Luis Alvarez/DigitalVision via Getty Images

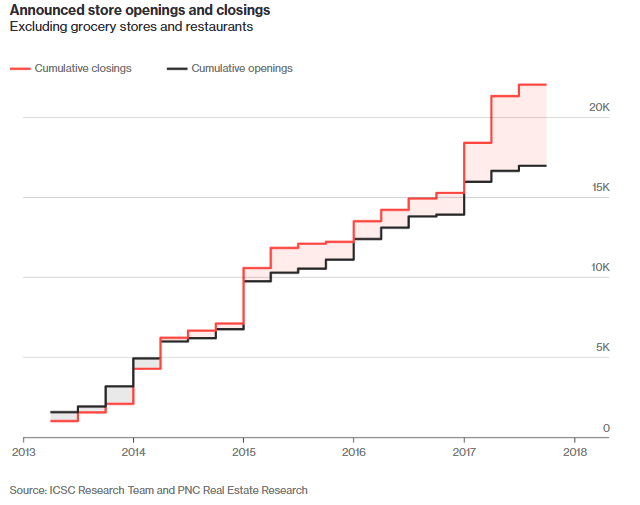

Around 2014, the E-commerce boom had taken hold, and retail store closings started to outpace store openings. It was an era known as the retail apocalypse.

Bloomberg

Source: Bloomberg

Each year, E-commerce took a larger and larger share of retail sales. It threatened to be the end of brick-and-mortar retail.

As investors contemplated the doom of one of the largest REIT sectors, they uncovered statistics about how the U.S. had vastly more retail square footage per capita than the rest of the world.

The thesis was simple: We had too many stores, and they couldn’t compete with Amazon and its equivalents.

There was a good bit of truth to the narrative, and retail REITs did indeed struggle for much of that era. However, the landscape in 2026 looks vastly different.

