halbergman/E+ via Getty Images

$200 million is a drop in the bucket for Blackstone (BX) and Prologis (PLD), yet a single $200 million transaction demonstrates a glaring distinction between the behemoths.

One is buying cash flows; the other is creating value.

Blackstone subsidiary Link Logistics bought a portfolio of 8 properties from PLD for $195.9 million. I posit that the specifics of this transaction point to Prologis being a higher return investment than BX industrial funds.

There are various ways in which a buyer can create value through property acquisition. Value creation mechanisms that we have frequently seen in REITs are:

The odd part of this transaction is that none of these value creation mechanisms are present.

Without a value creation component, this transaction tells me that Blackstone is simply willing to accept a lower rate of return than Prologis. In other words, Prologis is willing to sell at the transacted price because they believe they can generate higher returns elsewhere. In contrast, the Blackstone fund appears satisfied with the somewhat low return implied by the transaction price.

Blackstone’s purchase price of $195.9 million is for properties that Prologis bought in 2010 for $58.48 million.

High-quality industrial real estate has indeed appreciated since 2010, but triple the previous purchase price is clearly not discounted.

I think it is entirely plausible that Link Logistics, the Blackstone subsidiary, is a strong operator. They have the capital to hire highly professional asset management teams.

However, the seller is equally or perhaps even more competent. Prologis is the largest industrial real estate owner in the world and broadly respected as a best-in-class operator. Thus, there just isn’t any low-hanging fruit to pick.

Prologis is one of the most cost-efficient operators at both an asset level and a company level.

With 5,882 properties, Prologis has impressive economies of scale. Link Logistics is also quite large, with 3,000 warehouses across over 40 markets. Arguably, both can operate with a highly efficient scale, so property operation cost is a wash.

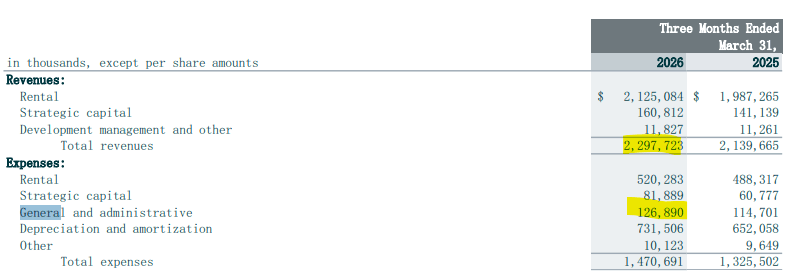

However, I think PLD is likely more efficient at a corporate level. The 1Q26 supplement reveals a G&A expense of just 5.5% of revenue.

PLD

That is difficult to match, especially with the high fees and high compensation that are characteristic of private equity.

This sort of value creation is most common when a big company buys from a mom-and-pop type of seller.

Prologis does not tend to have knowledge gaps, and having operated the assets for 16 years, they know both the submarkets and the properties.

Sale leasebacks are great ways to capture value from the buyer and seller having different businesses. Warehouses previously owned by the tenant can often be purchased at cap rates as much as 200 basis points higher (meaning cheaper) than warehouses already owned by a landlord.

W.P. Carey originates industrial sale-leasebacks at cap rates in the 8s, and they can do so because the operator tenant does not value the real estate in the same way, so the tenant views it as a way of freeing up capital to expand their operating business.

This sort of value creation does not exist in transactions between 2 landlords.

As far as I can tell, there is no value-add in this acquisition. That means the forward IRR is the same for the buyer and the seller. Blackstone is willing to buy at an X% IRR, while Prologis is willing to sell at the same IRR.

Why might PLD have a higher return requirement than a BX fund?

Well, let us look at it from both sides.

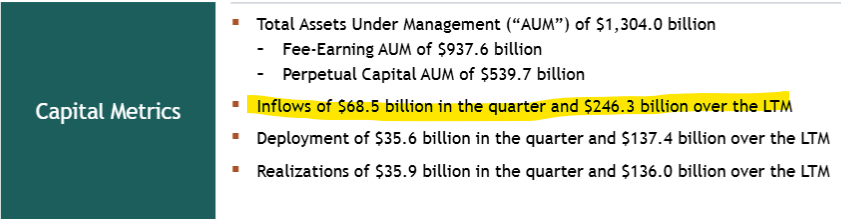

Blackstone is one of the most successful capital raisers in real estate. Per their April presentation, they raised fresh capital of $246.3 billion in the last 12 months.

