Ildo Frazao/iStock via Getty Images

The Schwab Fundamental International Equity ETF (FNDF) is a $24B-sized (in terms of AUM) ETF that was launched by Charles Schwab Investment Management in August 2013. This ETF, which is priced at an expense ratio of 0.25%, makes distributions on a semi-annual basis (with the yield annualizing to less than 3% at the current ETF price).

For the uninitiated, FNDF's goal is to serve as an enabler of large developed market stocks from outside the US (approximately 900 stocks) by following contrarian investing and disciplined rebalancing, and it does so by tracking an index (maintained by a third party called RAFI Indices that specializes in factor-based indices) called the RAFI Fundamental High Liquidity Developed ex US Large Index. FNDF's tracking index is a subset of a broader index called the RAFI Global Equity Investable Universe (RGEIU) that serves as the base universe.

Unlike market-cap-weighted indexes, which typically dominate the marketplace, FNDF's tracking index selects and weights its holdings on the basis of a fundamental score, which takes into account metrics such as adjusted sales, retained operating cash flow, dividends, and buybacks. Once all the stocks from RGEIU have been allocated an aggregate fundamental score, the top 87.5% (in terms of the cumulative fundamental score) are chosen to make it to FNDF's tracking index. Weighting is also carried out on the basis of the fundamental score, which means stocks with high sales, operating cash flow, and shareholder returns will garner higher weights.

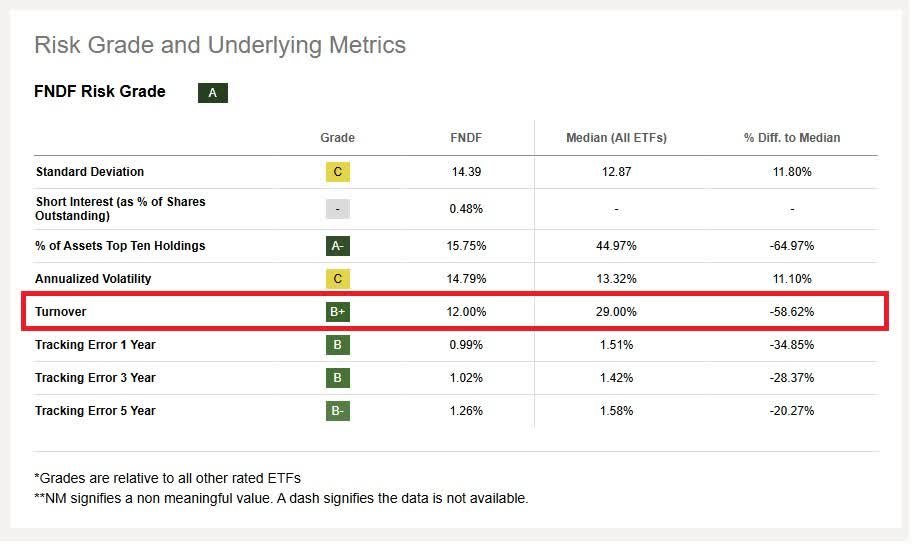

FNDF's tracking index also employs a rather unique "partial" quarterly rebalancing policy, whereby the index is initially split into four equal segments, and only one of these segments is rebalanced per quarter (the shift to the second segment takes place in the following quarter, and so on). This way the transaction costs associated with rebalancing can be spread out. It's worth noting that FNDF's annual churn levels are rather low at just 12% (not even half of what a standard ETF is subject to).

Seeking Alpha

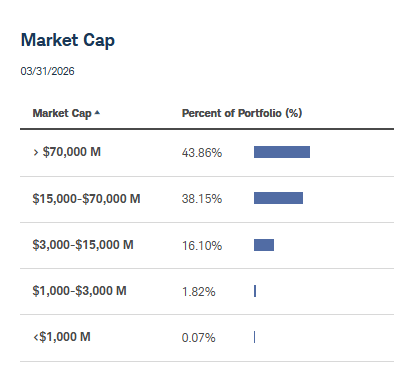

FNDF may track an index that isn't market-cap weighted, but also note that its base universe is still only "large-cap" developed market stocks (rather than an all-cap universe), which still makes this a large-cap-heavy product. Also, weighting takes place on the "quantum" of fundamental metrics such as sales, operating cash flow, etc., which would inevitably capture larger stocks in the screening process. To elaborate, note that giant and large caps account for 84% of the entire portfolio, with the rest largely consisting of mid-caps.

