monsitj/iStock via Getty Images

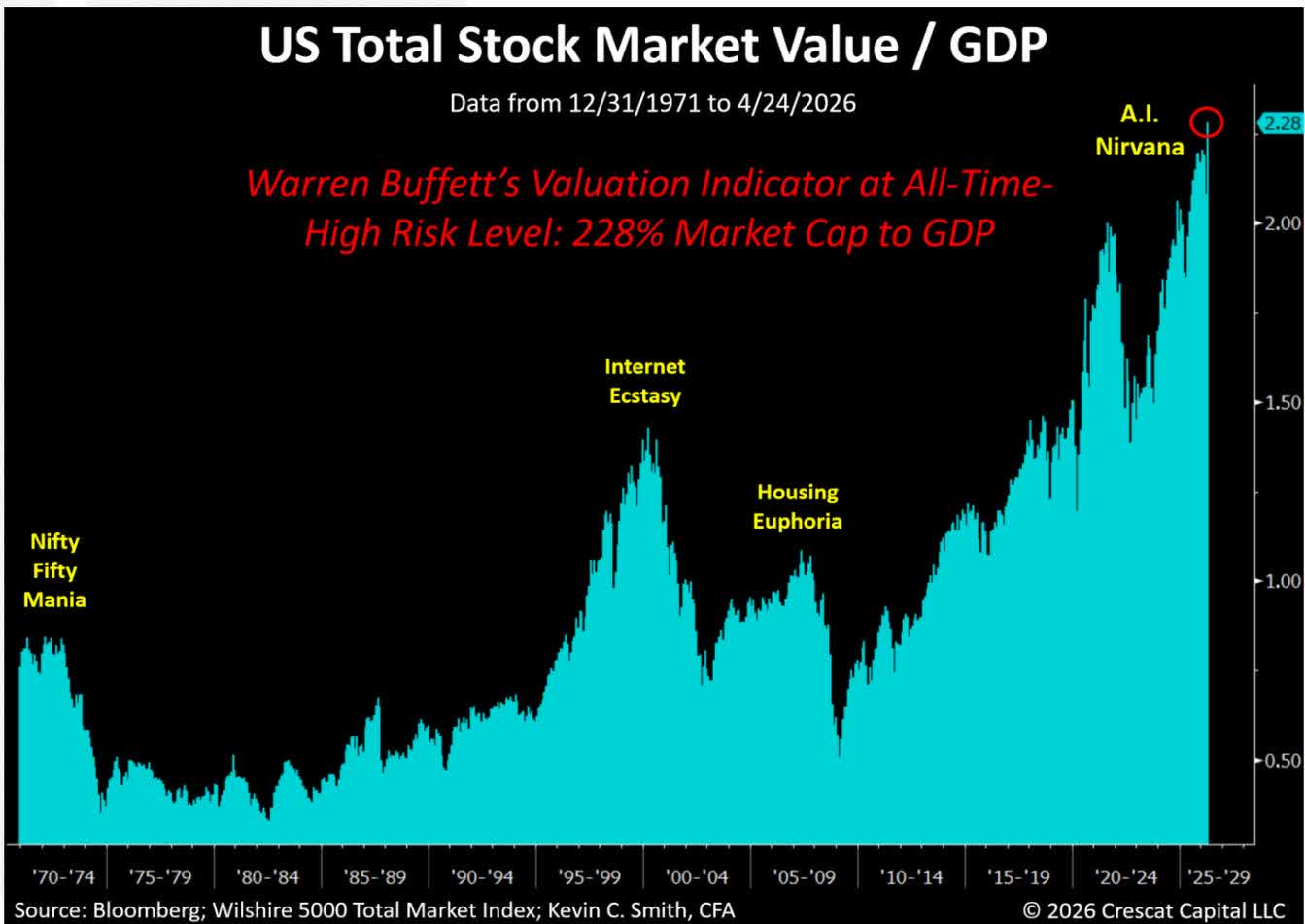

The US stock market is historically overvalued, posing a major potential risk to investors at large. The extent of the bubble is illustrated by Warren Buffett's favorite valuation risk measure, total stock market value to GDP. It just reached a new high, 228%, 59% higher than it was at the peak of the Internet boom in 2000!

