Getty Images

On Sunday, May 17th, NextEra Energy (NEE) announced its acquisition of Dominion (D). The stocks reacted Monday morning with D up about 9% and NEE down about 5%.

SA

The largest electric utility buying one of its large peers is a big deal in the utility space. The combined company will be unprecedented in size among utilities.

We have owned Dominion for years since our initial D thesis and welcome the merger. While the jump in stock price was nice, the more actionable idea to ponder is how to play it going forward.

This article will discuss the remaining opportunity in D through the merger’s completion as well as factors that could derail the merger.

Per the terms of the merger, it is an all-stock transaction in which each Dominion share will receive 0.8138 shares of NEE. Thus, there is an ongoing arbitrage that widens and contracts with the movement of each company’s share price. We track the arbitrage gap in real-time on Portfolio Income Solutions with our arbitrage tracker tool. As of the time of writing on 5/19/26, each Dominion share converts to $73.36 of value in NEE shares.

Portfolio Income Solutions

Inclusive of the $4.01 of dividends to be received before closing, this implies 13.25% upside remaining in Dominion shares.

As it is a stock-for-stock deal, the upside will also include the delta in NextEra’s price in the interim. While anything can happen to the market price of equities, an average year would be about +7% or ~10% over 18 months.

Assuming normal utility stock behavior, total return for Dominion over the anticipated 18-month close would be roughly +23%.

Since Dominion’s return is now tied to that of NEE, it behooves us to take a look at the merger from NEE’s perspective.

For a merger of its size, there is minimal integration difficulty or risk. The pre-existing Dominion teams will continue to run the utility in Virginia and the Carolinas. The main change to the Dominion operations is that they will now have access to NextEra’s development expertise and lower cost of capital.

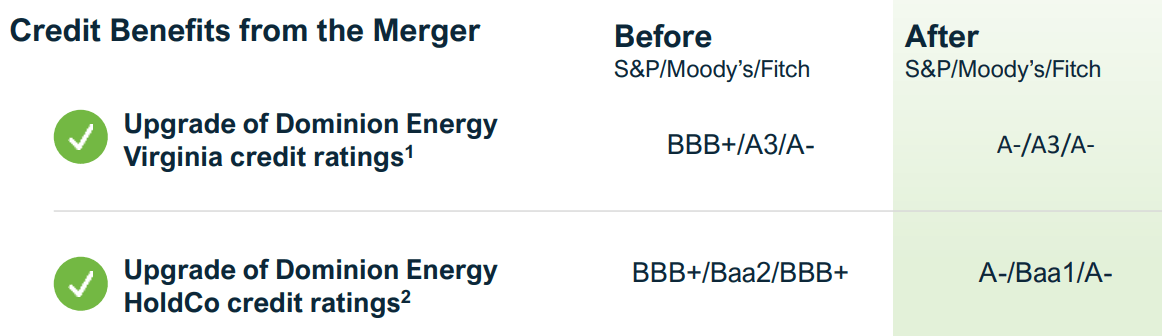

D has good credit at BBB+. NEE has excellent credit at A-. Upon completion of the merger, D will assume the A- credit rating and the cheaper debt capital that comes with it.

NEE

In addition to cheaper debt, NextEra has cheaper equity capital due to consistently trading at a higher multiple.