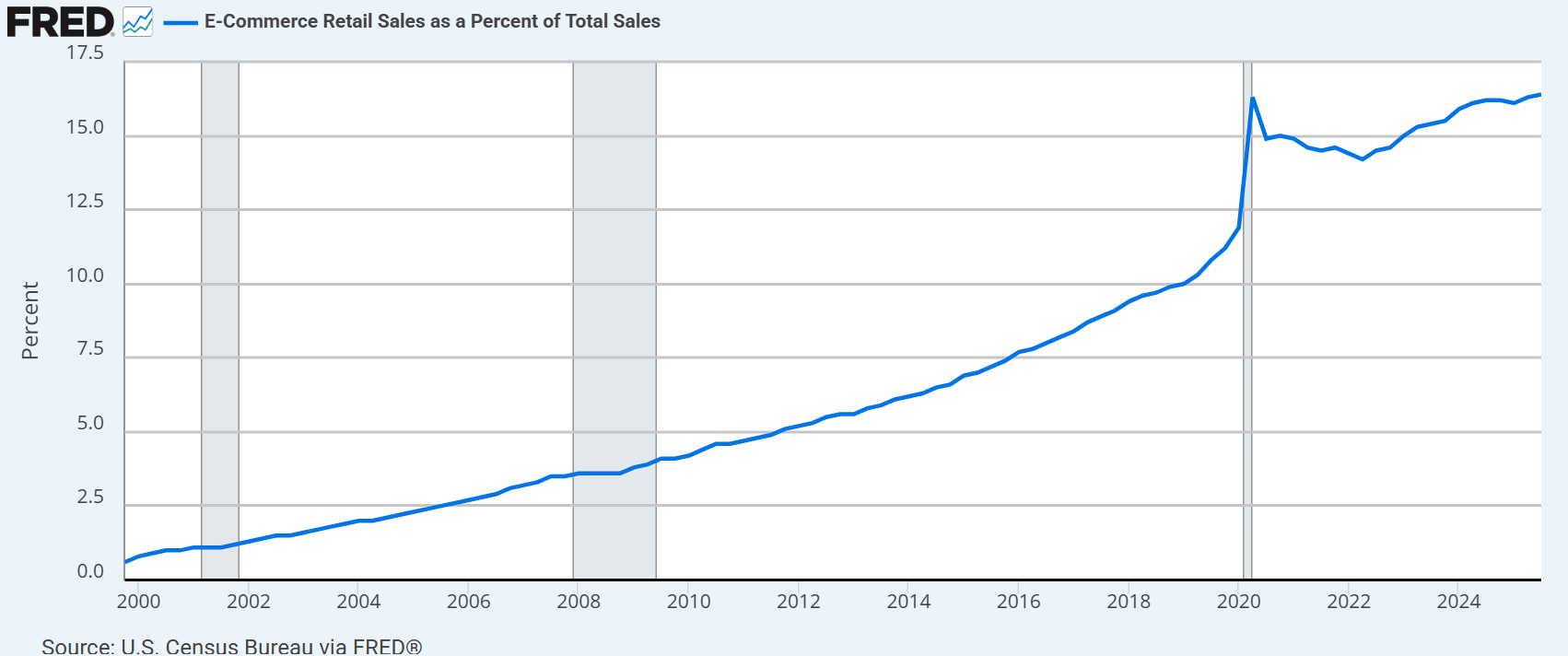

The Federal Reserve Economic Database tracks E-commerce as a percentage of retail sales. It had been rising at a fast pace from just over 0% in 2000 to 16% in 2020. The sharp spike upward in 2020 was clearly pandemic-related, as physical stores were mostly closed, forcing people to do most of their shopping online.

FRED

It left an open question, however, about whether it had changed people’s shopping habits forever.

In theory, the forced use of online ordering would remove the friction of those who were previously hesitant to use E-commerce. Once it became a habit, maybe customers would not return to stores.

After stores reopened, E-commerce market share dropped back down, but it did indeed remain well above the prepandemic level. In 3Q2025, E-commerce market share finally reclaimed the 2020 peak at 16.4%.

The slope, however, is greatly diminished. E-commerce market share seems to be plateauing.

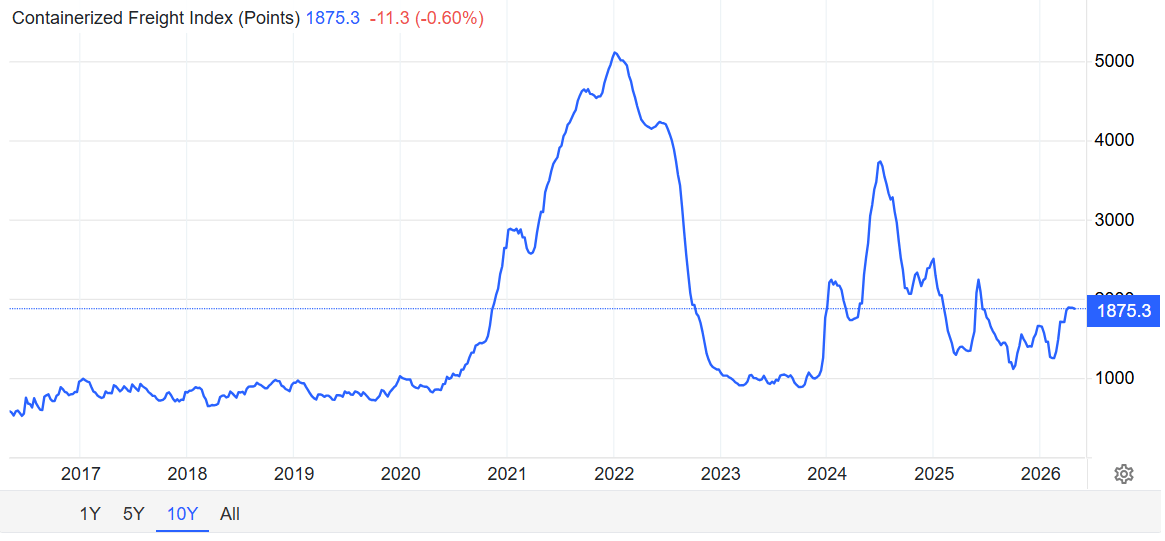

Shipping costs have increased materially. Overseas freight shipping rates are fully double what they were 10 years ago.