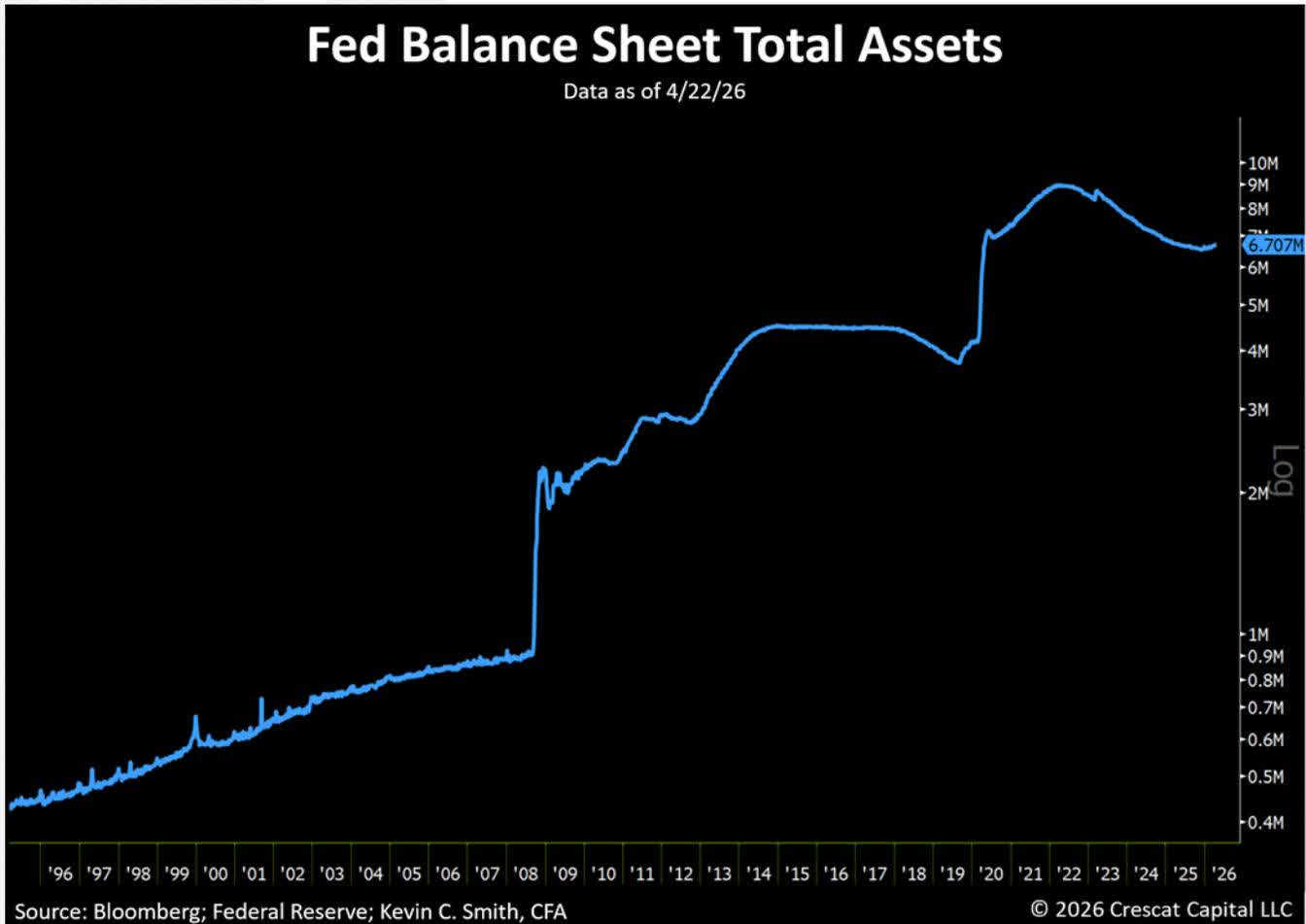

We see three catalysts at play simultaneously:

Each of these drivers has historic parallels including:

