tum3123/iStock via Getty Images

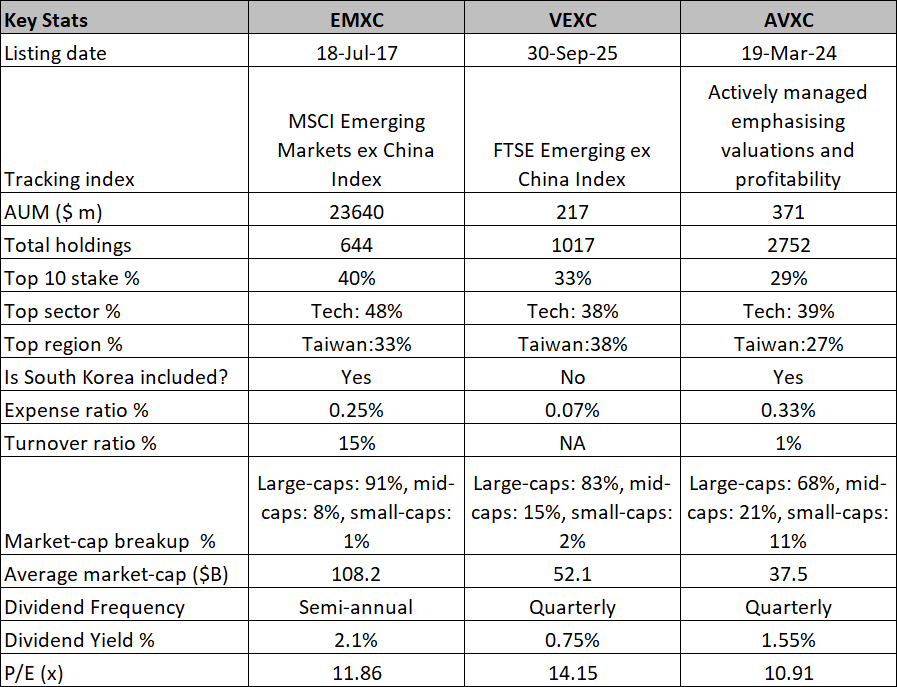

The iShares MSCI Emerging Markets ex China ETF (EMXC), which got listed on the 18th of July 2017, has managed to amass total AUM of $24B during its near-decade existence. EMXC which is issued by Blackrock under its ‘iShares’ stable of ETFs, pays dividends twice a year, which amount to an annualized yield of over 2%. This ETF is priced at a reasonable expense ratio of 0.25%, which is only half the median ETF rate.

EMXC strives to give investors exposure to a wide variety of emerging market stocks (close to 650 stocks) excluding Chinese stocks, and it seeks to go about this by sampling an index called the MSCI Emerging Markets ex China Index [MEMECI]. MEMECI, in turn, focuses on the top 85% of stocks that comprise the free-float market-cap of 23 different emerging markets including Brazil, Chile, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Kuwait, Malaysia, Mexico, Peru, the Philippines, Poland, Qatar, Saudi Arabia, South Africa, South Korea, Taiwan, Thailand, Turkey and the United Arab Emirates.

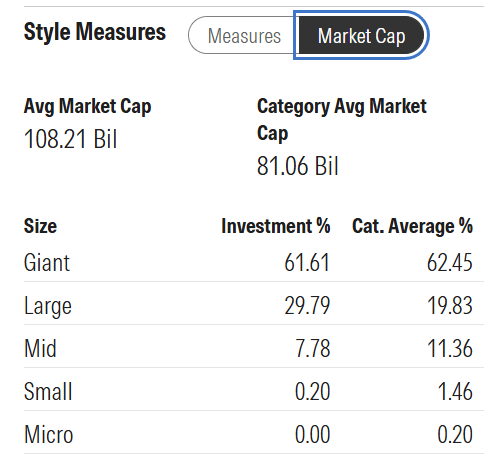

Given that EMXC’s tracking index focuses on only the top 85% of the free-float market-cap of any EM country, it is pretty obvious that small-cap exposure in this portfolio will be very minimal. Meanwhile, Giant-caps account for almost two-thirds of the portfolio, with the average market-cap ($108 billion), only reiterating the giant-cap centric profile of this product.