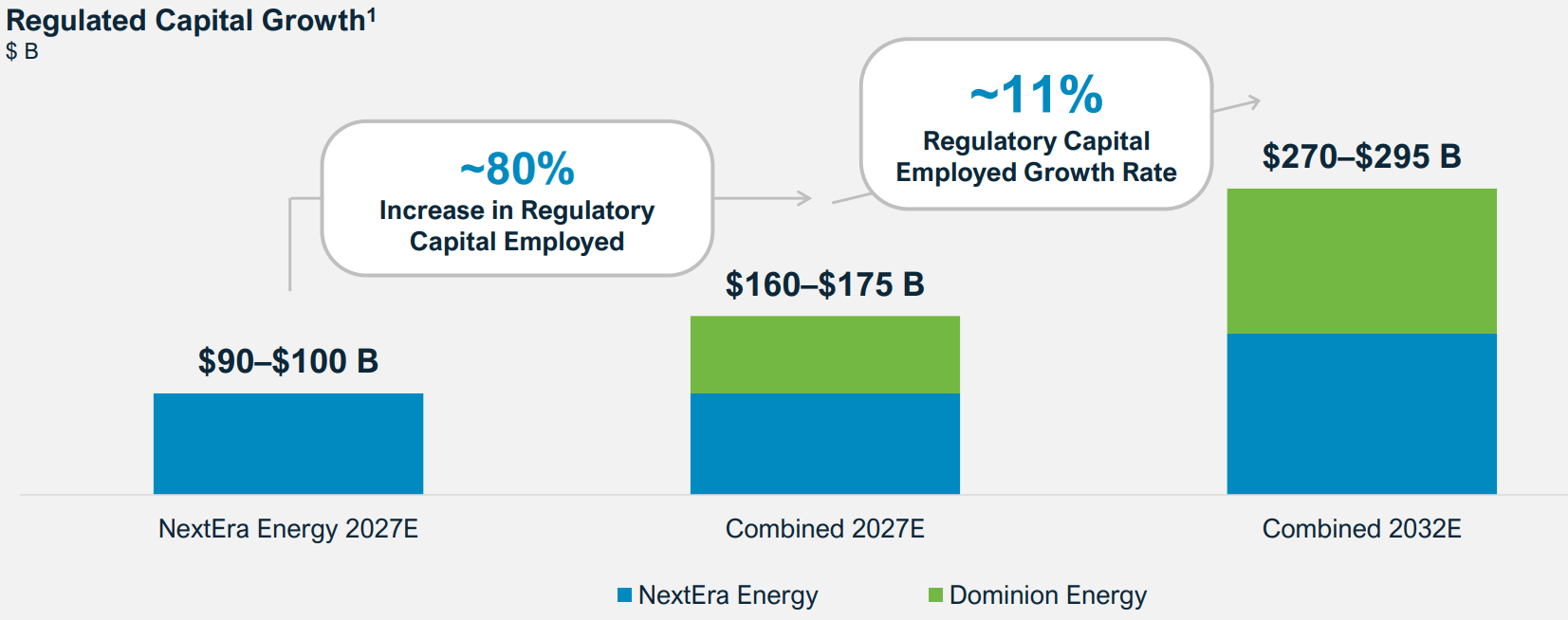

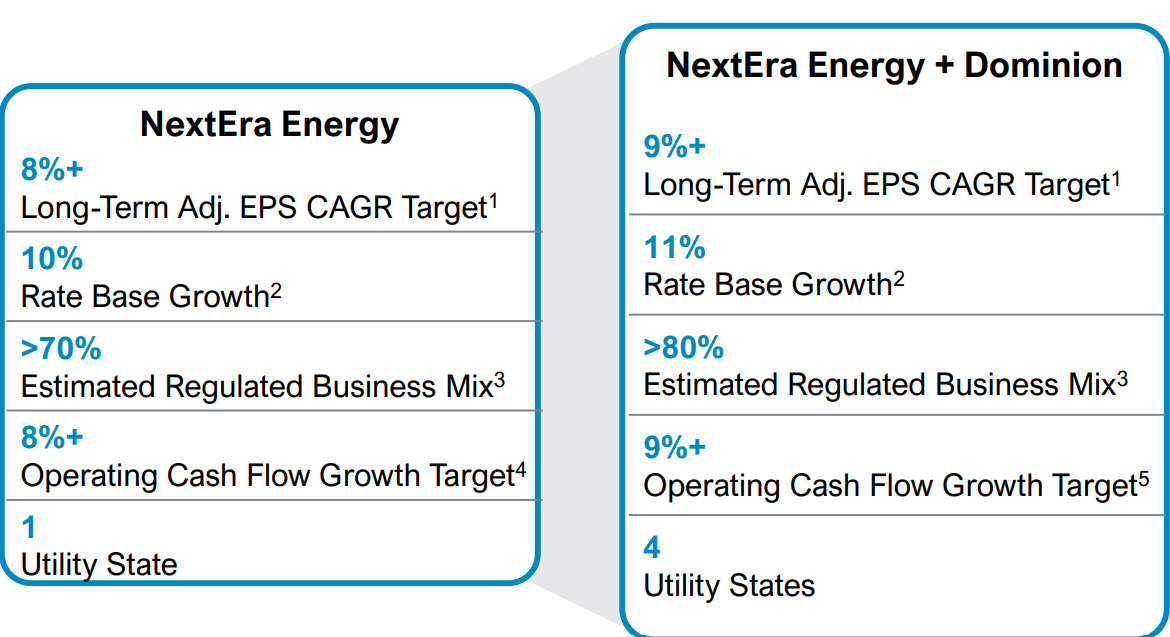

A cheaper cost of capital is a massive advantage in utilities currently because of the size of the pipeline in forward years. By 2032, the regulated capital base is anticipated to grow to $270B-$295B from the 2027 estimated combined $160B-$175B

NEE

That is over $110B in the next 5 years.

