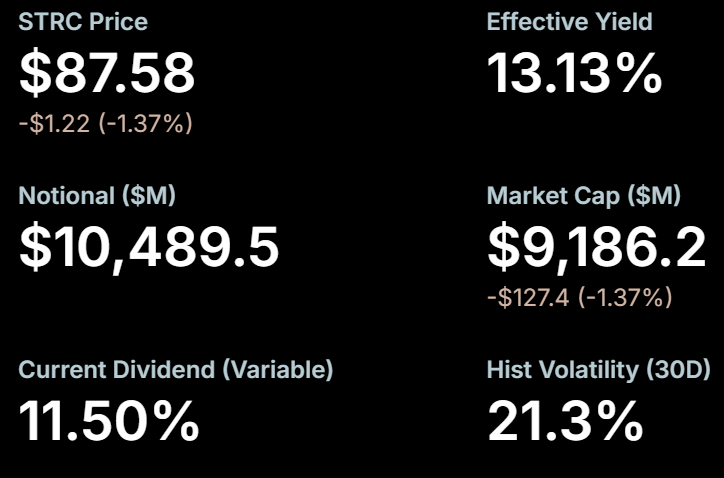

Strategy (MSTR) preferreds have attracted a whopping $14.5B of total investment. STRC, otherwise known as Stretch, is the largest at $10.5B notional value, so we will spend the bulk of this article putting it through the standard due diligence that should be performed on any preferred. In the process, we highlight multiple points of failure that subject investors to undue risk. We will conclude with alternative ways investors can achieve similar income, but at much lower risk.

There are dozens of aspects to note in full due diligence, but at the most basic level, a preferred investor wants to know 3 things:

With a current yield of nearly 13%, Stretch may look appealing to those seeking high income. However, due to multiple major risk factors, which we will discuss below, I think the total return will be far south of 13% and, in my opinion, likely negative.

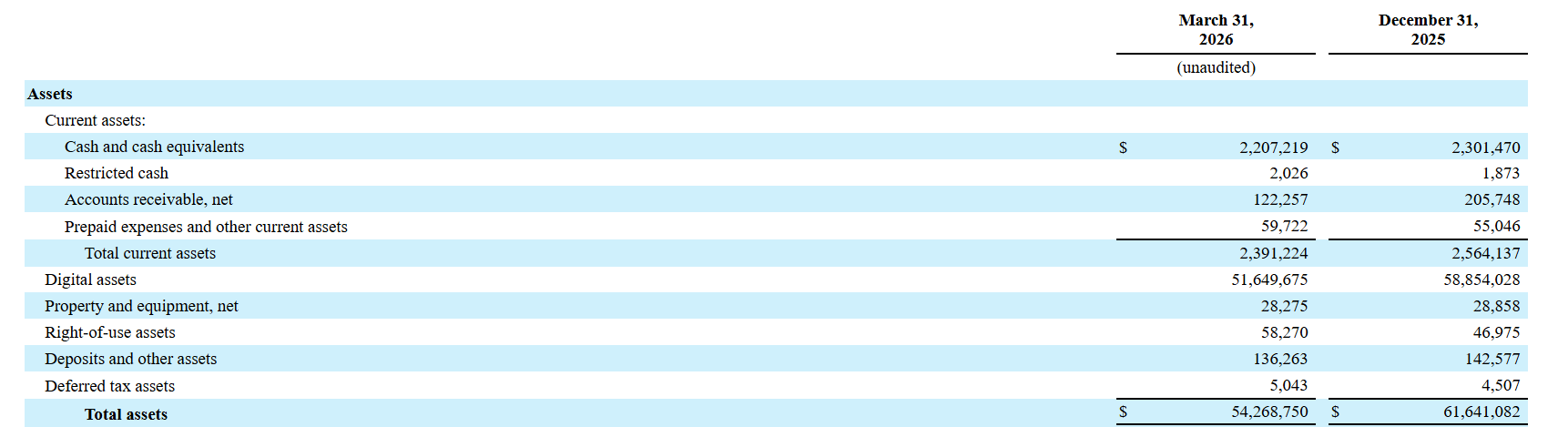

Strategy has about $8.6 billion of liabilities and $14.5B of preferred obligations. This is reasonably well covered by $54.3B of assets.

