I am upgrading Solid Power (SLDP) to a buy rating following substantial progress toward commercialization. I think the chance of success (by success I mean a major auto OEM adopting SLDP product in mass production models) has increased from around 20% at the time of my first article to around 80% today.

There is still a non-zero probability that it does not succeed, but I have taken a small position and will look to increase it.

Solid Power is hoping to disrupt the enormous market of lithium-ion batteries in EVs. The market was around $91 billion in 2024 and is forecast to top $200 billion by 2034.

Despite being a small-cap company, the business model, chosen technology, and leadership within that technology have convinced me to invest.

SLDP has adopted a B2B licensing and supply model. The new model ensures it can partner with incumbent manufacturers, helping them stave off threats from potential replacement technologies.

The SLDP electrolyte can be used in existing roll-to-roll manufacturing of battery cells, making the technology highly compatible with existing large-scale manufacturing plants and reducing adoption costs by up to 90% compared to building entirely new production lines.

Revenue Streams: Income is now driven by three pillars:

Electrolyte Sales: Supplying proprietary sulfide-based powder to partners.

Technology Licensing: Allowing OEMs to use SLDP cell designs in their own factories.

Joint Development Agreements (JDAs): Collaborative R&D funded by partners like BMW, SK On, and Samsung SDI.

The core of SLDP’s technology is its sulfide-based solid electrolyte, which replaces the flammable liquid electrolytes found in traditional Lithium-ion batteries.

Safety & Stability: By removing flammable liquids, SLD has improved the safety profile of batteries.

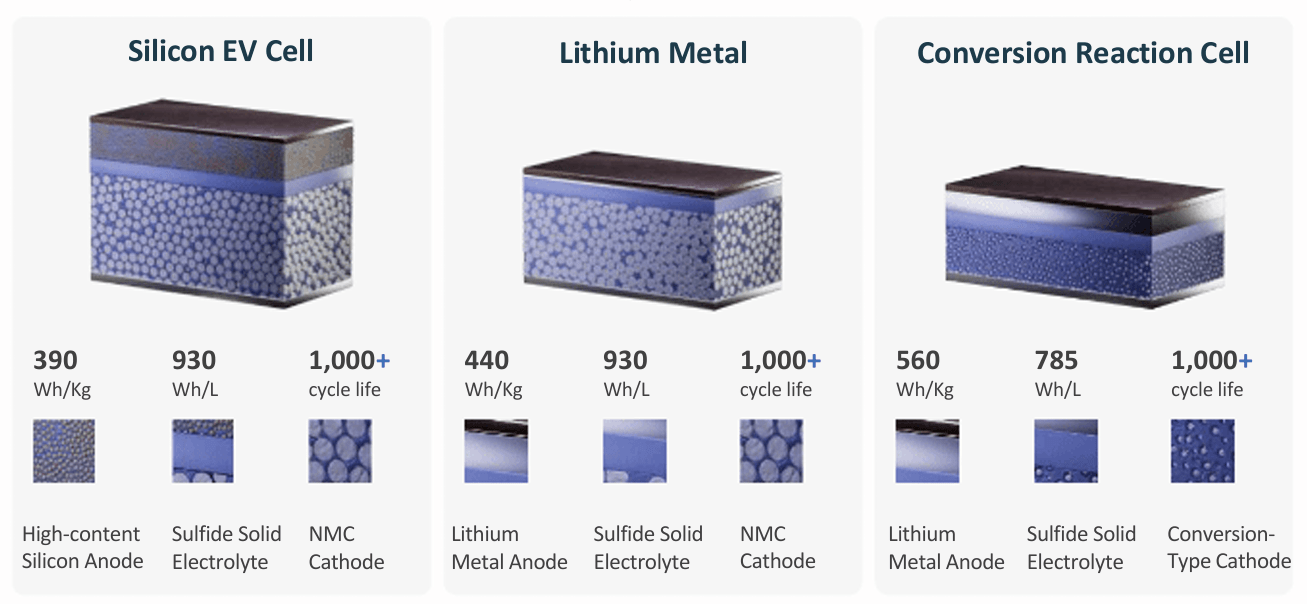

Chemistry Agnostic: SLDP technology supports Lithium Metal Anodes and Silicon Anodes, which could increase EV range by up to 80% at the same battery weight.