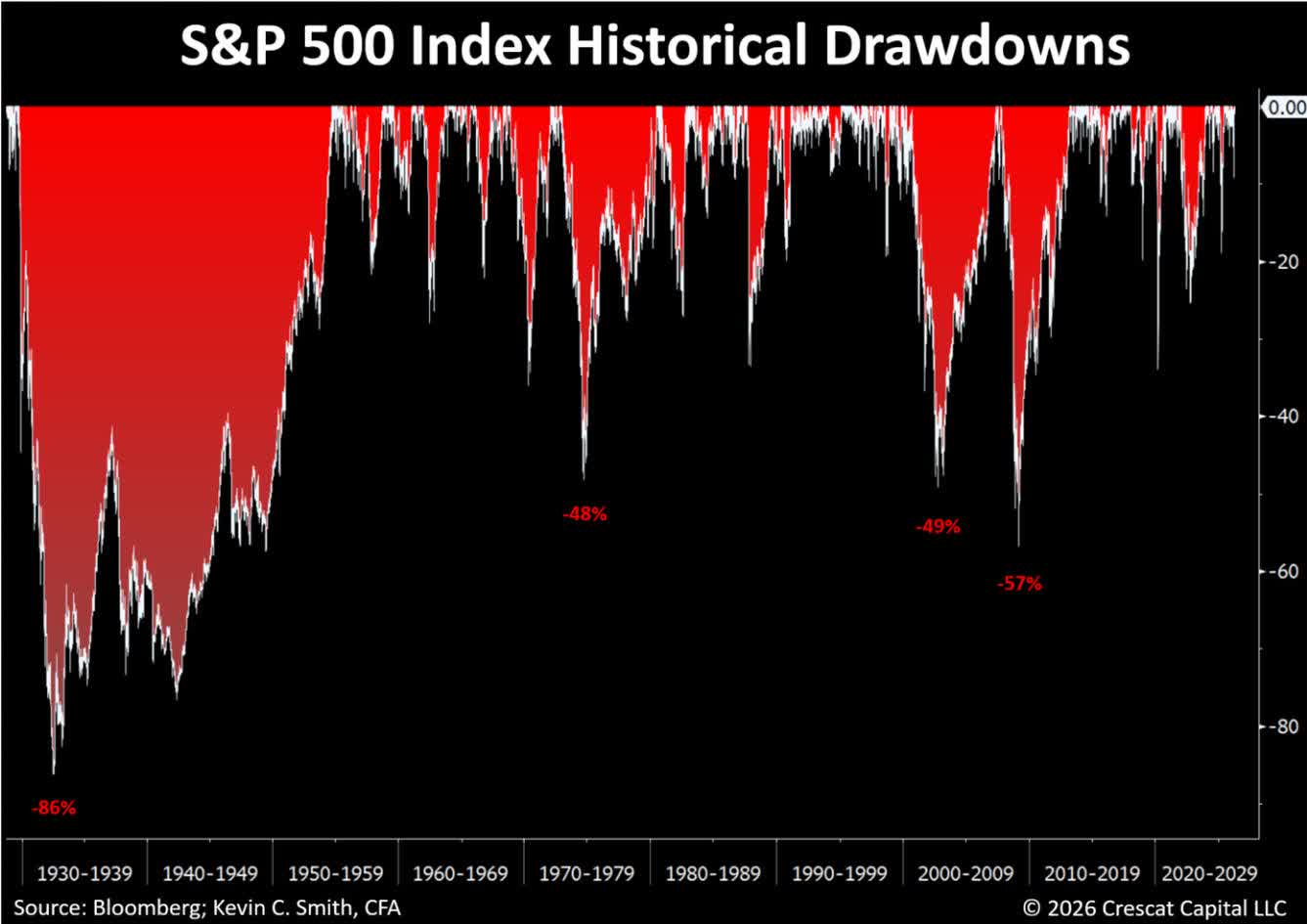

This chart is a reminder that the S&P 500 goes down too, sometimes a lot. The numbers show the max drawdowns of the four biggest bear markets in the index's history. It's been almost 97 years since the start of the biggest one to date. The red shaded areas show that amount of time the market spends recovering from a drawdown, just to get back to its prior high.

From all-time highs in price, combined with historic high fundamental valuations, and macro triggers abounding, the risk of a stock market meltdown on the near-term horizon is as high as we have ever seen it.