I would generally consider a roughly $31B equity cushion junior to the preferreds to be ample coverage regarding liquidation preference. However, in finance there is a concept called risk shifting, which causes various risks to impact various tranches differently.

Common equity has bi-directional risk. It participates in both upside and downside scenarios. Therefore, its expected value is not all that affected by volatility so long as the scenario weighted average is positive.

Preferred equity has 1 directional risk. Its upside is capped essentially at the par value, while its downside can go all the way to total wipeout. Therefore, higher volatility is unequivocally bad for preferreds.

This concept is relevant to Stretch because nearly all of Strategy’s assets consist of a single volatile asset - Bitcoin (BTC-USD).

10-Q

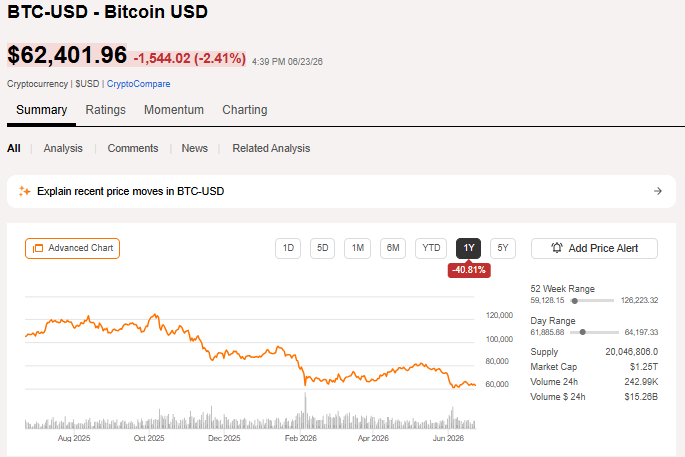

Bitcoin has always been highly volatile, and projections about its future are binary. Many bulls still claim it will go to $1 million per bitcoin, while bears say it has $0 intrinsic value and will eventually go to $0.

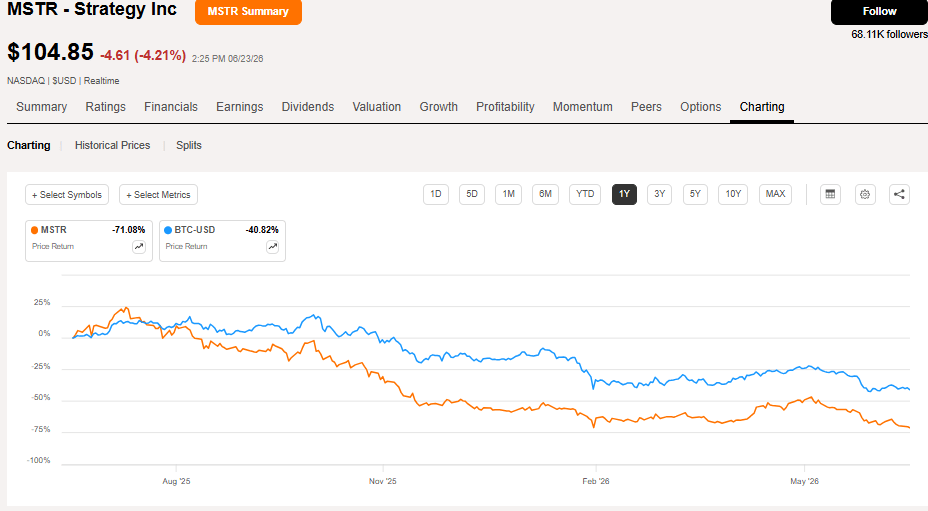

Bitcoin previously experienced a massive surge, making it a multitrillion-dollar asset class, while the recent pricing has been less favorable, down 41% in the last 52 weeks.