TradingEconomics

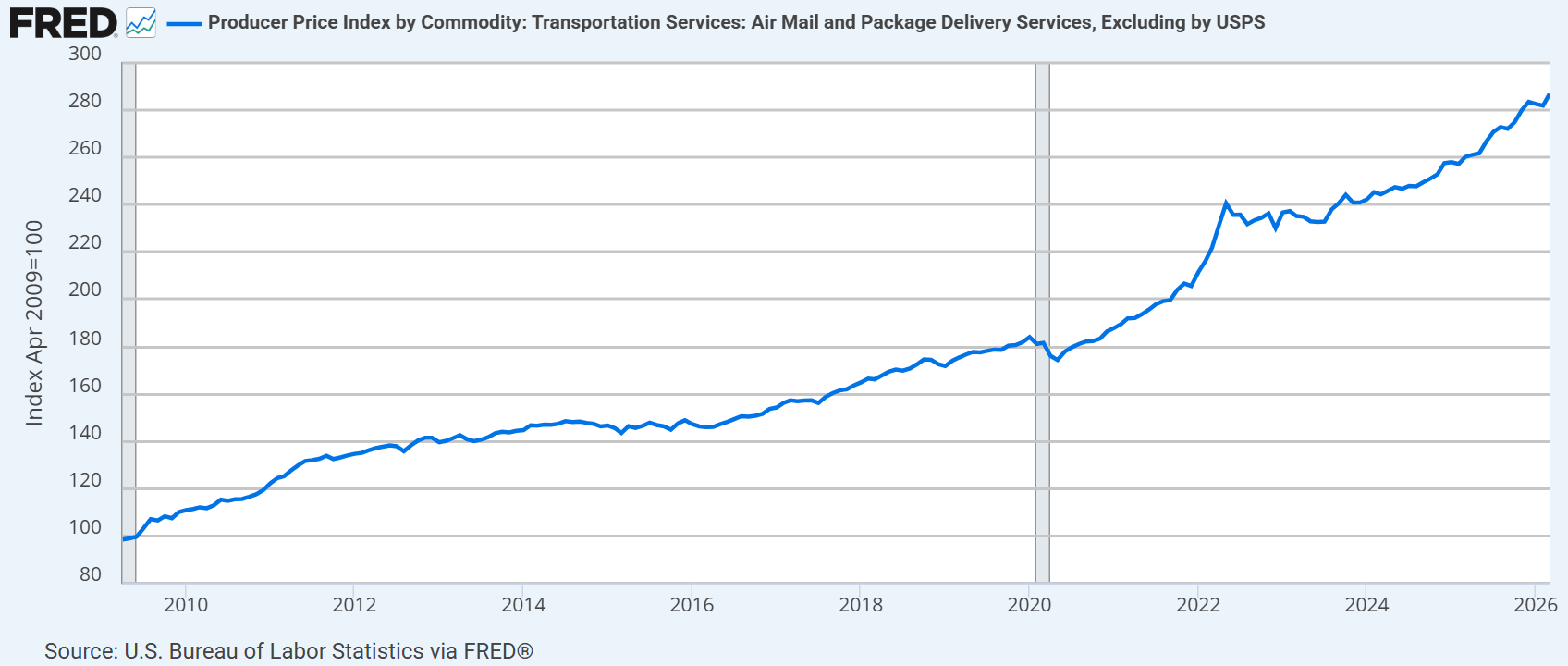

Domestic parcel delivery rates have nearly tripled since 2009.

FRED

In-store retail does still involve some transportation of goods, but significantly less than the individualized delivery of E-commerce. Quite simply, it is more freight efficient to bring a truckload of products from a warehouse to a store than it is to ship individual products to individual consumers.

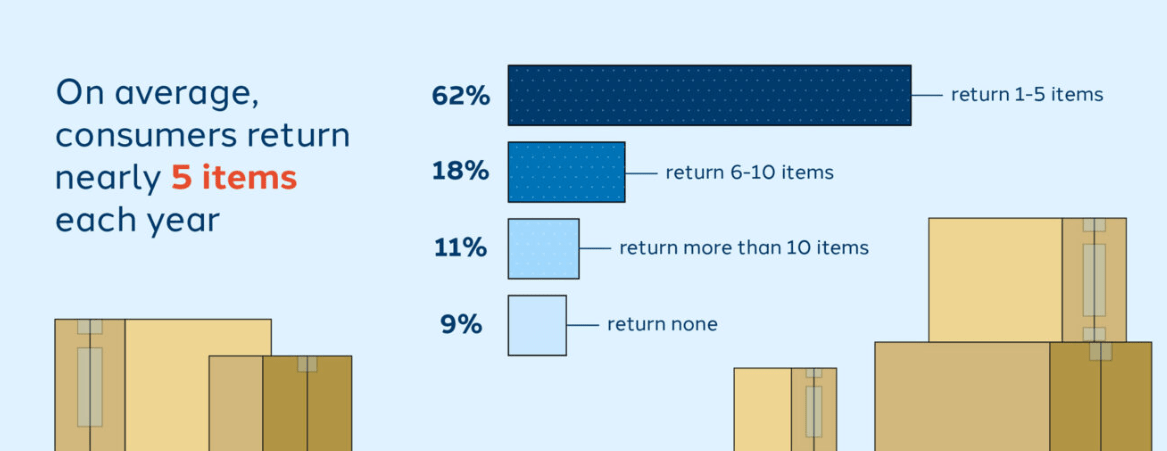

Returns are one of the most challenging aspects of E-commerce. Return rates are inevitably higher for E-commerce for 3 reasons:

91% of consumers utilize returns.

shorr

Source: shorr

Returns are very expensive for E-commerce. Restocking is expensive, and logistical difficulties sometimes even force discarding the product and writing it off as a loss.