FNDF

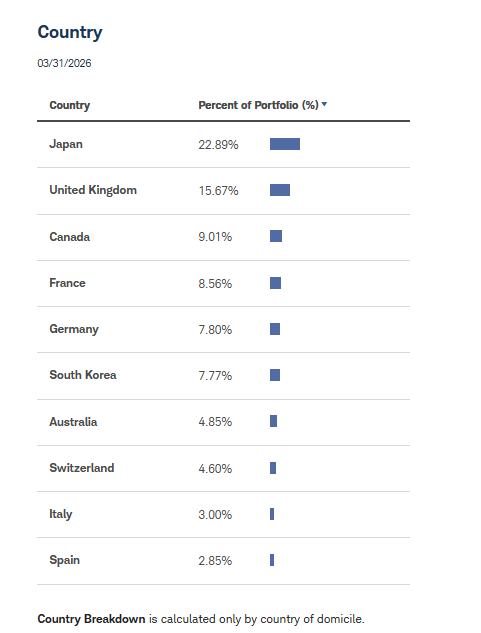

From a geographic angle, FNDF provides exposure to stocks from at least 10 different developed markets, with stocks from Japan and the UK enjoying double-digit weights in aggregate.

FNDF

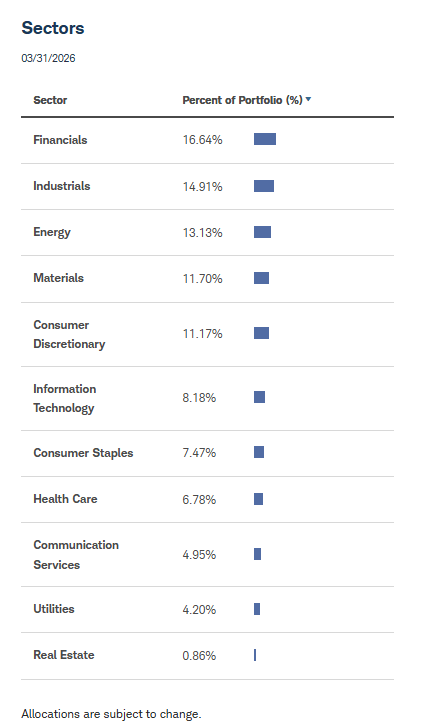

From a sector angle, FNDF dabbles with stocks from 11 different market segments, with the financial sector accounting for the largest stake at 17%.

FNDF

Morningstar

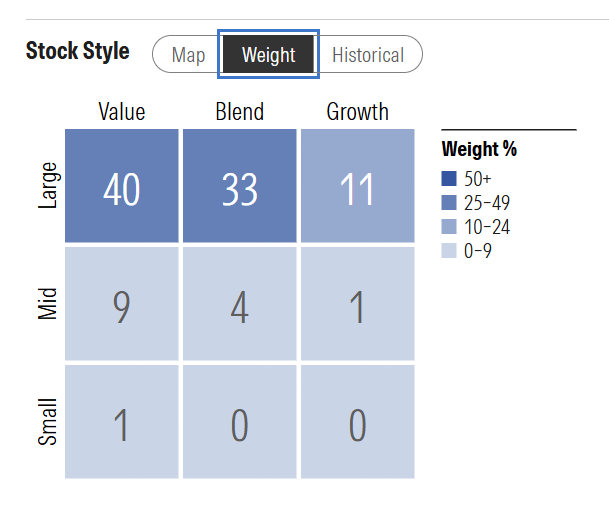

Stylistically, FNDF tilts mainly (50%) to value-type stocks (stocks with features such as low valuation multiples, high dividend payouts, and low growth potential), although a healthy hybrid component also helps (37% of the portfolio).

FNDF is an unhedged ETF, and since it holds stocks of international companies, most of which are denominated in the euro, the JPY, and the GBP, this product's returns could be adversely impacted if those currencies depreciate against the USD, even if those stocks don't move in local currency terms.

FNDF's top four sectors (financials, industrials, energy, and materials, which account for almost 60% of the portfolio) are all old-world sectors that are quite susceptible to cyclical swings, which may make it challenging for FNDF to flourish in an economic down cycle that afflicts developed markets.

Given the emphasis on low valuations, FDNF may end up being a value trap for investors; since FNDF's fundamental scores are driven by the quantum of cash flow, sales, etc., we could have a scenario where those historical metrics are elevated, but the market cap of those stocks is contracting due to other reasons.

FNDF will appeal to those who want exposure to portfolios with well-established foreign developed market stocks, where the emphasis is not so much on the market-cap quotient (as is the case with most developed market ETFs) but rather on the fundamental strength and quality of the holdings.

Since FNDF's weighting is not market-cap weighted, investors aren't also getting tied up with stocks that have typically seen strong price appreciation and, as a result, appear to be overvalued. Also, quarterly rebalancing takes place on fundamental scores, which means those that have run up and look overvalued will be trimmed in favor of undervalued stocks. All in all, the takeaway here is that FNDF would also be suitable for value-conscious investors. As things stand, it's worth noting that FNDF's holdings are only priced at less than 12x earnings and less than 1.5x book. In contrast, the oldest and the largest (as of May 2026) developed market ETF—the Vanguard Developed Market ETF (VEA)—is priced at steeper multiples of 14x and 1.9x, respectively. Given FNDF's quarterly rebalancing on the basis of fundamental scores, one can expect this valuation discount gap to be present (although it could vary by a few bps) for the foreseeable future.