Morningstar

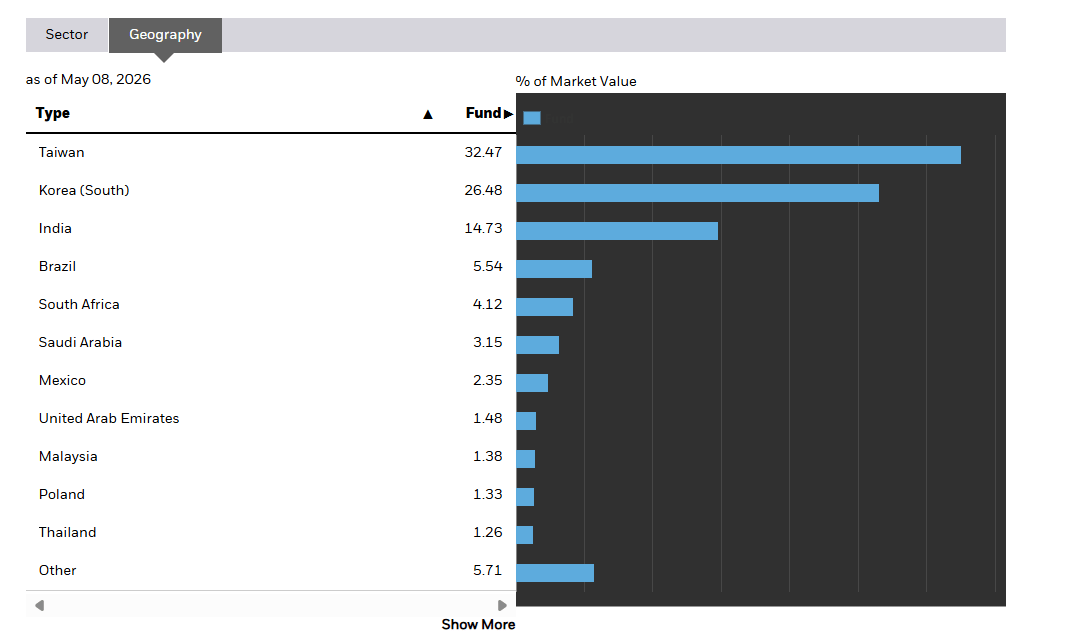

Prima facie, EMXC may attempt to build its portfolio from 23 different emerging markets across the globe, but as things stand, the bulk of the portfolio comes from three key markets in Asia — Taiwan, South Korea, and India, that account for almost three-fourth the portfolio.