On March 31, 2026, US financial markets began to reverse course. This was the start of the rally built on hope that the Iran war may be coming to an end. The S&P 500s 14-day Relative Strength Index (RSI), a momentum oscillator used to identify changes in momentum and price direction, bottomed the prior day at just below 30, by mid-month RSI was back above 70. This marked the second fastest weakness to strength rally in the S&P 500 dating back to 1950.

Dates SPX 14d RSI Days inbetween Market Prev. Market OS to OB Aug. 23, 1982 116.11 73.3 6 OB OS 11.8% April 16, 2026 7,041.28 70.0 11 OB OS 9.9% May 26, 1972 110.66 70.5 12 OB OS 5.3% Nov. 25, 2016 2,213.35 70.7 13 OB OS 5.8% Dec. 16, 1971 99.74 74.0 14 OB OS 9.4% Aug. 14, 1963 71.07 71.2 15 OB OS 4.4% May 5, 1997 830.24 72.7 15 OB OS 11.2% Nov. 20, 2023 4,547.38 71.6 15 OB OS 9.5% Nov. 18, 1952 25.16 71.5 16 OB OS 5.4% July 2, 1959 59.28 71.7 16 OB OS 4.9% Aug. 23, 1960 57.75 72.2 18 OB OS 6.2% July 1, 1964 82.27 72.4 18 OB OS 4.4% Nov. 23, 1962 61.54 73.0 20 OB OS 13.1% April 3, 1968 93.47 70.1 20 OB OS 6.2% Sept. 9, 1968 101.23 70.1 20 OB OS 4.5% July 3, 2019 2,995.82 71.0 21 OB OS 8.4% Nov. 10, 1966 81.89 71.1 22 OB OS 10.6% Nov. 18, 2014 2,051.8 71.3 22 OB OS 9.2% March 31, 1952 24.37 70.3 23 OB OS 5.0% Sept. 26, 1973 108.83 72.0 23 OB OS 7.6%

Note: Data based on daily close and only considers direct rallies where RSI was below 30 points and climbed straight to above 70 points. Source: Bloomberg

The recent rally comes with notable risks. The conflict with Iran remains unresolved. The Strait of Hormuz has opened and closed, then opened and closed, then opened and closed again. Peace talks have stalled multiple times. Meanwhile, WTI & Brent Crude are still up over 40% compared to before the conflict began.

In our assessment, the market appears to be ignoring these ongoing risks and is pricing in a resolution that has yet to materialize. Meanwhile, the conflict persists, and its longer-term economic and geopolitical implications are uncertain.