Infrastructure Compatibility: Critically, SLDP’s electrolyte is designed for roll-to-roll manufacturing. This means battery makers can upgrade existing lines for ~10% of the cost of building new ones.

Continuous Production: The company is currently moving from "batch" processing (30MT/year) to a continuous manufacturing process expected to hit 75MT/year by the end of 2026.

A large part of my research plan is talking with people in the industry- it is important to understand why people speak with me and assess any axes they may have to grind, but “Shop Floor” information is often invaluable. In this instance, I interviewed a former SLDP engineer who left the company in mid-2025 and now holds a senior management role at a US battery manufacturing company. I don't think he left on good terms, but he has since secured a higher-paying, more senior position. I will use [inv] to indicate information that came from the interview.

Conventional lithium-ion batteries are at their physicochemical limit; it is not possible for them to get substantially better. If we want an EV with a much longer range, then we either need a much bigger battery or a more energy-dense one.

Several scientific research papers suggest that sulfides are the most promising among solid-state electrolyte technologies.

Solid Electrolyte (Data: Reddy 2020, MDPI 2025)

A substantial advantage of solid batteries could be the ability to incorporate lithium and silicon anodes. Silicon anodes are a short-term prospect (Amprius (AMPX) is making real progress, and I am a repeat investor), and lithium anodes are probably more medium-term.

Different Anodes (SLDP Website)

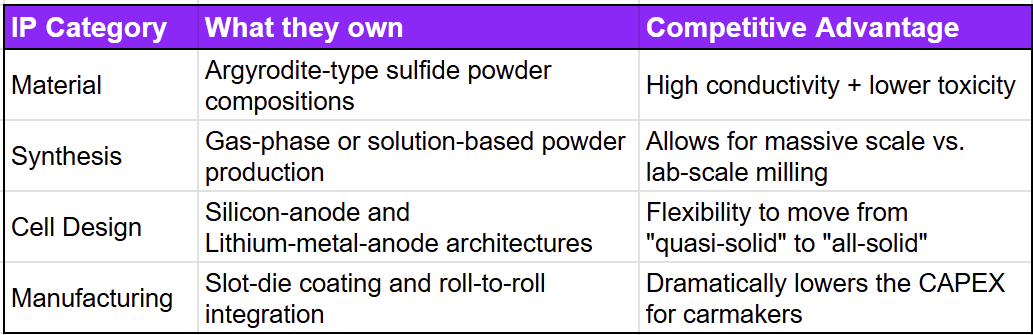

The sulfide product of SLDP is not entirely novel; Toyota has a sulfide electrolyte (though it is unclear whether it is completely solid), and the particular crystal they are using is well known in Academia.

However, SLDP has developed robust patent families surrounding its business.

SLDP Patents (Author)

