ismagilov/iStock via Getty Images

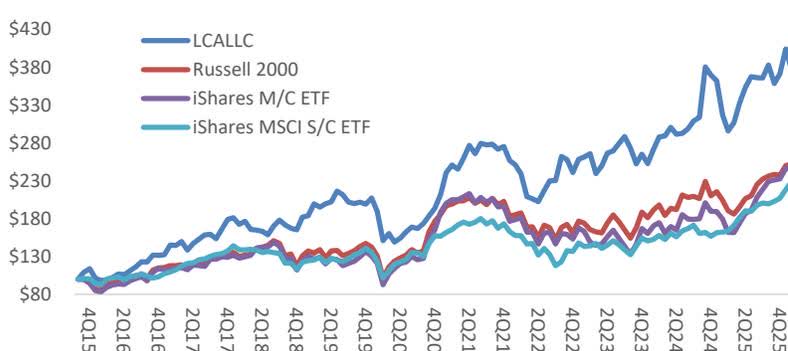

For the 1Q26 quarter ((ended March 31, 2026)), cumulative net returns were flat, roughly in line with indexes that represent small and micro-cap markets: The Russell 2000 (IWM), the iShares US MicroCap ETF (IWC) and the iShares SmallCap EAFE (SCZ) ((ex-N. Am)) ETF. Given the Iran war, inflation and market herding behavior around AI expectations, there was a lot of geopolitical, macro-economic and technological turmoil underlying those flat returns. Since inception in November 2015 through quarter end, LCA has returned a cumulative 270% net of fees, or 13% CAGR, well in excess of those same indices. Past performance is no guarantee of future results. Individual account returns may vary. ¹

Net returns Long Cast R2000 IWC SCZ 2015 (2-mos) 14% -5% -5% 1% 2016 15% 21% 21% 3% 2017 36% 15% 13% 33% 2018 -8% -11% -13% -18% 2019 21% 25% 22% 25% 2020 -3% 20% 21% 12% 2021 42% 15% 19% 10% 2022 -12% -20% -22% -21% 2023 10% 17% 9% 13% 2024 39% 12% 14% 2% 2025 0% 13% 22% 32% 1Q26 0% 1% 1% 1% Cumulative 270% 139% 136% 109% CAGR 13% 9% 9% 7% LTM 25% 26% 46% 28%

Long Cast was founded in 2015 to provide long-term and patient investing in well-researched and well-understood small- and micro-cap companies. We take concentrated positions and aim for 15% annualized returns ((aka “five year doubles”)). We operate as an alternative to passive investing, and with more transparency and less expense than a fund. Listed here are top and bottom performers since inception through 1Q26.

Of the top-performers, at quarter-end MAMA, CCRN and MTRX remained in the portfolio. The bottom performers have all been expensive lessons.

Top Performers Value CTR (%) EVLOLD 0.00 27.68% CCRD 0.00 26.52% MAMA 1,421,803.24 19.40% CCRN 488,179.60 16.01% MTRX 1,767,942.96 13.12%

Bottom Performers Value CTR (%) CTEK 0.00 -7.83% PSSR 0.00 -6.30% ESWW 0.00 -4.79% DAIO 0.00 -4.30% SANW 0.00 -3.12%

PDEX, MAMA and MPTI were largest contributors in the quarter, offset by declines in RSSS, QHRC and PESI. In the first quarter, we added to NRC and CCRN and exited positions in RELL, ENVX and CRAWA ((which was acquired)). At quarter end the top five positions represented 62% of the portfolio.

PURCHASES: I wrote about both NRC and CCRN in last quarter's letter. Nothing has dissuaded me from owning more of the former. The latter was acquired in early May for $13.25 per share. With the deal expected to close in 3Q, I've taken our short-term gains sooner rather than later. At the moment we have excess cash.

SALES: We sold ENVX when the guy whose charge was solving a key manufacturing process exited shortly before its supposed launch. Scaling the company's new battery architecture remains a "science project" and without it I don't see much sizzle on the steak. RELL is a long time value darling benefitting from the AI updraft and it is reinvesting cash flow into new projects, but I sold it as a source of capital. May revisit. CRAWA was compounding capital nicely before it was acquired.

Among our larger holdings:

MTRX (($7.50 avg price)). The company finally reported a profitable quarter and FY4Q ((June year end)) revenue guidan ce o f ~$250M implies FY EBITDA could be ~$15M, which means this is trading at 7x EV / trailing EBITDA, in an environment with several tailwinds. I have urged the Board to observe what has happened at other small E&C's such as STRL, TPC and IESC when outsiders changed the culture at what were previously sleepy regional construction companies like ours. With strong profitability at hand, a newly booked mining project and changes coming in the CEO and CFO positions, there is a wide path for this to grow backlog and earnings and re-rate higher.