BX

This impressive ability to raise AUM could potentially make Blackstone itself a good investment, but it does not help the returns of the funds in which people invest. This article is comparing PLD to a Blackstone fund, specifically one focused on industrial real estate.

The way funds work is that they have fees, and they pay investors dividends. Thus, as they raise capital, there is a need to put the money to work right away. If the capital just sits in cash, those fees and dividends will deplete the cash.

So as capital is raised, they need to deploy it into cash-flowing assets rather quickly. With the extreme success of recent capital raising, many BX funds are awash with capital to deploy.

I would argue that the time urgency of deployment does not bode well for discernment as to how it gets invested. They are skilled and can select strong assets such as the Prologis portfolio they bought, but due to the speed at which capital gets deployed, they likely have to take market price. In my opinion, the purchase of the $200 million portfolio from PLD was at full market price. I suspect it will generate a positive return, but nothing special.

Prologis is a value creator. They don’t buy assets just to get money deployed.

Industrial real estate is considered strong right now, which results in industrial cap rates being fairly low. Most stabilized institutional-grade transactions go at cap rates around 5%-6%, give or take a percentage point for submarket and/or growth prospects.

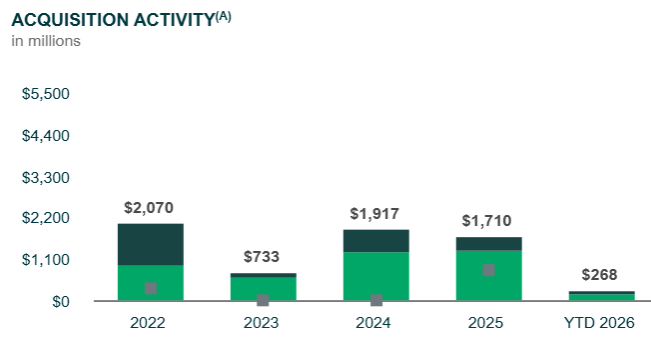

As a result, PLD has significantly pulled back on acquisitions of stabilized assets.

PLD

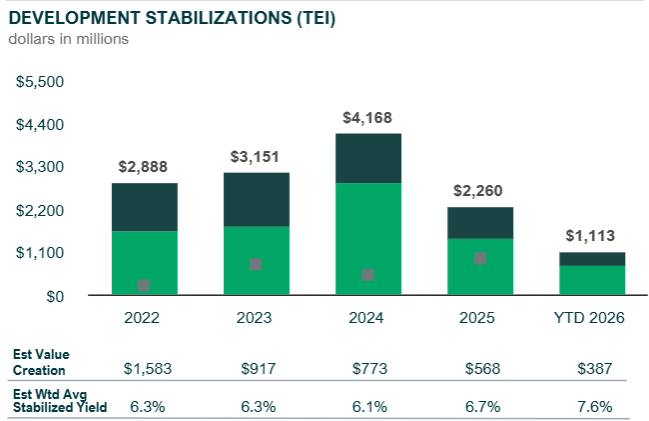

Instead, they have opted to create value through development, which facilitates a much higher cap rate. YTD developments for PLD total $1.1B at an estimated cap rate of 7.6%

PLD

PLD estimates YTD developments created $387 of value based on the difference between the price at which PLD could build and the price at which these assets would transact in today’s market.

I don’t like to just take a company’s word for it when they say they create value, but in this case, I think it can be demonstrated.

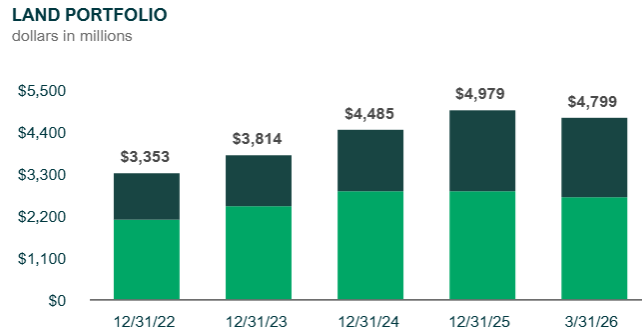

Prologis has a large bank of land that they have been holding for a long time. As of the start of 2026, it was worth roughly $5 billion.

PLD

As demand rises in specific submarkets, they put that land to work with development, often with a tenant already lined up.

There are multiple levers of value creation here:

PLD does not deploy capital at a pace dictated by how successful the latest round of AUM raising was.