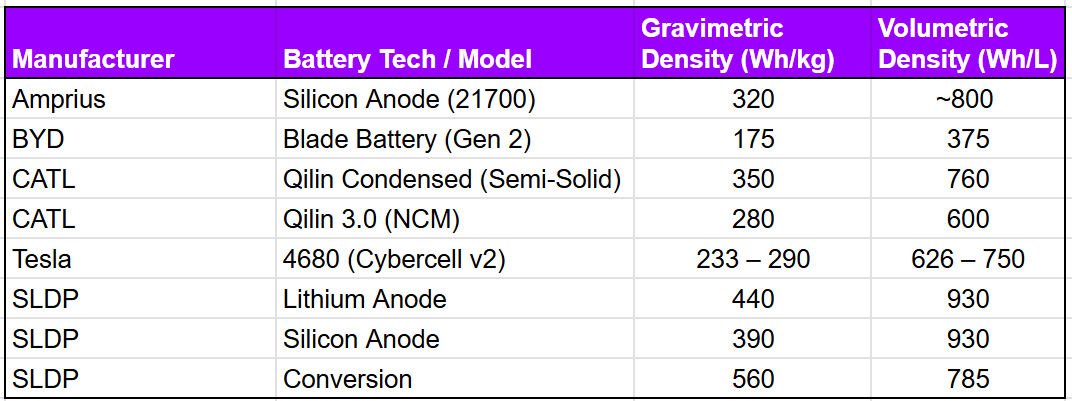

SLDP has two types of competition: batteries already in use and new emerging technologies

Existing batteries are compared below

Battery Comparison (Author)

SLDP would appear to have a significant advantage in energy density, but to enter full-scale production, they must be cost-competitive. The focus for large EV manufacturers seems to be cost rather than range.

Lithium batteries have been coming down in price, but the electrolyte represents only 10% of the bill of materials. The anode, and especially the cathode, made from expensive nickel, manganese, and cobalt, will be the drivers of future cost reductions.

If the cost of Lithium-ion batteries falls significantly, the market for SLDP could be reduced dramatically.

There is a potential that cheaper solid-state battery cathodes could appear. SLDP is working on such a cathode, using a much cheaper material because of the sulfide electrolyte's low electronic resistance. [inv]

SLDP is working hard to source all of the precursors they need to reduce cost, but the best they can hope for is on par [inv]- but on par with more energy density would be a big selling point.

When comparing this product to the emerging competition, SLDP is a leader in stability and cyclability, not necessarily in other metrics [inv]. Other companies are delivering similar energy-density results using different technologies. Factorial with oxides and QuantumScape with ceramics and a lithium anode are the two direct competitors.

Oxide batteries are making great progress in buses, where it is feasible to apply the 2 tons of pressure needed to make them work effectively, but it is prohibitive in a car; it adds so much weight that the benefit of the increased energy density is lost.

QuantumScape is working with Volkswagen and scaling up its manufacturing equipment.

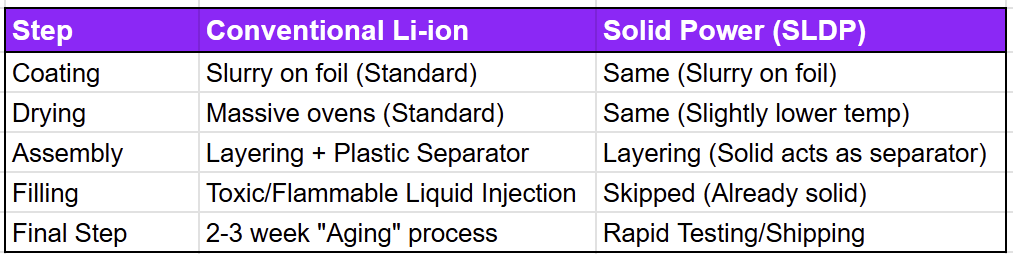

The key competitive advantage of SLDP over its new technology competitors is its compatibility with existing manufacturing processes. The technology can be used alongside the trillions of dollars of machinery already in place. The competitors using Oxides and ceramics require entirely new manufacturing equipment.

I have summarized the process for building a conventional lithium-ion battery and compared it with the requirements for incorporating SLDP.

Flow of Production (Author)

This is the single largest competitive advantage of SLDP; its sustainability will determine the company's long-term fate, but at the moment, it is unique and a defensible competitive moat.

SLDP has proven its electrolyte works; it has demonstrated this with the cathode and the anode. I also believe they can make it at scale. The issue is, can solid-state batteries be made at scale?

Scaled production of the batteries is the final hurdle for them to jump.

SLDP is not going to make the battery or the cells; they are hoping existing battery companies can solve this final issue.