PDEX (($28.51 avg price)). We discussed PDEX at length in our 3Q25 letter. As expected, the company completed the acquisition of a primary supplier, which could negatively impact margins in the short term but offer more substantial long-term upside.

As with all our investments, our bullish thesis around the company is ultimately driven by observing the kind of value creation a capable management team can achieve over time. One way to illustrate this is through the company's growth in book value per share, which has compounded at 20% over the last seven years.

The renewed contract with "customer 1" should support near term earnings and at 15x EBITDA it seems fairly valued on that alone. Zimmer Biomet (ZBH)'s expected commercialization of Monogram's mBos system could radically accelerate value creation. PDEX is a contracted and critical supplier to the platform. One need only listen to ZBH conference calls to see the extensive resources supporting its expected '27 launch. ((Concurrently, as a point of caution, one need only look at ZBH stock chart to see that the market is skeptical)). If hurdles are met along the commercialization process, PDEX will realize gains on "valuation rights" it received in the Monogram sale. If commercialization is successful, the opportunity path would be multiples longer and wider.

MAMA (($2.95 avg price)). As you know, I spent an earlier part of my pre-finance career working for a private investigator doing background research on management teams, typically on behalf of a lending or investment office. Its work that still informs my investment process today because I think management due diligence provides a strong signal. I know other investors who prefer to never meet management teams, because they want to own businesses any idiot can run and / or they want to avoid biases of thinking they understand how people are likely to operate. The varying perspectives is part of what makes markets great.

I mention all this to re-emphasize my perspective on the importance of management in smaller companies. Exceptionally run companies are rare and unusual, and we should want to own rare and unusual things because they can retain value and are hard to replicate. But even exceptional companies have dysfunction that an outside investor will never see. On the spectrum of dysfunction, the average small public company is probably mediocre, often through neglect or a lack of awareness of alternatives, which often starts at the top. And even companies that make effortful intentions towards operating improvement and capital allocation can fail because it's hard and complicated. All of this is similar to the range of sports teams and their outcomes and the observations one can draw on consistency and process. I cannot imagine rooting for a sports team and not thinking about how roster construction and coaching decisions influence the players and team.

Under prior management, the CEO's son in law ran operations and results were mediocre. Since 2023, when the current CEO started, a well-regarded former consultant with limited experience as an operating manager, MAMA has grown tangible book value per share from $0.06 to $0.97. Under his management, even the Board is chosen with the intention of mentorship for the executive team, a superior strategy compared to other companies. This may be what exceptional looks like.

MAMA has a vision of being a +$1B revenue company and management has been operating against this plan. The stock is presently trading at a high valuation on a trailing basis but assuming they achieve the target while holding margins steady ((and margins would likely improve with scale)) than this is outright cheap. I think it fits our paradigm of a five-year double which is why we continue to own it.

RSSS (($2.57 avg price)). The last 50 years – my lifetime - has seen countless advancements in many areas of industry, from healthcare to payments to tooling, but I think more than anything the change in media – the Internet – has broken everything and caused vast re-sorting. It's a great environment for entrepreneurs.

Since we initially made our investment in RSSS, AI has emerged as a technological threat to the information services industry. I see AI as a tool, like obsidian, fire, the wheel, etc. and I don't believe (as I've heard others say) that it will be the last tool humans invent.

Taking this tool-analogy one step further, it is said that the person holding a hammer sees everything as a nail. I think that's where the market is with AI; it thinks it will cudgel everything. I disagree. Companies that learn to use the tools and build around them should do well. Again, a great environment for entrepreneurs.

Growth has slowed in recent quarters off of harder comps, and the question is whether this is a secular AI driven challenge or an operational issue. Deferred revenues offers evidence of an improving slope ahead, and meanwhile cash flow generation and valuation remain attractive. Within the executive ranks - and it's a pretty flat organization - are entrepreneurial and talented engineers and managers "hooked" on AI and innovating quickly. Furthermore, in a budget constrained academic environment, universities are trading down. Anecdotally, a friend who works at one in the intersection of scientific research, academia and law ((and who for years has been barely aware of the company)), is now a customer of Article Galaxy because it helps their organization lower costs. The only problem, the friend said, are the rumors that the company will be acquired. This would be music to the ears of shareholders.

There's barely any asset that a small company owns that a large company can't replicate, except for its people and culture. Ironically, as companies get larger, and layers of management intrude, those factors are harder to sustain. Some large companies do it well at scale and many small companies do it poorly. But for a small company to get big, it either needs a killer product, or good people and culture, which starts from the top. To reinforce a notion I've beaten to death in this letter, it's why I care so much about the executives running our companies.

As always, I remain committed to building a durable and sustainable business based on a repeatable investment process and intelligent capital allocation. I remain grateful to have clients ((by design)) aligned with my long term, small company centric and research-intensive focus. I welcome the continued interest from individuals and institutions as I patiently grow the business.

Sincerely

Avi

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。