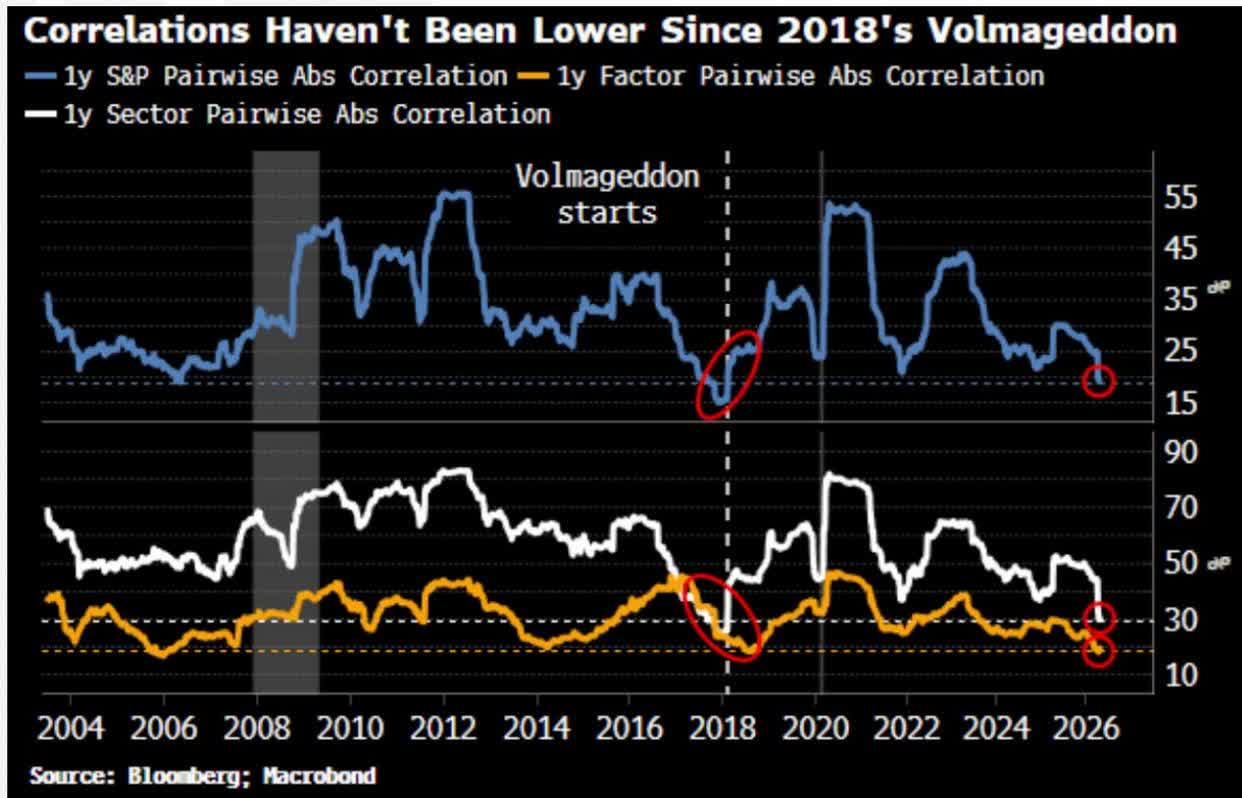

The chart below shows 1-year pairwise absolute correlations of members within the S&P 500 are historically low. In fact, they are the lowest since right before Volmageddon in 2018. This is an indication of complacency with respect to macro risks. Low pairwise correlations mean that over the last year, it has been a stock-picker's market as opposed to a market where stocks move together based on broad economic events. Low pairwise correlations in low volatility environments suggest investors are ignoring potentially systemic risks.

We think cheap gold and silver mining stocks are still the best countercyclical hedge for the long side of investor portfolios in the current and what we see as likely upcoming macro environment that should be dominated by supply-constrained inflationary pressures. The activist metals portfolio remains the largest long exposure across all our funds. We are tilted toward the smaller cap miners with exploration and development projects that, in our analysis, provide extraordinary value and high growth potential compared to owning the metals themselves. We are short the S&P 500 and Nasdaq 100 through put options in our macro and long/short funds. Of all the macro environments historically, we think the decade of the 1970s most closely represents the outlook for the decade ahead.

Though, we think we will also see elements of the Great Depression and the early 2000's tech bust. These were both times when gold miners outperformed dramatically while the broad stock market crashed.

We are short the U.S. dollar and long Japanese yen in our macro funds. Long gold though cheap mining stocks remains our favorite way to short the dollar. However, the current setup in the yen is too good to pass up. The 10-year rate differential between U.S. Treasuries and Japanese Government Bonds historically has been a reliable directional indicator for dollar/yen. The Trump administration favors a weak dollar to reindustrialize the country. The yen is the only major currency that has yet to cooperate though the Bank of Japan seems onboard with the plan from an interest rate policy standpoint.