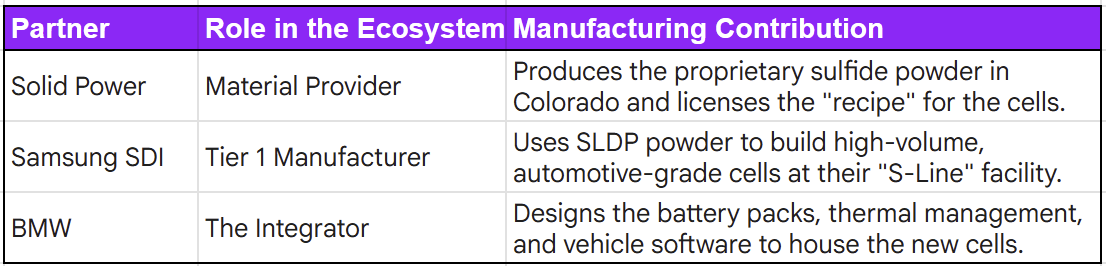

Two large battery manufacturers have committed to installing pilot lines and moving to commercial production, which will likely give them a competitive advantage with their customers if they can turn the technology into batteries.

The original agreement, signed in 2024, is valued at $50 million and has three parts. An R&D license for SLDP's products and processes. A commitment to build a pilot production line at SK On's site in Korea and an electrolyte supply agreement.

The aim is to de-risk the battery manufacturing problem, and the partnership has moved forward quickly. Construction on the pilot line started almost immediately and is now in the commissioning phase. Factory acceptance was completed in early 2026, and the focus will shift to supplying sample cells to OEM customers. SK recently pulled forward the commercialization date by 1 year to 2029.

A second Korean manufacturer, Samsung SDI, has joined the SLDP team.

Samsung has joined the BMW/SLDP joint venture and will manufacture prismatic cells for BMW under the SolidStack brand using SLDP electrolyte and know-how.

BMW released a prototype BMW i7 demo vehicle late last year and intends to have early functional prototype vehicles running later this year.

The SLDP/BMW/Samsung SDI deal is unique in the industry, creating a distributed manufacturing model that could serve as the basis for SLDP's business model going forward.

SLDP/BMW/SAMSUNG (author)

SLDP has two facilities near Denver (Louisville and Thornton). Its current pilot lines have a max capacity of 30 million tons of electrolyte; plans are in place to build this to 75 MTons by end of this year and 140 MTons by end 2028.

In my forecasts, I have assumed that SLDP will co-locate production lines within battery manufacturing sites, should it win contracts, resulting in a total capacity of 500 MTons by 2030.

The agreements with SK On in Korea and Samsung SDI are the models for this expansion.