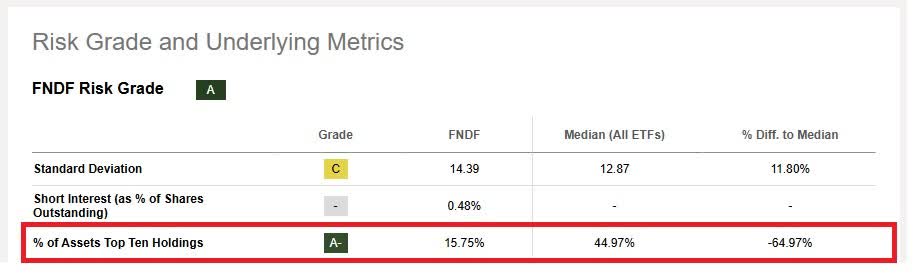

Those who like ETFs that aren't overly concentrated in certain pockets and are not top-heavy will also appreciate FNDF. Note that this product covers stocks from 11 different sectors, and no single sector has an overwhelming weight (there are five different sectors with double-digit weights, whereas most global ETFs will have two or three sectors with double-digit weights, and the rest consisting of single digits). Meanwhile, FNDF's top 10 stocks only account for 16% of the portfolio (the top 10 share for a median ETF is usually closer to 45%).

Seeking Alpha

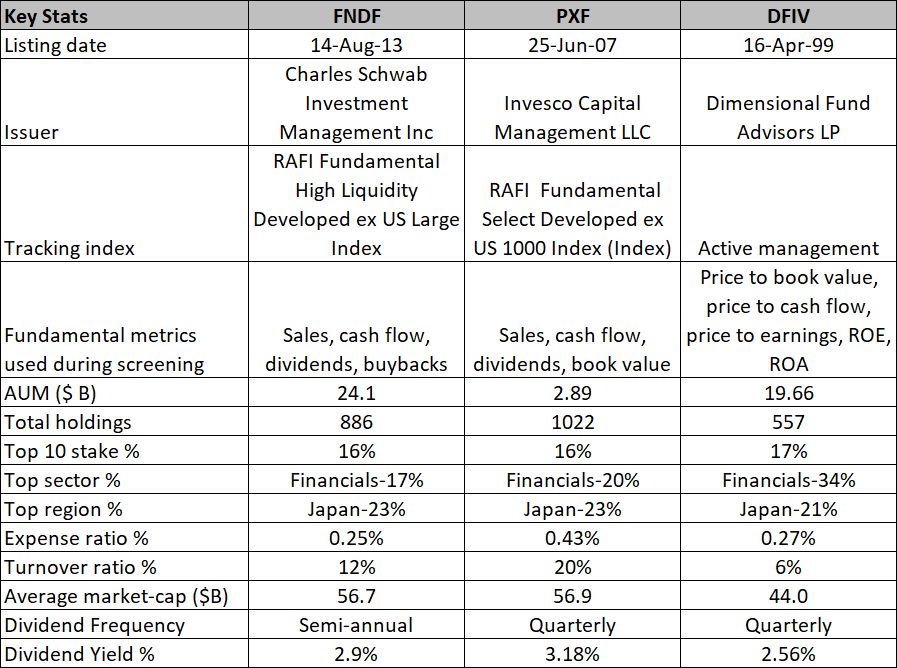

If investors want to consider other ETFs besides FNDF, they can consider other developed market value ETFs that are not built and weighted on the basis of market cap, but rather the fundamental qualities of their constituents will also appreciate another passively managed and another actively managed option. The ETFs we're referring to are the Invesco RAFI Developed Markets ex-U.S. ETF (PXF), which tracks the RAFI Fundamental Select Developed ex US 1000 Index, and the Dimension International Value ETF (DFIV), which is an actively managed ETF.

DFIV, which has been around since April 1999 and is managed by Dimensional Fund Advisors, has quite a competitive expense ratio (only 2 bps pricier than FNDF and much cheaper than PXF) for an actively managed fund. Curiously, it isn't prone to ample churn either, with a turnover ratio of just 6%! While picking its constituents (a much narrower portfolio of around 550 stocks relative to FNDF and PXF), DFIV uses metrics such as price to book value, price to cash flow, price to earnings, ROE, and ROA. Investors who want deeper exposure to developed market financial stocks will also like FNDF.

PXF, which isn't as high profile as the other two (AUM of less than $3B, whereas the other two are closer to $20B), is the priciest from an expense ratio angle but also offers the most lucrative yield (it also makes more frequent distributions than our ETF in focus). While it uses almost the same fundamental metrics, such as FNDF, in building its portfolio, the one major difference is PXF's usage of book value rather than buybacks (which FNDF employs). If you want a much wider reach, PXF is the go-to option, as it covers over 1020 stocks.

Seeking Alpha, Morningstar, ETF prospectuses

FNDF focuses on fundamentally strong developed market stocks from outside the US and is meant for value-conscious investors who want to avoid market-cap weighted ETFs. FNDF, which is well-diversified across sectors and doesn't suffer from concentration risks, may also be prone to getting involved with value traps.

This article answers three main questions about FNDF:

Editor's note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。