SA

Depending on one’s view of the chances of various outcomes, this roller coaster could theoretically be a good scenario weighted expected value for common equity of MSTR, but the volatility is clearly bad for preferreds.

A preferred holder does not share in the upside if BTC-USD goes to $1 million per coin, but it fully partakes in the losses if BTC-USD goes to $0.

So while the $54.3B of assets are sufficient in size to cover the preferred, they are highly volatile and completely undiversified. As such, the chance of liquidation preference becoming uncovered is much higher than one would normally expect given the magnitude of assets.

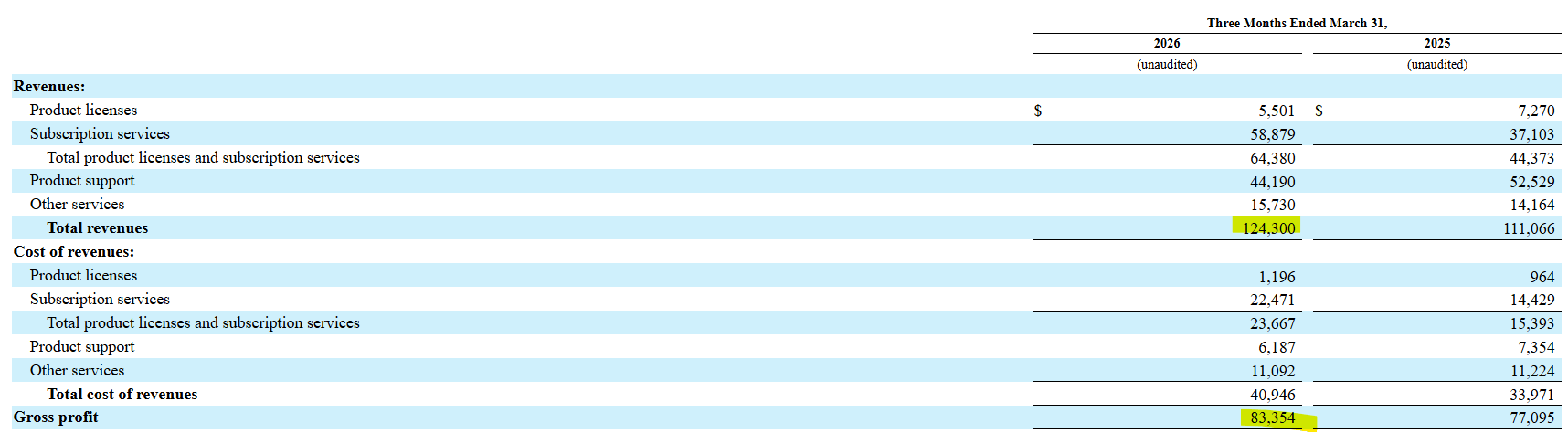

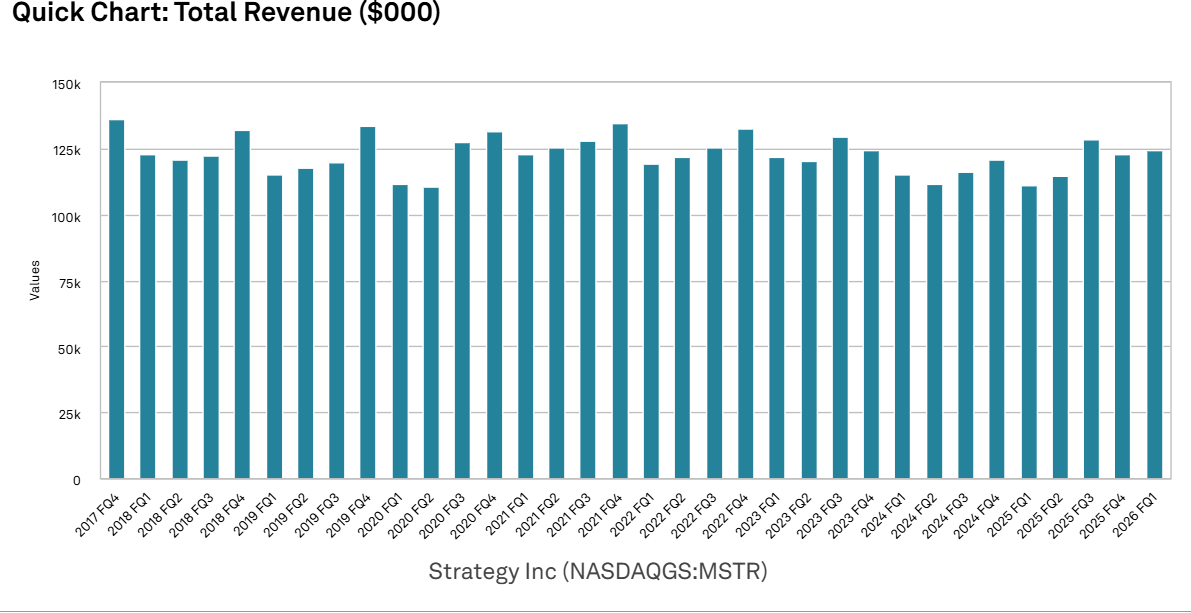