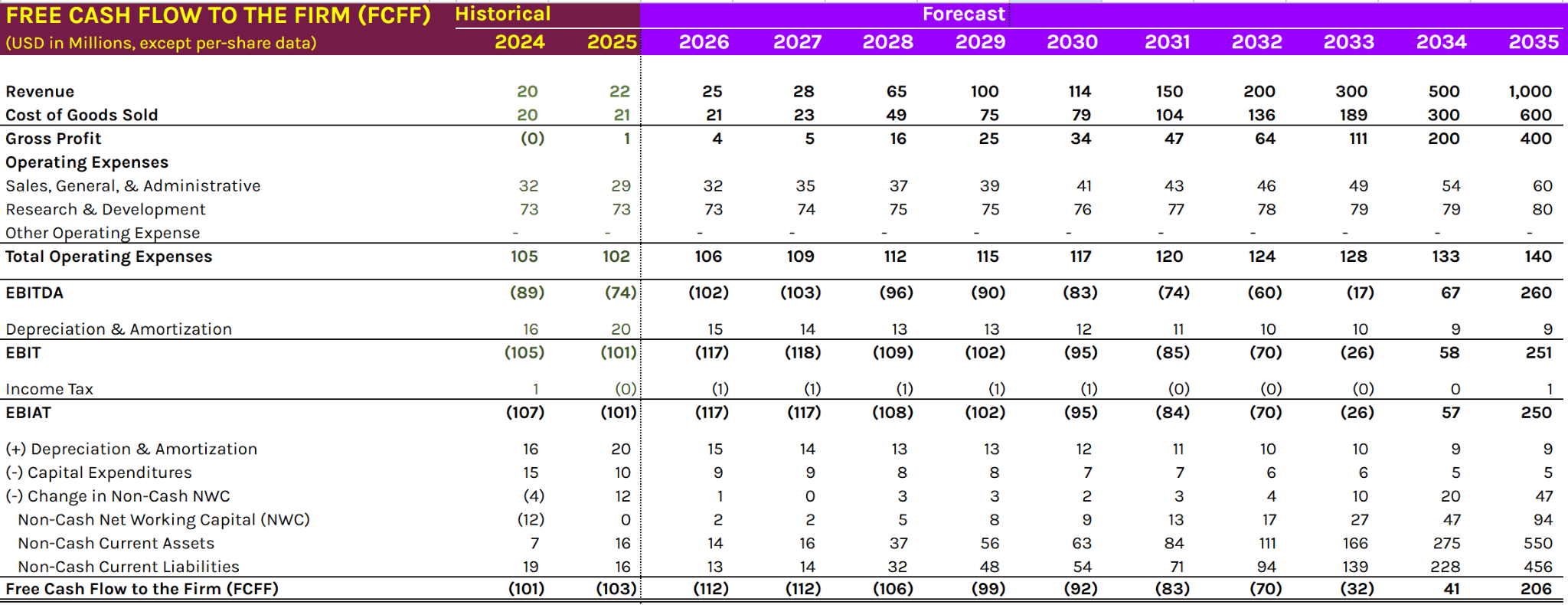

SLDP holds roughly $450M in cash, but it will not be enough, according to my model; we can expect at least another $200M in dilution.

Revenue growth assumes they win the BMW contract and then expand into multiple different customers. It seems a reasonable, if somewhat aggressive, assumption. BMW has built a test car and moved to a higher level of agreement with Samsung as the battery manufacturer, and SK On is targeting 2029 for commercial production.

I use mathematical models to forecast and track the performance of the companies I invest in. I also use them to develop a fair value for the shares. We all understand the difficulty of this type of work and the enormous number of assumptions required.

SLDP Model (Author)

It is the first time that the SLDP model has forecast a break-even date, but it is still way out in 2034, just inside the forecast period. The model is most sensitive to revenue because SLDP has adopted an asset-light business model, in which revenue has little effect on costs.

I think my revenue forecasts may actually be quite conservative, and the $500 million could be achieved in 2030 if things go according to management and SK On plans rather than my more conservative forecast.