It deploys capital patiently and opportunistically.

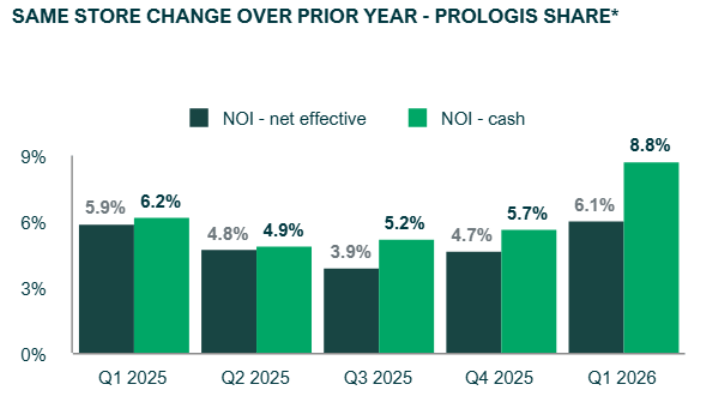

After a few years of heavy supply, the industrial sector outlook has improved. Market rental rates have started to tick back up, as Prologis CFO Tim Arndt noted on the earnings call:

An uptick in market rents this quarter, the first increase in 2.5 years

He went on to discuss how supply was looking more subdued going forward:

The U.S. vacancy rate was flat sequentially at 7.5%, aided by lower completion levels as the construction pipeline remains favorable at just 1.7% of stock compared to a 10-year average of 2.6%.

Data centers seem to be a massive new source of demand for industrial real estate.

Reid Dunbar, East Group Properties President, noted:

Of our 685,000 square feet of development leasing that we've done year-to-date, about half of that was related to data center-related type users.

Incremental demand combined with moderating supply is resulting in accelerating growth in what was already a higher-growth real estate sector. We noted that a majority of industrial REITs had strong first-quarter reports with guidance raises.

Prologis saw same-store net effective NOI growth improve to 6.1%.

PLD

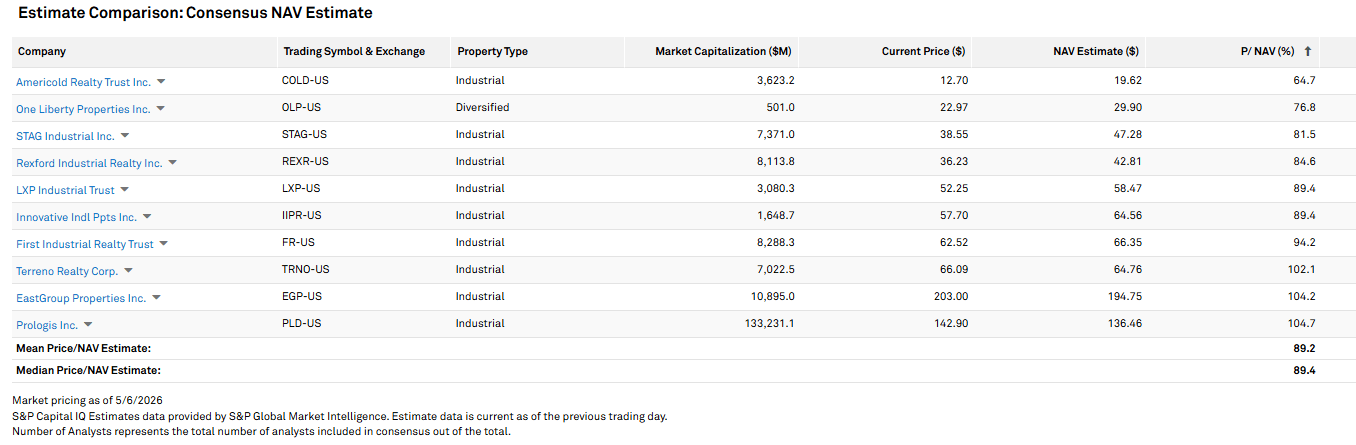

Despite the strength, most of the industrial REIT sector still trades at discounts to NAV. The median industrial REIT is at 89% of NAV.

S&P Global Market Intelligence

Only those of supreme quality like EGP and PLD trade at slight premiums to NAV.

Industrial REITs remain a strong sector in which to invest. I would strongly lean toward owning high-quality public operators over private equity.

In a low cap rate environment, there is a massive difference between those who buy to deploy capital and those who create value.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。