EMXC

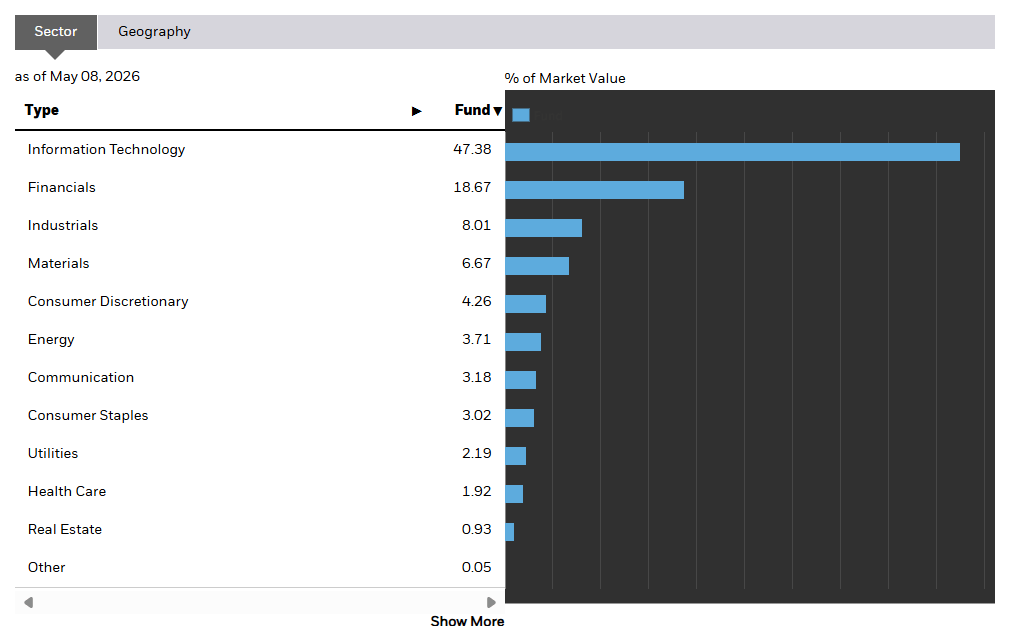

Sectorally, EMXC dabbles with stocks from 11 different options, but one sector in particular- technology stands out, accounting for almost half this portfolio!

EMXC

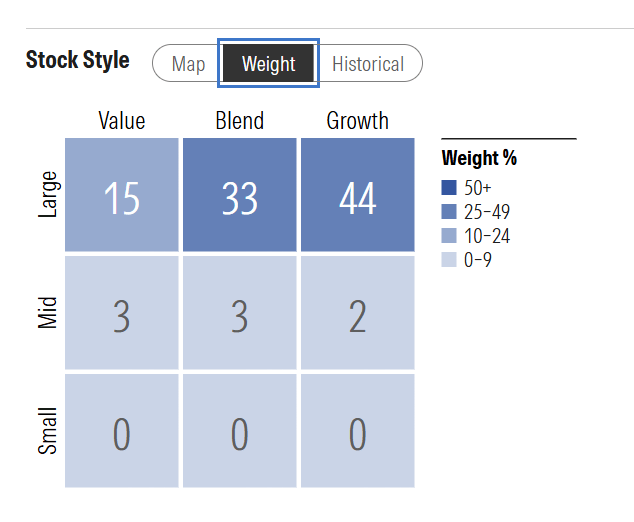

Stylistically as well, this is a portfolio with a strong growth hue (stocks which have strong sales/earnings growth rates, stocks with strong price momentum across months, stocks that don’t make strong payouts to shareholders).

Morningstar

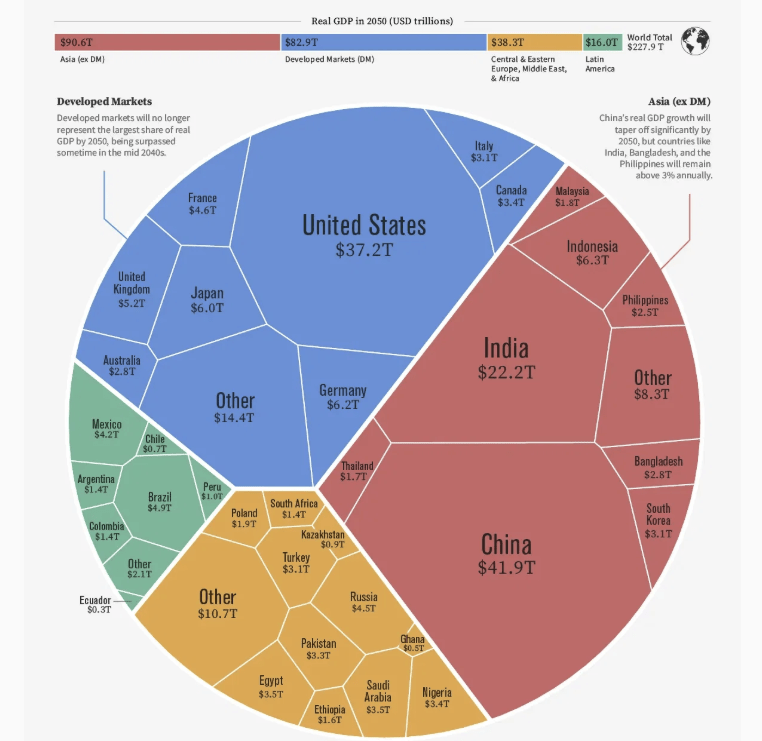

By excluding China, owners of EMXC run the risk of not getting involved with an economy that is still poised to account for a larger share of the global economy (currently at almost 20% of global GDP) and could well become the largest economy in the world by 2050. Of course, this may change over time.

