Getty Images

By Eric Leininger

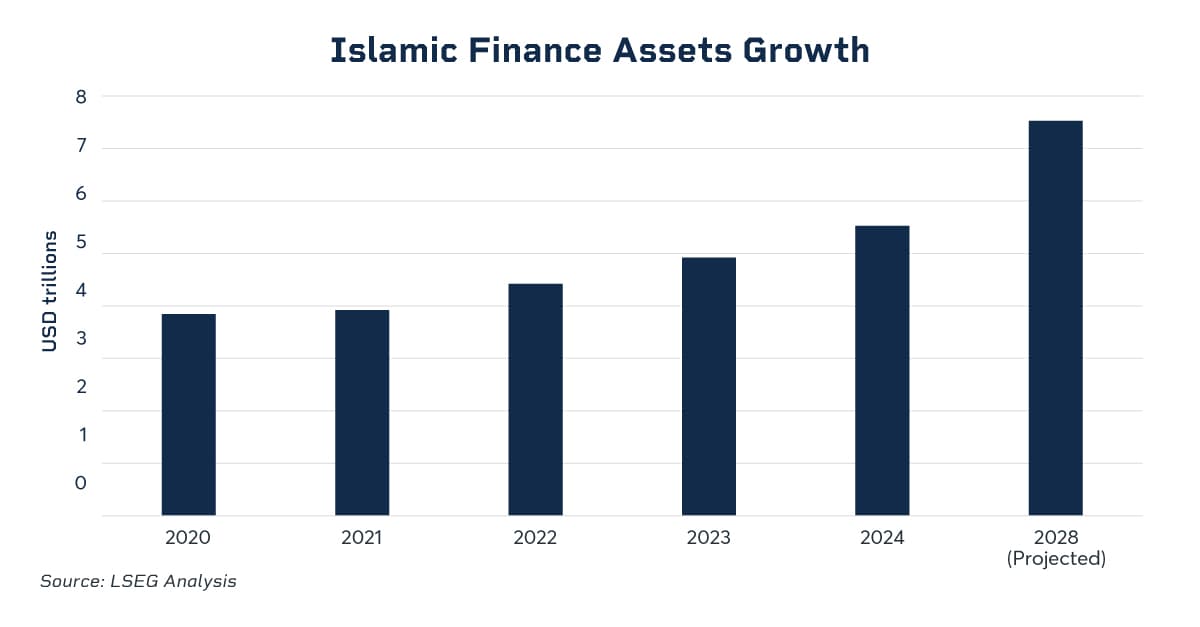

Islamic finance has historically been characterized as a localized, regional subset of the global economy. However, recent data suggest a different trajectory.

Moving through a period of growth, the industry surpassed $5 trillion in total global assets in 2024. Driven by an estimated 14.5% compound annual growth rate, total assets are now projected to reach $7.25 trillion by 2030. This anticipated expansion represents a systemic shift that global investors are starting to factor into their long-term strategies.

At the core of this evolution is a rapidly growing, increasingly affluent global demographic. As the middle class expands across emerging markets, there's a surging grassroots demand for financial systems that strictly align with Sharia principles, which are centered around themes like equity, fairness, transparency, risk-sharing, and ownership/materiality. Islamic finance requires the elimination of excessive uncertainty (Gharar), the avoidance of speculation (Maisir) and the strict avoidance of interest (Riba).

This preference is evident in the growing popularity of structures like Sukuk (Sharia-compliant financial certificates often referred to as “Islamic bonds”), where instead of traditional debt, funding is directed into the creation of physical infrastructure, renewable energy projects, and industrial manufacturing.

These investments result in the acquisition of capital assets that provide measurable utility to the real economy, effectively transforming the traditional debtor-creditor relationship into a partnership-based model.

The macroeconomic impact of a shift like this lies in the potential development of a massive, aggregated pool of Sharia-compliant capital. This capital would likely start to flow upward into wealth management, institutional investing, and sovereign wealth funds, providing the baseline liquidity that drives the industry's broader need for institutional-grade financial architecture.

State-level initiatives have also historically provided Sharia-compliant, macroeconomic support through plans like Saudi Arabia’s Vision 2030, which aims to diversify the country’s economy away from oil among other objectives. However, as we move through 2026, many regional powerhouses are entering a more disciplined phase of capital deployment.

With government debt in key Gulf markets forecast to rise to fund these initiatives – Saudi Arabia's debt alone is projected to approach 40% of GDP next year – sovereign wealth funds are transitioning from an era of expansion to one of strict fiscal oversight and streamlined priorities. For large regional corporations executing multi-billion-dollar financing facilities under these new constraints, securing predictable financing is critical. Cost certainty has become a mandatory tool for accurate cash-flow forecasting and strict alignment with tighter budgets.

Historically, a structural friction existed between Islamic finance markets and Western institutional capital. While international investors recognized the diversification benefits of Islamic instruments like Sukuk, the underlying pricing structures often did not easily translate to conventional risk models.

However, recent data suggests this friction is diminishing. Building on the industry's $5 trillion asset base, global Sukuk issuance reached $264.8 billion in 2025, up from $234.9 billion the previous year. More significantly, foreign currency-denominated issuances have now exceeded the $100 billion mark, nearly doubling their 2021 volume. This growth indicates that non-Islamic international investors are actively buying in, seeking secondary market liquidity and driving down the cost of capital for issuers.

Further accelerating this global adoption is the natural alignment between Islamic finance principles and the mandates of Environmental, Social, and Governance (ESG) investing. Ethical, Sharia-compliant investments are a natural fit for global ESG portfolios, and the market is responding. Total sustainable Sukuk issuance reached $21.5 billion in 2025 – a 38% increase from 2024. By positioning these green instruments alongside globally understood ESG criteria, issuers are able to capture both the traditional Islamic finance buyer and the Western institutional ESG portfolio manager simultaneously.

To support this influx of foreign and sustainable capital, the demand for sophisticated, transparent and robust financial benchmarks has never been higher. This is where forward-looking benchmarks, such as CME Term SOFR, serve as the link between Islamic finance and global capital.

By establishing a known profit rate at the beginning of a corporate or institutional contract – derived from deep, observable transaction data from the underlying futures market – these benchmarks provide the up-front cost certainty required for Sharia-compliant structures, while offering a risk profile that Western institutions already understand and can hedge.

To further facilitate integration into global portfolios, these methodologies operate under strict governance. Administered by the CME Benchmark Administration (CBA) and supervised by the United Kingdom Financial Conduct Authority, the processes operate in full compliance with IOSCO Principles for Financial Benchmarks. Recognized by standards bodies like the International Islamic Financial Market (IIFM) and the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), this provides Islamic institutions with the confidence that their profit rates are calculated using an objective, auditable methodology.

Over the next 12 to 18 months, as sovereign wealth funds and corporate borrowers operate under renewed fiscal discipline, a significant expansion in the global reach of cross-border Sukuk issuances could be ahead. With unified data architectures now allowing global banks to align their conventional and Islamic treasury desks using a single benchmark, the historical barrier to entry for non-Islamic institutional investors has effectively been removed.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。