MSTR has some minor cash flow from product licenses and subscriptions, but it is almost non-existent relative to the size of the company. Gross profit in Q1-2026 was $83 million.

10-Q

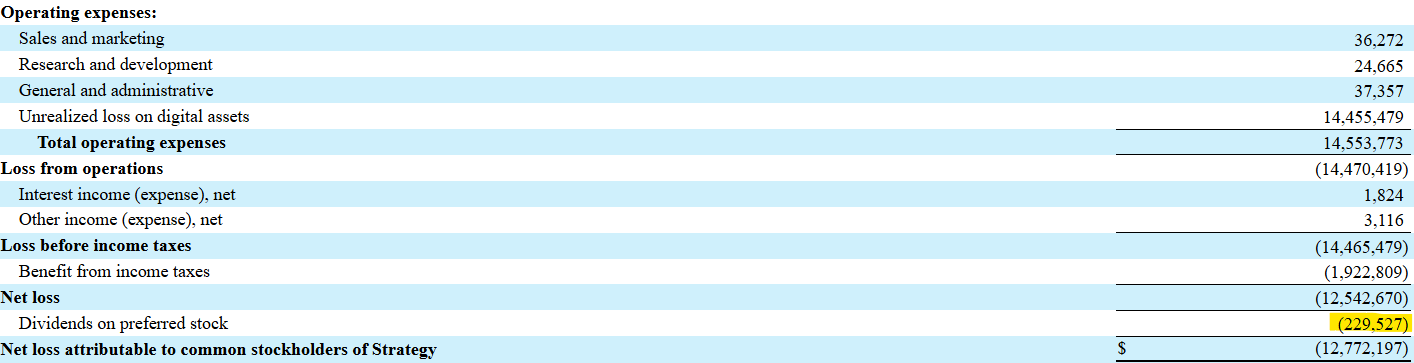

Operating expenses exceeded net revenue at about $98 million for the quarter between sales and marketing, R&D, and G&A.

10-Q

We will ignore the $14.45 billion loss on the mark-to-market of Bitcoin.

Net earnings are negative, yet they have $229.5 million of quarterly preferred dividends to service. Perhaps worse is that there is no real business model with which to generate recurring cash flow. Note that revenue has not risen even as the company has become much larger.