Visual Capitalist

EMXC’s whose NAV is denominated in USD terms, focuses on assets that are denominated in various foreign currencies, particularly the Taiwanese dollar. Thus, even if these assets do well, or even stay relatively flat over a certain period in their local currency terms, but if we have a scenario where the USD appreciates substantially against those currencies, EMXC’s net returns could be negatively impacted.

The prospects of emerging market currencies too are also very susceptible to shifts in global risk sentiment and foreign flows. When risk sentiment in the global markets dip, and foreign investors tend to cash in on their stakes in EM assets, which in turn end up hampering these EM currencies. Investors also need to consider that these EM economies typically also run up relatively high import bills to meet the requirements of an expanding domestic economy, which in turn end up driving large balance of payment deficits that also leave an inimical mark on the currencies.

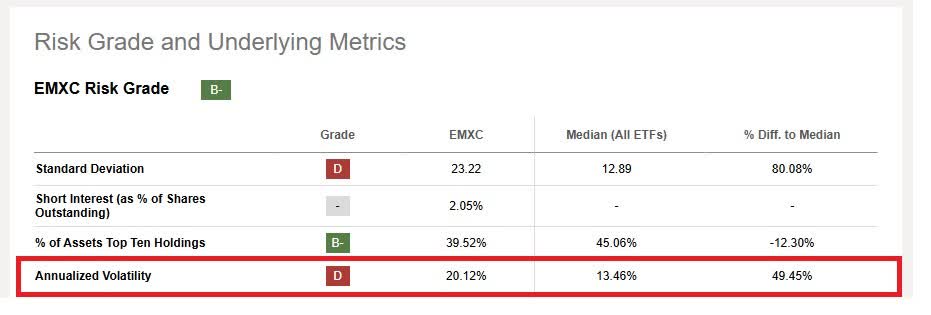

Emerging market equities are not known for being too stable in their movements, and EMXC’s annualized volatility profile of over 20% (which is around 650bps higher than the volatility that a standard ETF is subject to) only reiterates this; in simple terms, this means, an investment in EMXC could be prone to much wide gyrations than what a standard ETF experiences, making it unideal for those who like to see steady and relatively linear progress in their portfolios.

Seeking Alpha

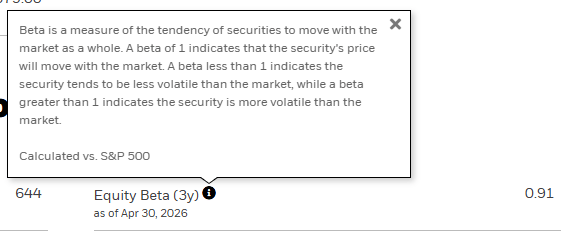

It is also questionable if EMXC, will serve as a good enough global diversifier for portfolios that are centered around US stocks particularly from the S&P500. We say this because over the last 3 years, EMXC’s beta of nearly 1x with the US benchmark suggests that it moves in close tandem with the latter. Put another way, for every 1% move in the S&P500, expect EMXC to move up over 0.9%.

EMXC

One could argue that one of the reasons for this strong linkage is because EMXC like the US markets, is also over-indexed to the technology sector (and is not well diversified amongst other sectors), which has its merits, but is also marked by steep valuations. Sectors characterized by high valuations are also subject to steep sell-offs if the market feels that incumbents in those sectors are not delivering ample bang for buck.

EMXC is meant for investors who want to exploit the alluring growth profile of emerging markets, and their associated equity base, without getting involved with China, which is not only in the midst of seeing historic GDP growth downgrades, but is also increasingly being seen at the center of geopolitical and trade tensions, particularly with the US.

By using EMXC as an EM core in one’s portfolio, investors also have the flexibility of optimizing their Chinese exposure (by pursuing MCHI or other Chinese ETFs in incremental quantities) or keeping it quite limited. By pursuing most standard EM ETFs, this option won’t quite be there, as most of them are heavily exposed to China with exposures ranging from 20-40%.