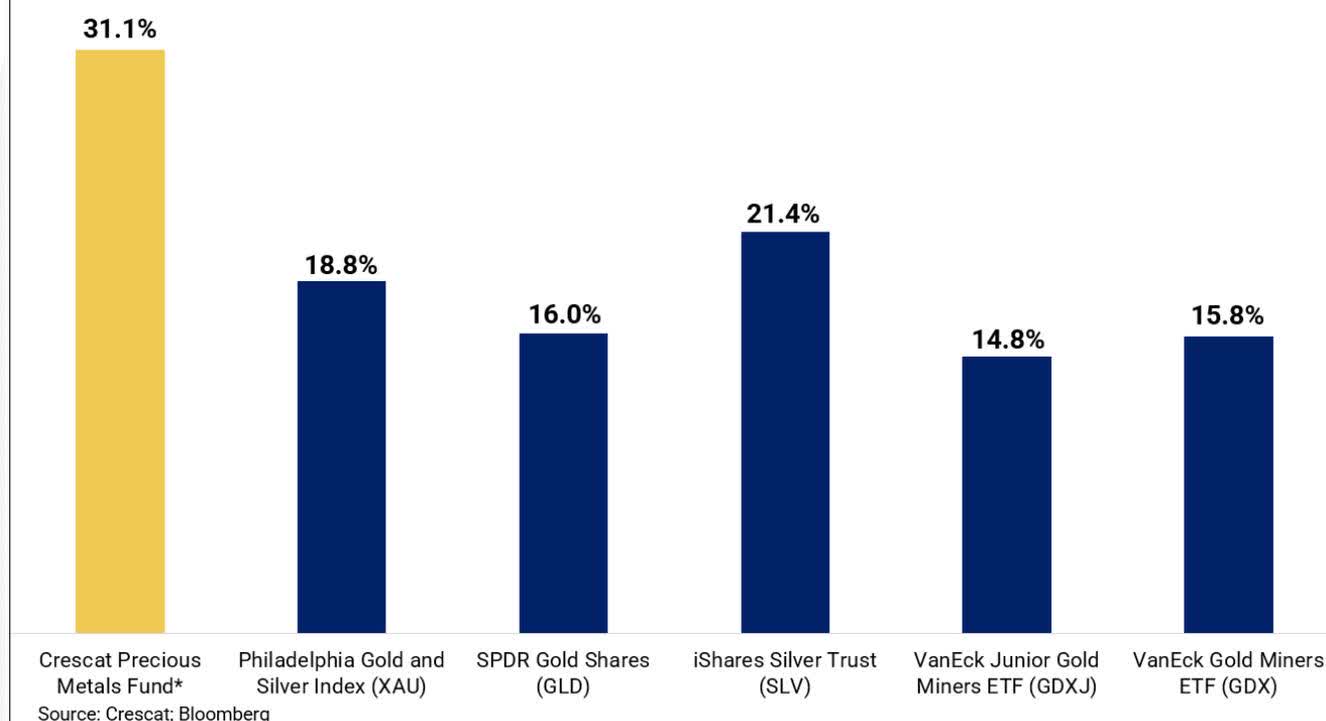

Precious metals mining stocks corrected in March from short-term overbought conditions in February after leading the entire market in 2025 and the first two months of 2026. While our funds were down for the month as a result, we are encouraged to report that all Crescat funds significantly outperformed multiple of the precious metals benchmarks in this pullback. For reference, the VanEck Junior Gold Miners ETF (GDXJ) was down 23.1%, VanEck Gold Miners ETF (GDX) down 20.8%, and the Philadelphia Gold and Silver Index (XAU) down 20.2%. The Crescat Precious Metals Fund has substantially outperformed these benchmarks since inception over five years ago as we show in the chart below. Through March 31, 2026, as it was at year-end 2025, this fund remains the best performing resource-based hedge fund in the eVestment database since its inception, August 1, 2020. We remain highly convicted in our hard asset and precious metals positioning across the firm.

Crescat Precious Metals Fund: Annualized Net Performance vs. Benchmarks Since InceptionAugust 1, 2020 through March 31, 2026 (Estimates)