S&P Global Market Intelligence

Thus, preferred dividends are primarily funded from 2 buckets:

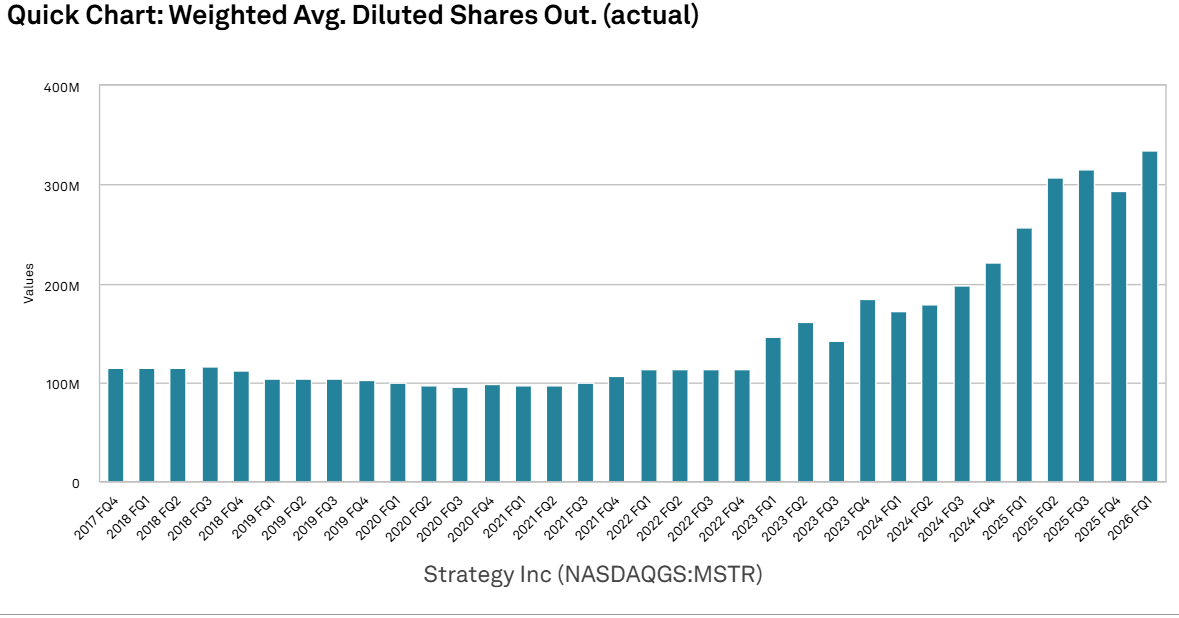

Both of these are short-term solutions that require things to go a certain way. Equity issuance was highly accretive for MSTR when they were trading at a huge premium to book value. They could issue shares well above book value and use the proceeds to buy more Bitcoin. Each existing shareholder would end up with more Bitcoin per share than they had prior to the equity issuance.

The strategy worked wonderfully when Bitcoin was soaring and the market was broadly enthusiastic about the asset class. Strategy traded at a huge premium to book, which facilitated massive issuance of equity.

S&P Global Market Intelligence

However, in recent periods, Bitcoin has been dropping. As MSTR’s business is so levered to the success of BTC-USD, MSTR dropped even harder.

SA

With its corrected stock price, its premium to book has evaporated.

SA

Trading around book value for the past 7 months, Strategy pivoted to preferred issuance.