When retailers were battling to establish their online presence, they were often willing to subsidize the costs of E-commerce.

They could do this because they were rewarded with higher stock prices and trading multiples. Those which successfully became online retailers were regarded as survivors that would inherit the earth from brick-and-mortar retailers.

With everyone incentivized to hype their online presence, sales were often categorized as online in nature. There are certain sale categories that are sort of both online and in-store:

As all of this was new, there was leeway as to how these categories were accounted for. Since online sales were traded at higher multiples, retailers were incentivized to categorize these sales as online sales even though they were clearly supported by brick-and-mortar stores. There were even some instances where goods bought online and returned in store were recorded as negative brick-and-mortar sales.

All of this added to the perception that brick-and-mortar retail was failing.

Now that E-commerce platforms are more established, sellers are less willing to subsidize the costs. Customers are now more likely to have to pay shipping, and return policies are getting substantially stricter.

With shipping costs and return costs now more factored into the equation, consumers are realizing that in-store purchase is often the cheaper way to buy. They will still use delivery as a convenience sometimes, but it is no longer more convenient AND cheaper like it was in the era of subsidies.

Retail REITs have pivoted their square footage in favor of services (like haircuts and gyms) and products that people prefer to pick out in person (like grocery).

These categories are intrinsically brick-and-mortar and make up a substantial portion of retail sales.

Whitestone REIT (WSR) was among the more aggressive in tailoring their tenant mix in favor of services and experiential retailers. They successfully created a tenant ecosystem that generates a high amount of foot traffic and one where each store benefits from the surrounding stores. It resulted in extremely valuable real estate that attracted a slew of buyout offers.

REITs like Whitestone will often reject the tenant willing to pay the most rent and instead opt for the tenant that improves the value of their remaining space. So rather than having 3 competing shoe stores in a shopping center, it will be one shoe store, a gym, and a smoothie restaurant. A customer could potentially visit all 3 in a single trip.

Grocery stores are known for paying slightly lower rent per square foot than other tenants. However, they consistently generate an incredible amount of foot traffic. Brixmor (BRX) has had a strategy of focusing on strong grocery anchors. Its anchors signed in 1Q26 pay $15.34 per foot.

BRX

These grocery stores make Brixmor’s in-line small shops quite attractive, allowing them to charge $35.36 per foot on new small shop leases signed in 1Q26.

E-commerce no longer looks like the death of stores.

Given the cost of shipping and the large portion of goods and services that work better in a store, I think there is a cap on how high E-Commerce market share can go. It sits at 16.4% today, and while it will likely continue to climb a bit, I don’t think it can get much over 20%.