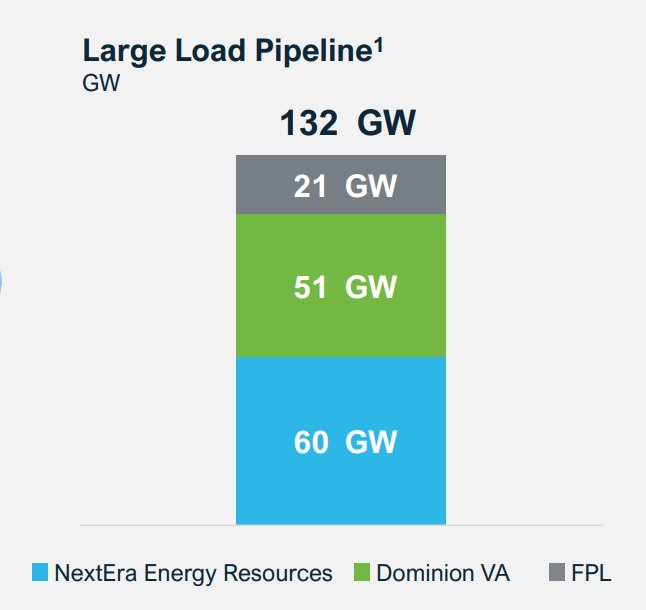

As you know, the buildout of AI data centers is causing a surge in demand for power. The combined entity has a large load pipeline of 132GW.

NEE

Technology matters, but building this out is primarily a capital concern. Having access to large amounts of cheap capital makes this pipeline highly accretive.

Abundance of demand has increased growth rates across the utilities sector. The combined NEE and D leads the pack with a long-term target of 9% EPS CAGR.

NEE

Given the reduced cost of capital in addressing Dominion’s large pipeline in the data center Mecca that is northern Virginia, I think the merger is clearly accretive from a growth standpoint.

It is also immediately accretive.

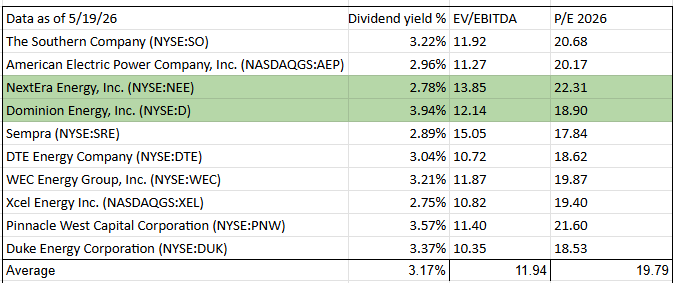

The immediate accretion comes from the delta in multiple at which the stocks trade. NEE consistently trades at a premium to the sector on EV/EBITDA as well as PE multiple. Dominion has consistently traded at a discount.

2MC

The all-stock transaction allows NEE to use its stock as currency to buy D at a significantly lower multiple.

Some of the pre-existing valuation gap shrank in the initial market reaction to the merger as D stock jumped up 9% while NEE stock dropped 5%. However, the conversion ratio was already locked in, so the accretion to NEE will remain.

At current pricing, each share of D would convert to $73.36 worth of NEE, yet D is trading at just $68.32.

I suspect there are 2 reasons for the large gap:

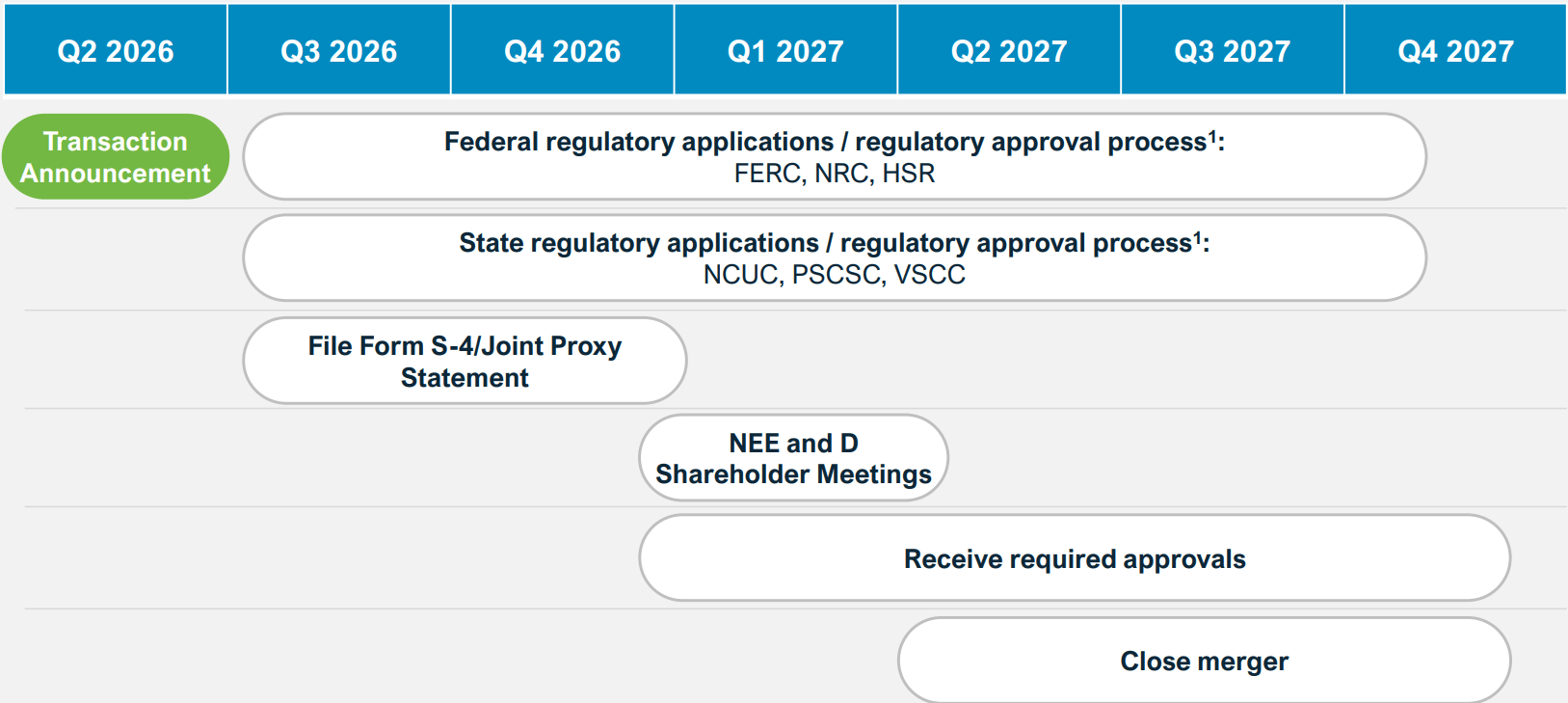

NEE lays out the steps to merger completion below:

NEE

Shareholder approval should be quite easy. Nuclear commission approval should be easy, as both entities are safe operators on their own and should have equal or better capabilities together.

The main hurdles are the federal and state regulators. A recent Wall Street Journal article discusses the hoops through which they will have to jump.

Per the Journal, one of the key concerns of regulators is cost to end consumers and making sure data centers don’t push costs onto regular customers.

While I agree that is a significant concern of regulators, I think that is a concern whether or not the merger happens.

The data center pipeline is just as massive for the independent companies as it is for the combined company. Electricity demand is not related to the merger.

What the merger does impact is how that demand gets addressed. Due to the aforementioned lower cost of capital, it would make sense that the larger combined entity could address the demand slightly more cost-effectively, thereby marginally reducing the cost to end consumers relative to what would happen with the individual entities.

Another potential concern of regulators could be the sheer size of the company. NEE is already the biggest, so absorbing a peer of over $100B in size will create an absolute colossus. In any other industry, combining two of the largest market share companies would trigger antitrust concerns. Having such a large market share can lead to oligopolistic opportunism and higher prices.

It is a bit different with regulated utilities. Each utility already has essentially 100% market share in their coverage region. The prices are already not set by market forces like competition but rather set by the regulators. Thus, customers in Virginia are largely unaffected by the fact that their electricity supplier now also supplies Florida.

NEE has pledged billions of dollars of savings/refunds to end customers as part of the merger. They seem to be willing to do whatever they need to do to assuage regulatory concerns.

My take is that the merger is likely to go through but on a delayed timetable. That said, there is a real chance that the merger will be blocked by regulators.

In the event regulators block the merger, NEE has to pay a large break-up fee to D, per WSJ:

“The deal includes a $4.8 billion termination fee that NextEra would pay if regulators block the deal.”

$4.8B is $5.45 per Dominion share, which is just about as much as D has risen since the merger was announced. I think that would go a long way toward cushioning the blow and reducing the downside to D investors if the merger fails.

As the merger is accretive immediately and to growth rate, I think NEE is worth more now than before the announcement. As such, I think it will swiftly recover the roughly 5% drop since the announcement. This bodes well for the Dominion leg of the merger, as the share prices are largely tied since it is a stock-for-stock deal.

With D being the discounted entity, I think it is a much better way to play the combination than NEE. I think D offers strong total return potential with about 23% upside to closing, assuming normal utility behavior.

While there is a significant chance of the merger being blocked, the very large break-up fee should help mitigate most of the damage to D shares. Therefore, I consider the overall reward-to-risk of D to be quite favorable. At current pricing, I remain bullish and am holding my shares.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。