S&P Global Market Intelligence

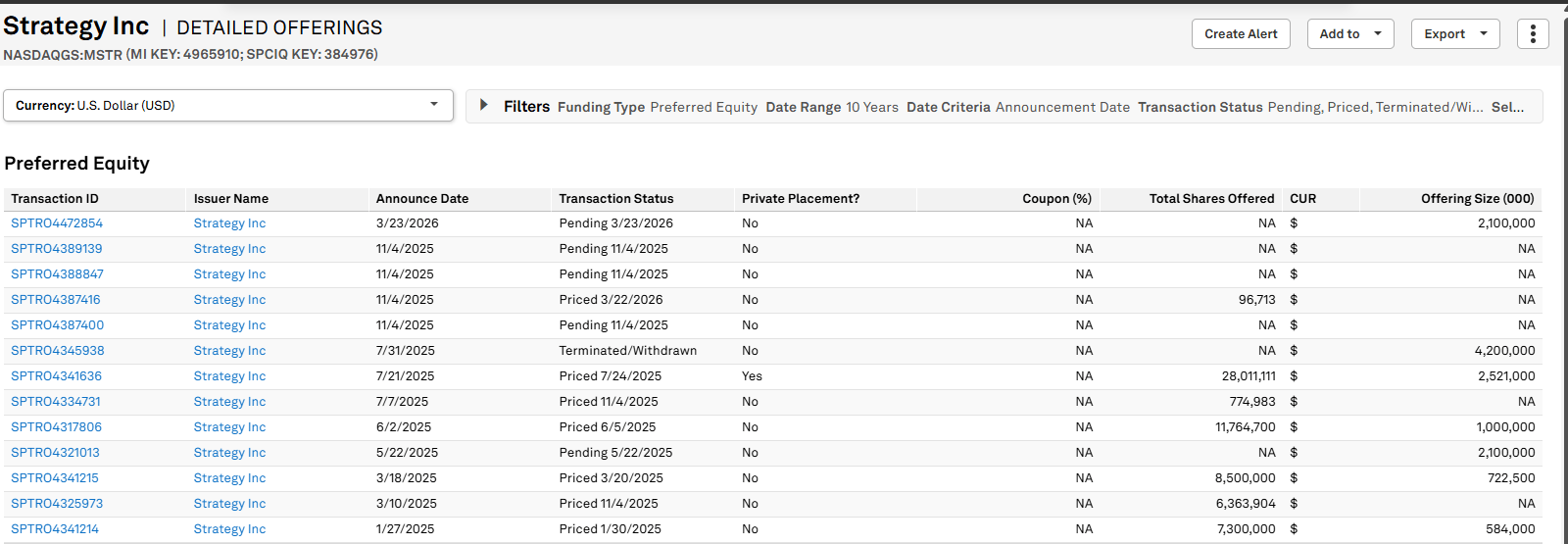

Their website details the outstanding volume of each preferred issue. STRC is approaching $10.5B

Strategy

Source: Strategy

Additionally, they have

Each of these are high coupons.

As the size of the preferred stack increases relative to the size of the overall company, it creates an increasingly awkward cash flow situation.

Servicing preferreds with coupons around 10% plus or minus a couple percentage points is difficult when the proceeds of those preferreds were invested in a zero percent yielding and zero cash flow instrument.

To make the math work, MSTR needs BTC-USD to go up. As the preferred stack gets larger, the company needs BTC-USD to go up at a faster and faster pace just to break even.

A speculative asset like BTC-USD is already high risk, but when the speculator needs it to work on a specific timetable, it becomes even more risky.

Again, going back to the risk-shifting concept, this sort of binary outcome is not beneficial to preferreds. A preferred wants dividends to be supported by steady cash flows generated by reliable and hopefully diversified sources.

We at 2nd Market Capital invest in a variety of variable rate preferreds. The terms of the variable rate are usually well defined in the preferred’s charter.

For example, AGNC Investment Corp preferred (AGNCO) pays variable dividends at a rate equal to 3-month SOFR +26.16 basis point adjustment +499.3 basis points.

The terms are clearly defined, and SOFR is public information, so investors can know how much dividend they will be entitled to. Preferreds across the REIT spectrum have similar terms where the dividend amount, whether fixed or variable, is very clearly defined.

Strategy has more nebulous terms on its preferreds, with the dividend amount largely coming down to management discretion.