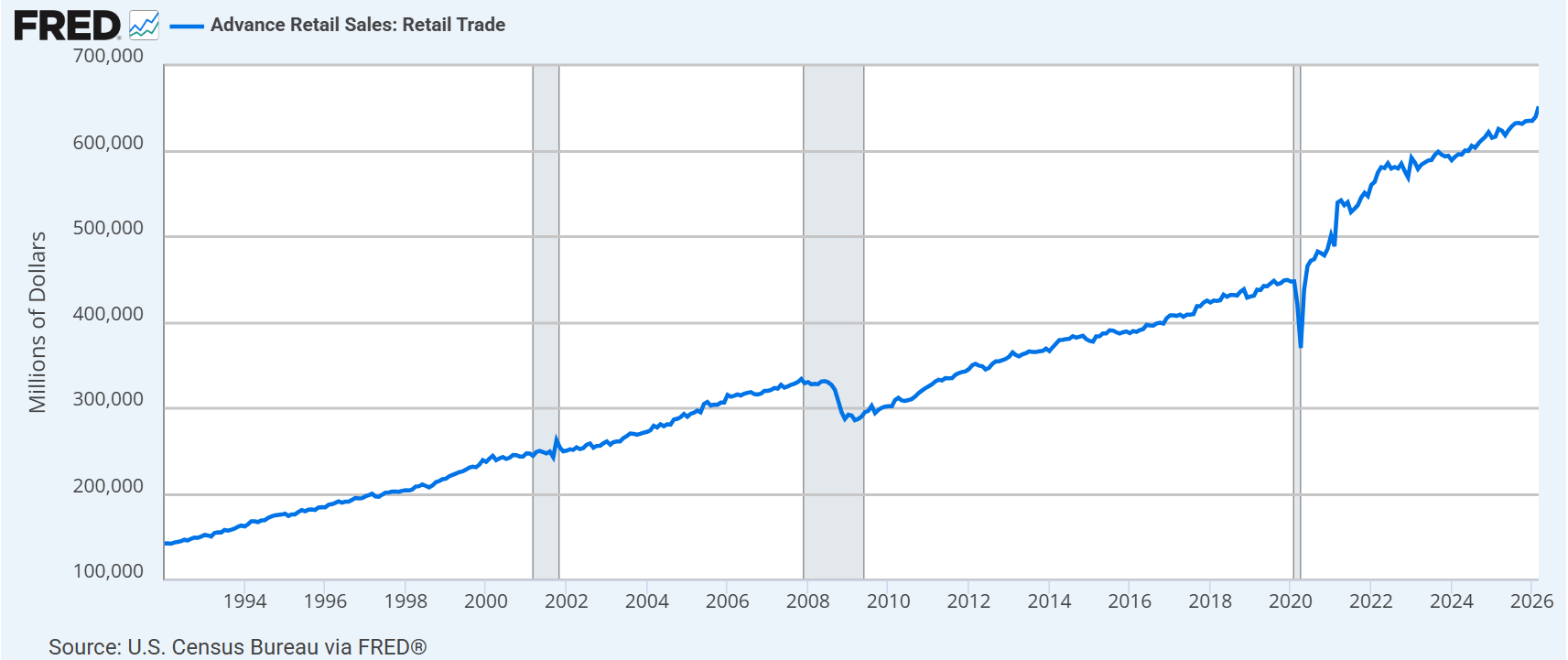

I think the future of retail will be more of a coexistence. Omnichannel is taking over as retailers overwhelmingly opt to have both a physical and digital presence. The split of consumer dollars will remain relatively steady, allowing both online and brick-and-mortar stores to enjoy an increasingly large pie. Retail sales are rising steadily.

FRED

While retail sales are up, there has been minimal new supply of shopping centers. Development is prohibited by the roughly $350+ cost per foot to build a new shopping center not being justified by the current NOI.

Rental rates will have to rise another roughly 30% before significant new supply is unlocked.

This means the increasing retail sales have been accruing to a relatively static square footage, making each existing square foot more valuable. Higher sales per square foot allow landlords to charge higher rent.

Vacancy in the sector sits just over 5%, which is barely more than frictional vacancy. At this level, negotiations are starting to be significantly landlord-favored. The REITs are reporting very strong re-leasing spreads on both new and renewal leases. Here is what has been reported so far in 1Q26 earnings reports.

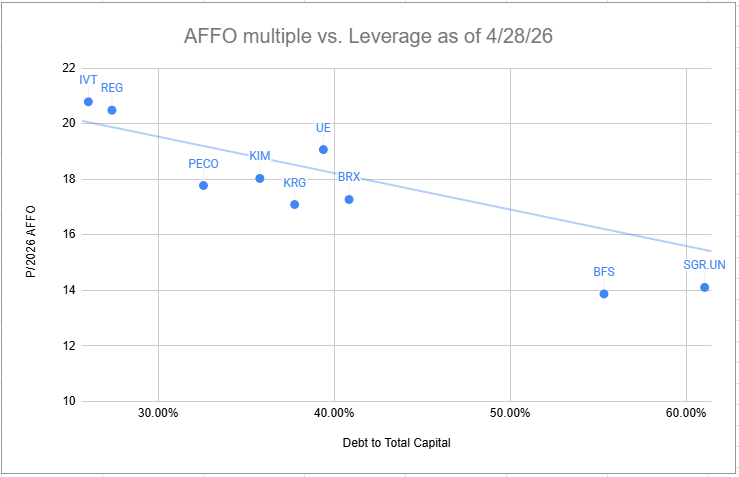

I think shopping centers are fundamentally strong for the foreseeable future. One of the challenges of investing is that the stocks have done quite well recently, which has pulled multiples up considerably. As of 4/28/26, the mean AFFO multiple is 18.1X. At that pricing, they do need to show significant AFFO/share growth to keep going up.

Portfolio Income Solutions

PECO had strong 1Q26 numbers, but I just don’t think they have as much operating expertise as peers. They aren’t taking advantage of the public-to-private pricing arbitrage as well as some peers.

In my opinion, Kimco (KIM) and Brixmor have the best combination of fundamentals and value.

Whitestone also has promising fundamentals, but since it is trading near its take-out price, the remaining opportunity is somewhat limited.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。