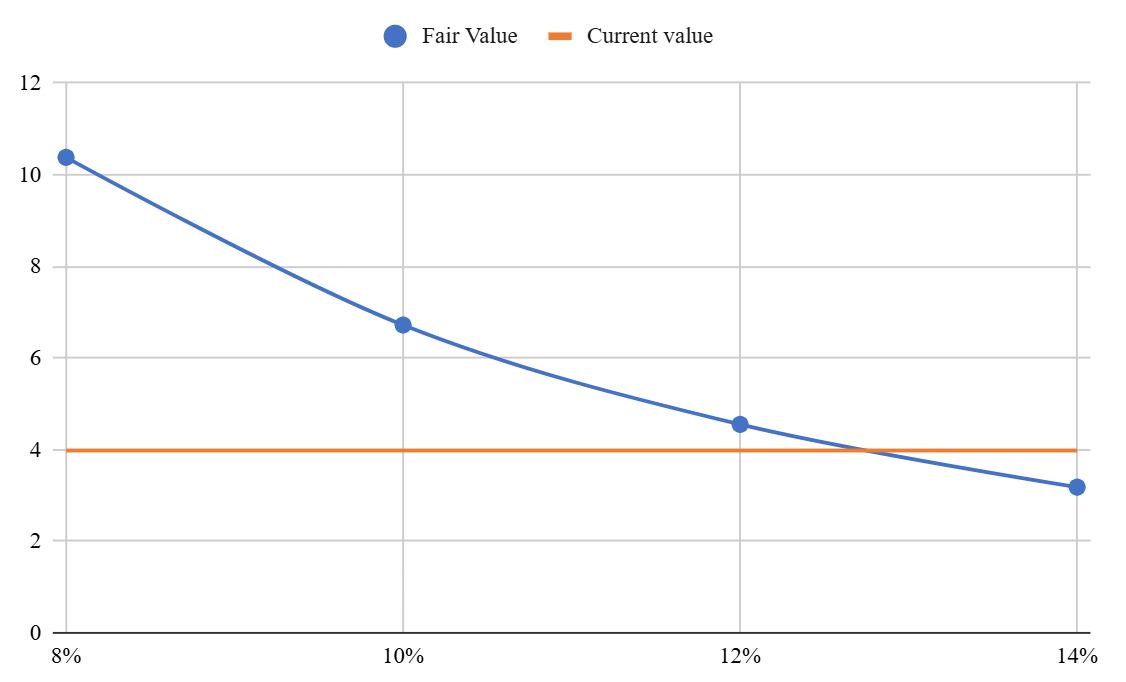

I ran the model at various discounting factors to produce the following chart

Fair Value vs. Current Value (Author Model)

I also ran the model with varying revenue ramps. If the $500 million of revenue is brought forward from 2034 to 2030, the model suggests a fair value of $50 at a 10% discounting factor.

Numerous catalysts exist that could drive the stock higher in the short term, and the two biggest are

Late 2026: Commissioning of the world’s first continuous electrolyte production line.

Ongoing Partner Validation: Continued road-testing with BMW and joint evaluation with Samsung SDI.

I have two primary risk factors. Firstly, they have not yet signed a full manufacturing deal with an OEM. These things can drag on, but BMW and Samsung's commitment gives me hope they will land a deal. Without such a deal, this stock is going back under $1.

Secondly, competition, especially QuantumScape (QS), if QS technology proves to have a significant advantage and can be price competitive, then the key advantage of SLDP- integration into existing manufacturing- could be null and void. If QS or another company demonstrates a significant battery density advantage, most EV manufacturers will be forced to adopt that technology, and SLDP is likely to go to zero.

Other issues

Regulatory Uncertainty: Recent legislative changes (OBBBA Act) have created uncertainty regarding clean energy tax credits.

General EV malaise: the momentum behind EVs has dropped of late

Execution Risk: Moving from lab scale to continuous production is not yet complete

Supply Chain: Sourcing Lithium Sulfide (Li₂S) at scale remains a primary challenge that the company is actively working to de-risk. Li₂S is the primary ingredient of the electrolyte, and currently, there is no scaled manufacturing anywhere that could deliver the volume SLDP will need. They are trying to mitigate this by building their own manufacturing lines and negotiating with multiple contract manufacturers.

SLDP is currently ahead in the race to disrupt the large lithium-ion battery industry in the EV market. It has real advantages in its business model and ability to integrate its tech with traditional manufacturing processes.

I have upgraded SLDP to a buy and taken a small position. If it can land that first volume OEM deal, I will upgrade them to a strong buy and increase my position size.

If you need help managing emerging tech investments, my investing group officially launches on May 4th.

Want a preview of the depth we provide? Visit my blog on Seeking Alpha to see examples of pieces I have recently published in my successful private newsletter; it is an opportunity to see our proprietary "Funnel" strategy in action.

Small-cap investing is not easy, but it does offer outsized potential. Active Followers will receive an article detailing our approach and the returns we have achieved (both good and bad) since we first launched our paid product three years ago.

Strategic Waves (Author)

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。