Per the 10-Q:

“We may, at any time in our sole and absolute discretion, and without the consent of any holder of STRC Stock, choose to reduce the monthly regular dividend rate per annum to the maximum extent permitted by the terms of STRC Stock, without regard to the impact that reduction may have on the trading price or value of STRC Stock. If we reduce the monthly regular dividend rate per annum, then the trading price or value of STRC Stock could decrease significantly. If you hold STRC Stock at the time of such a decrease, the value of your investment could materially depreciate, and you may not be able to resell your STRC Stock at favorable prices, if at all. Moreover, the mere existence of our right to unilaterally reduce the monthly regular dividend rate per annum could, in itself, and without any actual reduction in the monthly regular dividend rate per annum, cause STRC Stock to trade at prices below those that may otherwise be expected.”

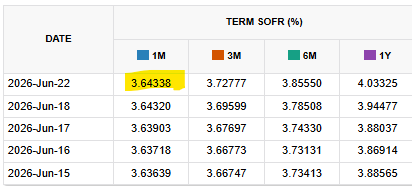

The minimum rate to which they can reduce it is SOFR. It can actually go below SOFR, though, as they do not have to raise it if SOFR rises. Again, per the 10-Q:

“If we reduce the monthly regular dividend rate per annum to the minimum dividend rate of the monthly SOFR per annum, and the monthly SOFR per annum thereafter increases, we will have no obligation to increase the monthly regular dividend rate per annum to the new monthly SOFR per annum.”

So investors are buying a preferred that is stated as having an 11.5% coupon, but management can unilaterally take that down to SOFR, which right now is about 3.64%.

CME Group

STRC is already trading substantially below par, but if the dividend gets cut to SOFR, math would suggest the price would crater.

STRC would have to trade down to $31.65 for it to trade at a current yield of 11.5% (the now-stated coupon). Thus, we see about 60% downside on a dividend cut, which management can unilaterally decide to enact.

For now, management’s stated goal is to adjust the dividend to such a coupon level that keeps the price around $100. If BTC-USD keeps falling as it has for the past year, the financial strain of the high dividend could be enough to encourage management to make the cut. In theory, a cut could be viewed as fulfilling their fiduciary duty to MSTR investors.

STRD also has fairly dangerous terms for investors.

Again, per the 10-Q:

“Dividends on STRD Stock are discretionary and not cumulative. If our board of directors or any duly authorized committee thereof does not declare a dividend on STRD Stock in respect of a dividend period, then no dividend will be deemed to have accrued for such dividend period, be payable on the applicable dividend payment date or be cumulative, and we will have no obligation to pay any dividend for that dividend period”

Non-cumulative dividends make the dividends functionally not senior to the common. They could just stop dividends on STRD, and the missed payments would not accrue as a liability, nor would they add to the liquidation preference.

MSTR’s preferreds are among the most dangerous we have come across.

I can entirely understand the desire to find high income investments. There are just better sources of high yield available.

In a previous article, we discussed how we built an 11.33% yield on invested capital through disciplined selection of fundamentally sound preferreds. I would like to take the time here to contrast aspects of these preferreds with STRC.

Agency mREIT preferreds such as AGNCZ, which we wrote about here, are attached to companies with underlying assets that are fully backed by U.S. government agencies. If the mortgages were to default, the company would be reimbursed. This keeps a rock-solid asset base underneath the preferreds. It cannot be eroded by something as simple as the market selling off Bitcoin.

Equity REIT preferreds such as those of Gladstone Land (LANDO) and (LANDP) which Ross Bowler wrote about here, are funded by recurring and reliable cash flows generated by the underlying properties. In this case, the farmland is long-term leased to a diversified batch of tenant farmers. These recurring cash flows fully cover the preferred dividends. Unlike with Strategy where capital issuance funds the dividends.

Don’t buy a preferred just because it has a juicy yield. Fundamentals and terms matter. Consider switching to high yield preferreds with better terms and dividend coverage.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。