CRESCAT STRATEGIES VS. BENCHMARK(Inception Date) MARCH YTD ANNUALIZED TRAILING SINCEINCEPTION CUMULATIVESINCEINCEPTION YEARS SINCEINCEPTION 1-YEAR 3-YEAR 5-YEAR 10-YEAR Global Macro Hedge Fund(Jan. 1, 2006) -13.2% -0.4% 57.8% 16.3% 9.6% 7.2% 11.6% 816.2% 20.3 Excluding SCM SP ²(Jan. 1, 2006) -18.3% -6.7% 34.4% 8.9% 5.4% 5.2% 10.5% 653.1% 20.3 Benchmark: HFRX Global Hedge Fund Index -3.0% -0.6% 6.0% 5.0% 2.5% 3.2% 1.5% 35.4% Institutional Macro Hedge Fund(July 1, 2023) -13.1% -0.5% 50.2% - - - 15.6% 48.9% 2.8 Excluding SCM SP ²(July 1, 2023) -16.5% -4.6% 29.7% - - - 8.2% 24.1% 2.8 Benchmark: HFRX Global Hedge Fund Index -3.0% -0.6% 6.0% 5.0% 2.5% 3.2% 5.2% 14.9% Long/Short Hedge Fund(May 1, 2000) -12.9% 0.1% 59.7% 17.4% 8.3% 6.6% 7.9% 616.0% 25.9 Excluding SCM SP ²(May 1, 2000) -17.2% -5.2% 37.6% 10.5% 4.4% 4.7% 6.4% 394.3% 25.9 Benchmark: HFRX Equity Hedge Index -4.4% -1.5% 8.2% 7.4% 5.7% 4.9% 3.1% 119.5% Precious Metals Hedge Fund(August 1, 2020) -12.1% 1.9% 82.3% 33.2% 14.5% - 34.2% 428.8% 5.7 Excluding SCM SP ²(August 1, 2020) -16.2% -3.3% 74.5% 27.5% 11.5% - 31.1% 363.4% 5.7 Benchmark: Philadelphia Gold and Silver Index -20.3% 9.7% 113.8% 43.8% 24.7% - 18.8% 165.0% Institutional Commodity Hedge Fund(July 1, 2023) -12.1% 2.3% 81.8% - - - 31.2% 111.1% 2.8 Excluding SCM SP ²(July 1, 2023) -14.6% 0.3% 73.9% - - - 26.9% 92.5% 2.8 Benchmark: Philadelphia Gold and Silver Index -20.3% 9.7% 113.8% - - - 53.4% 224.6%

Sources: HFR, Inc., NASDAQ, and Crescat Capital LLC. Past performance does not guarantee future results; Investing involves risk, including risk of loss. See additional important disclosures below.

Crescat is pleased to announce that it has hired Bill Pearson, PhD, P.Geo., as Geologic and Technical Advisor to provide professional expertise with respect to the full scope of the firm's activist metals portfolio. With over 50 years of boots-on-the-ground global mining experience (see his bio below), his addition represents a meaningful expansion of our geologic and technical investment research capabilities.

Bill Pearson is an economic geologist with more than 50 years of experience in the global mining industry. He earned a PhD and MSc in Economic Geology from Queen's University and a BSc (Hons) in Geology from the University of British Columbia. Bill has led exploration programs across Canada and in 17 other countries, with experience spanning all phases of mining from grassroots exploration through advanced exploration, mine development, and underground and open-pit production across a wide range of geological environments and commodities, including precious metals, base metals, and industrial minerals.

He has held senior executive roles with junior and intermediate mining companies and has served as a director of multiple public companies listed on the Toronto Stock Exchange and TSX Venture Exchange. He is a founding President of the Association of Professional Geoscientists of Ontario and a past director of Geoscience Canada. He received the PDAC Distinguished Service Award in 2015. He has been involved in several notable projects, including Jacobina in Brazil (acquired by Yamana Gold), Central Sun in Nicaragua (acquired by B2Gold (BTG)), and Hope Brook in Newfoundland (acquired by First Mining), and was a co-discoverer of the Iska Iska silver-tin polymetallic deposit in Bolivia, Eloro Resources' flagship project.

Quinton Hennigh, Crescat's former Geologic and Technical Advisor, has stepped away from his official role within the firm to focus on his duties as Chairman and CEO of San Cristobal Mining. Thanks to Quinton's leadership at SCM, this investment has grown to Crescat's largest and most successful holding across our funds to date. Crescat's funds are also collectively SCM's largest shareholder, so we view this move as a positive and logical evolution that is in the best interest of our investors. We maintain a strong relationship with Quinton and are confident that SCM will benefit from his dedicated focus.

Quinton also continues to serve as a director or advisor to many of Crescat's other portfolio companies. Crescat will continue to engage with him regarding all these companies.

Kevin Smith remains the lead portfolio manager and final decision-maker across Crescat's five funds. Having expert guidance from seasoned industry professionals, like Quinton and Bill, is an important differentiator for Crescat with respect to its activist metals portfolio.

We are excited to welcome Bill to the Crescat team!