EMXC’s strong tilt towards the tech sector also means that investors of this product will be well-positioned to profit from the AI wave and other technological revolutions that are likely to germinate in the years and decades ahead.

A lot of emerging market products also avoid pursuing South Korea which is seen as a developed market in certain quarters, but EMXC shuns this trend, and would thus be useful for those EM investors also seeking some Korean exposure.

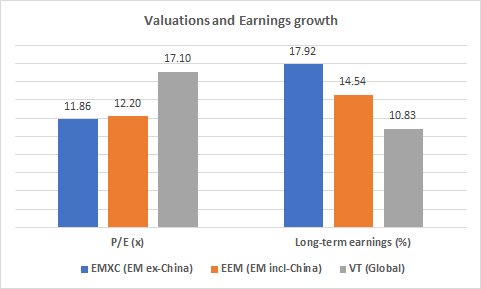

EMXC, also comes across as one of those rare products that will satisfy both value and growth investors. For further context, note that its holdings are currently priced at an earnings multiple of 11.9x (which is a tad cheaper than the iShares MSCI Emerging Markets ETF, the principal EM ETF which also includes Chinese stocks), which translates to a 30% discount over global stocks. However, despite being priced at a cheaper earnings valuation multiple, EMXC’s holdings are still poised to deliver much superior long-term earnings growth of nearly 18%, which is 340bps more than China-included EMs, and over 700bps better than global markets! Again, this is the context at the time of writing and will change over time.

Morningstar

Besides EMXC, investors have quite a few other ETF alternatives that offer non-Chinese EM equity exposure. The two alternatives we’ve suggested here, stand out for different reasons.

The first is the Vanguard Emerging Markets ex-China ETF (VEXC), which may not “yet” be winning any popularity contests (AUM of only $220 million, which is less than 1% of EMXC’s AUM), but which we expect, will become more prominent over time, given its very compelling and best-in-class expense ratio of just 7bps (that doesn’t even equate to a third of what it costs to own EMXC). However, VEXC, which only got listed in September 2025, passively tracks a FTSE-crafted index called the FTSE Emerging ex China Index, and this could be pertinent for those who already have a portfolio with a strong non-US developed market-tilt. We say this because, unlike MSCI (which has created and maintains the index that EMXC tracks), FTSE does not consider South Korean equities to be a part of the EM cohort and rather classifies them as developed market stocks. Thus, owning VEXC could potentially result in some overlap (of South Korean stocks) for those who already have other non-US developed market ETFs in their portfolio.

The second alternative differs from EMXC and VEXC in that it is an actively managed ETF and doesn’t track any index; the ETF in question is the Avantis Emerging Markets ex-China Equity ETF (AVXC) and is managed by a 5-member portfolio management team. AVXC which made its debut in March 2024, and has garnered AUM of $370 million, stands out from the other two as relative weighting of its stocks takes place on the basis of valuations and profitability (basically stocks with cheaper valuations and higher profitability get a superior weight in the portfolio). Note that AVXC’s portfolio is the cheapest out of the lot from a valuation standpoint (less than 11x earnings). Given that it is actively managed, the expense ratio is the priciest out of this lot, but those who want a much wider reach of non-Chinese EM stocks (it also includes Korean stocks unlike VEXC), with a lower top 10 concentration, will also appreciate AVXC as it covers over 4x more stocks than EMXC (with the strongest mid-cap and small-cap exposure of the three products). Ironically despite being actively managed, this is a portfolio that is not prone to a great deal of churn with annual turnover of just 1% (VEXC’s annual churn levels are not available as it is yet to complete a year at the time of writing this article).

Seeking Alpha, Morningstar

EMXC, which covers close to 650 non-Chinese EM stocks, tilts mainly towards technology and Taiwanese stocks, and will likely appeal to both growth chasing and value-conscious investors. However, EMXC’s close linkage with the S&P500 dampen its effectiveness as a global portfolio diversifier.

This article answers these three main questions about EMXC:

Editor's note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。