Sincerely,

Kevin C. Smith, CFA, Founder & CEO

Nathaniel Gilbert, Analyst

For more information, including how to invest, please contact: Marek Iwahashi, Head of Investor Relations miwahashi@crescat.net (720) 323-2995 Linda Carleu Smith, CPA, Co-Founder & Chief Operating Officer, lsmith@crescat.net (303) 228-7371 © 2026 Crescat Capital LLC Important Disclosures Discussion and details provided are for informational purposes only. This letter is not intended to be, nor should it be construed as, an offer to sell or a solicitation of an offer to buy any security, services of Crescat, or its Funds. The information provided in this letter is not intended as investment advice or recommendation to buy or sell any type of investment, or as an opinion on, or a suggestion of, the merits of any particular investment strategy.This letter may contain certain forward-looking statements, opinions and projections that are based on the assumptions and judgments of Crescat with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Crescat. Because of the significant uncertainties inherent in these assumptions and judgments, you should not place undue reliance on these forward looking statements, nor should you regard the inclusion of these statements as a representation by Crescat that these objectives will be achieved. CPM has not sought or obtained consent from any third party to use any statements or information indicated herein that have been obtained or derived from statements made or published by such third parties. All content posted on CPM's letters including graphics, logos, articles, and other materials, is the property of CPM or others and is protected by copyright and other laws. Performance Performance data represents past performance, and past performance does not guarantee future results. Performance data, including Estimated Performance, is subject to revision following each monthly reconciliation and/or annual audit. Individual performance may be lower or higher than the performance data presented. The currency used to express performance is U.S. dollars. Before January 1, 2003, the results reflect accounts managed at a predecessor firm. Crescat was not responsible for the management of the assets during the period reflected in those predecessor performance results. We have determined the management of these accounts was sufficiently similar and provides relevant performance information. Benchmarks The HFRX Global Hedge Fund Index is designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies, including but not limited to convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage, and relative value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry. The HFRX Equity Hedge Index measures the performance of the hedge fund market. Equity hedge strategies maintain positions both long and short in primarily equity and equity derivative securities. A wide variety of investment processes can be employed to arrive at an investment decision, including both quantitative and fundamental techniques; strategies can be broadly diversified or narrowly focused on specific sectors and can range broadly in terms of levels of net exposure, leverage employed, holding period, concentrations of market capitalizations and valuation ranges of typical portfolios. The HFR Indices are being used under license from HFR Holdings, LLC, which does not approve of or endorse any of the products or the contents discussed in this these materials. The PHLX Gold/Silver Sector Index (XAU) is a capitalization-weighted index composed of companies involved in the gold or silver mining industry. The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 leading companies and covers approximately 80% of available market capitalization. The VanEck Junior Gold Miners ETF (GDXJ®) seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the MVIS® Global Junior Gold Miners Index (MVGDXJTR), which is intended to track the overall performance of small-capitalization companies that are involved primarily in the mining for gold and/or silver. The VanEck Gold Miners ETF (GDX®) seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the MarketVector Global Gold Miners Index (MVGDXTR), which is intended to track the overall performance of companies involved in the gold mining industry. The SPDR® Gold Shares seeks to reflect the performance of the price of gold bullion, less the Trust's expenses. The iShares® Silver Trust (the 'Trust') seeks to reflect generally the performance of the price of silver. Returns for any index include the reinvestment of income and do not include transaction fees, management fees or any other costs. The performance and volatility of the funds will be different than those of the indexes. One cannot invest directly in an index. Benchmarks are unmanaged and provided to represent the investment environment in existence during the time periods shown. Hedge Fund disclosures: Only accredited investors and qualified clients will be admitted as limited partners to a CPM hedge fund. For natural persons, investors must meet SEC requirements including minimum annual income or net worth thresholds. CPM's hedge funds are being offered in reliance on an exemption from the registration requirements of the Securities Act of 1933 and are not required to comply with specific disclosure requirements that apply to registration under the Securities Act. The SEC has not passed upon the merits of or given its approval to CPM's hedge funds, the terms of the offering, or the accuracy or completeness of any offering materials. A registration statement has not been filed for any CPM hedge fund with the SEC. Limited partner interests in the CPM hedge funds are subject to legal restrictions on transfer and resale. Investors should not assume they will be able to resell their securities. Investing in securities involves risk. Investors should be able to bear the loss of their investment. Investments in CPM's hedge funds are not subject to the protections of the Investment Company Act of 1940. Those who are considering an investment in the Funds should carefully review the relevant Fund's offering memorandum and the information concerning CPM. For additional disclosures including important risk disclosures and Crescat's ADV please see our website: Important Disclosures

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。