ArtMarie/E+ via Getty Images

There are three parts to this article:

There are quite a few attractive opportunities in preferred shares and some reasonable choices in the baby bonds as well. We're a bit spoiled for choice. I decided to add AGNCP as it's one of the lowest-risk-rated preferred shares, and we didn’t have much exposure there. It also has a reasonable case for bouncing back relative to peers, which enhances the appeal.

I would like to collect the stripped yield until we see the relative valuations even out between the AGNCP preferred shares. I think we’ve got a decent shot at pulling in a moderate capital gain over the next three to six months. I don’t mind sitting in the shares longer, but I have no problem taking the gains and walking away or swapping to a different share if valuations support that.

These are the prices presently:

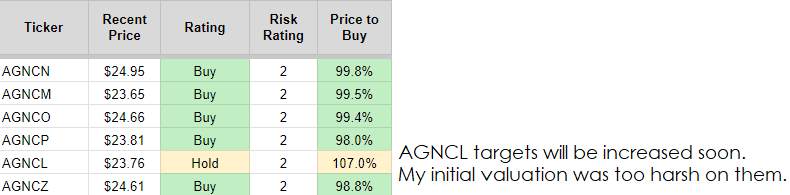

Note: The target on AGNCL was increased materially since this screenshot. (The REIT Forum)

I'm highlighting that the AGNCL targets will be increased because the 107% ratio is too harsh.

However, the reason for the image is so investors can see the price-to-buy calculations on the other shares. Especially the first four. Those should be closer together.

I am planning to release a public article on AGNCP soon, and I’ll include the article at the bottom.

This is my order execution

The REIT Forum

Source: Schwab

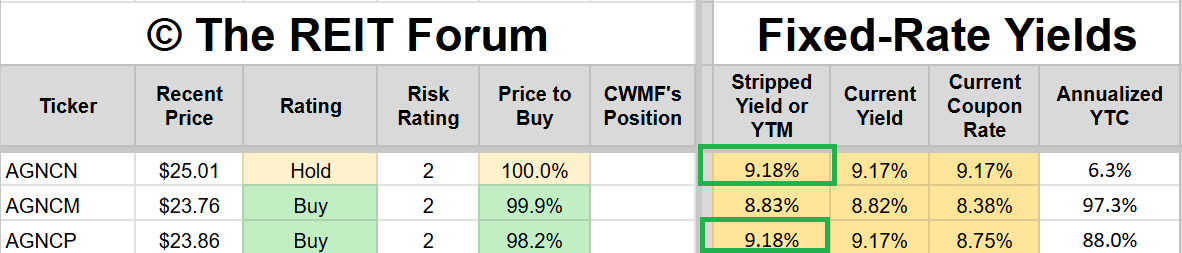

AGNCP (AGNCP) is a floating-rate share from AGNC Investment Corporation (AGNC). The strip yield on the share is fairly attractive.

The REIT Forum

Note: This screenshot was taken right before updating my portfolio to include a small purchase of AGNCP. Consequently, it shows CWMF’s position as blank. It's now 0.62%.

It comes in at 9.18% and is very comparable to several of AGNC's other preferred shares. In particular, I find AGNCP a little bit more appealing than some of the alternatives (using recent market valuations) because the strip yield is only a tiny bit lower, but the discount to call value is materially larger. Therefore, an investor initiating a position in AGNCP would only lose out on a very small amount of quarterly dividends, but they would get materially more upside in a scenario where credit spreads tighten.

If credit spreads were to widen, it would not create materially more downside for AGNCP than for the other related preferred shares. Since the yield is a primary factor in valuation, the very comparable yields would be expected to move by a similar amount.

You can see comparisons for a few of the shares below.

The REIT Forum

Note: This screenshot was taken right before updating my portfolio to include a small purchase of AGNCP. Consequently, it shows CWMF’s position as blank. It's now 0.62%.

Is there any case where AGNCN wins over AGNCP? Sure, there are technically two scenarios:

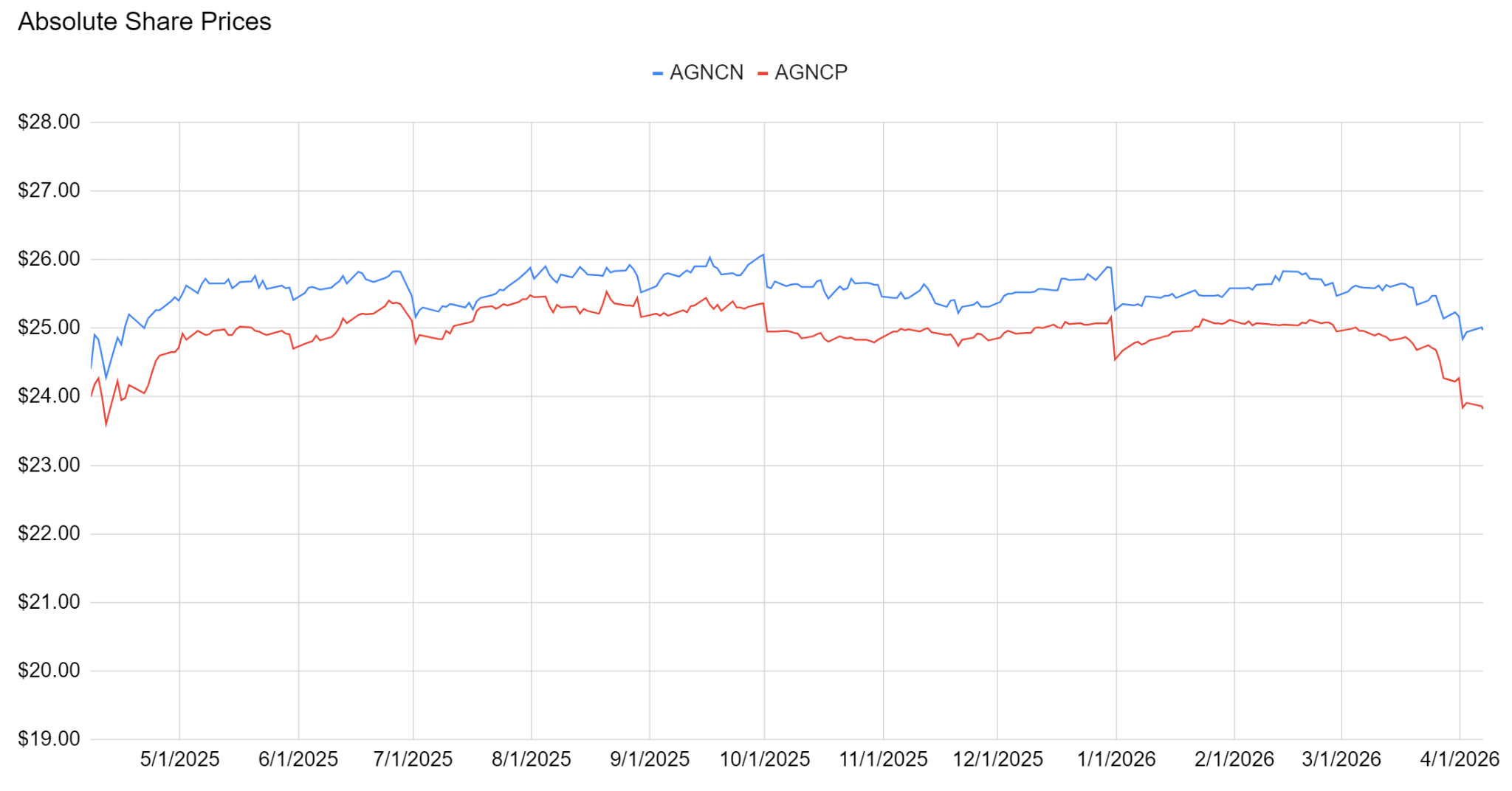

We usually see AGNCN trading at a higher price than AGNCP. The shares always go ex-dividend on the same date, so we can simply chart the share prices together to establish the normal spread:

The REIT Forum

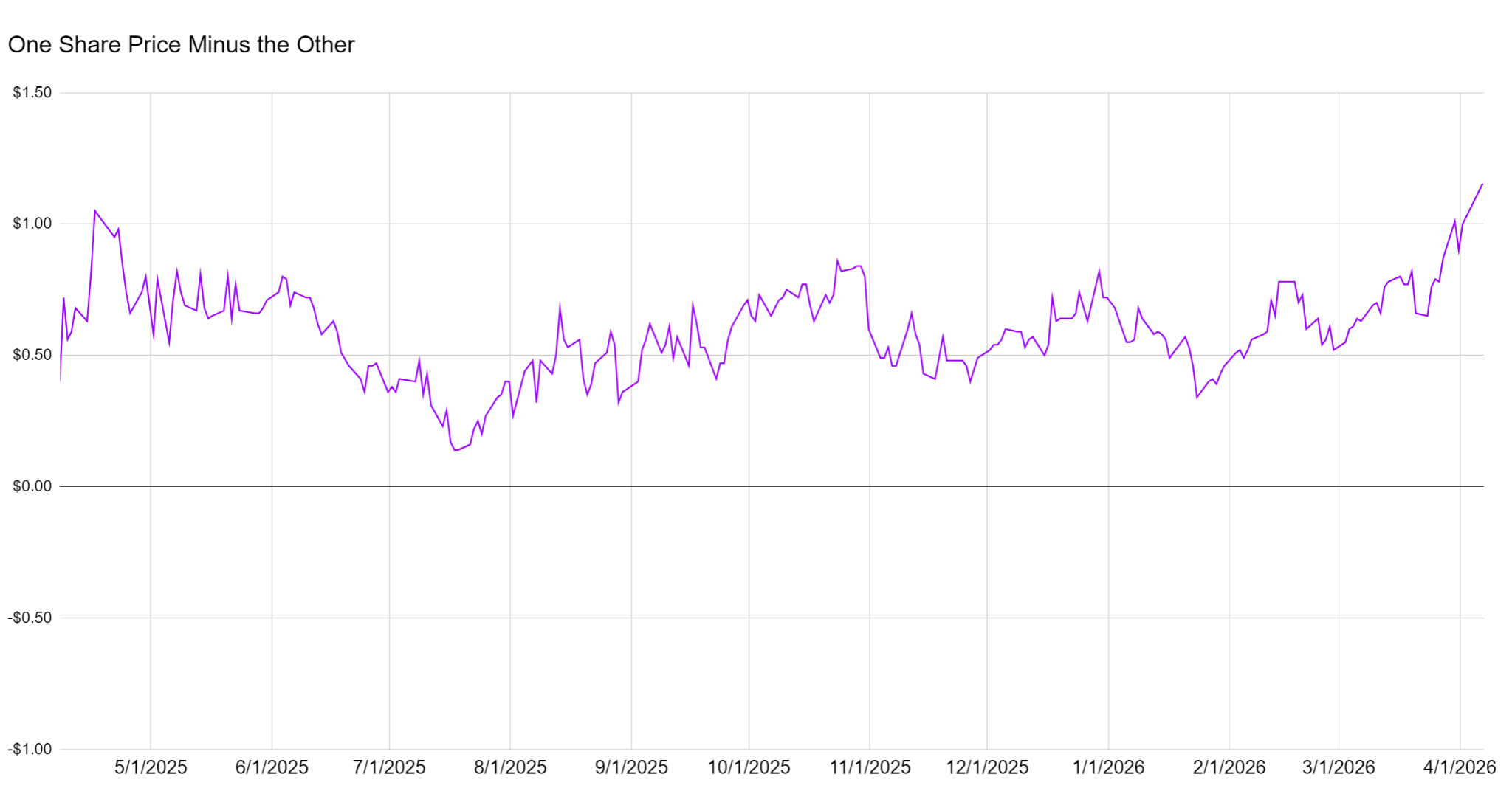

You can just eyeball that chart and tell that it feels like the spread is unusually large. However, we can also simply chart the difference in the share prices:

The REIT Forum

That chart makes it pretty obvious that this spread is unusual.

AGNC also has other preferred share options investors may consider. I was initially a bit too harsh on AGNCL (AGNCL). That's the fix to reset share. My targets there need (or needed, depending on how quickly this is published) a little bit of an update. We primarily run our targets based on discounting future cash flows and creating a slight adjustment in the required yield based on the implied upside to call value. Of course, we also require higher yields on higher-risk shares and lower yields on the less risky ones.

For instance, if you had two preferred shares from the same REIT and:

Then you should find the share with the lower price per share more attractive because you get:

In that scenario, you’re getting the additional upside for free. We could debate for hours about precisely how much value it deserves, but the value is greater than $0.00. Ultimately, there's usually some level of trade-off between upside and yield, and we want to optimize for finding the best combinations available in the market within our sector at any given time.

Common stock for AGNC has generally been quite popular with investors over the last year or two. The price-to-book ratio has been remarkably high at times. Investors have been excited by the high level of core earnings reported by the REIT. While that's favorable, I wouldn't put too much of an emphasis on the core earnings. If they were terrible, that would be more of a concern. However, having an extremely high core earnings yield on book value presently is less relevant to the long-term health of the REIT, particularly from the perspective of the preferred shareholder.

The investor in the preferred shares is interested in the coverage ratio for the preferred dividend and the preferred equity position. We've seen AGNC issue a substantial amount of common equity over the last few years. That common equity is very useful for creating a cushion for the preferred shareholder.

There have been a few other opportunities where AGNC's preferred shares have dipped into the attractive range. However, they don't spend very much time there. At least over the last few years, it has been significantly less common to find them trading at a discount where we would consider them attractive. They typically traded slightly above our targets.

The biggest concern for an investor in these shares is probably the floating rate aspect. If short-term rates were to decrease significantly, it would reduce the required dividend payment. We've already seen a reduction in short-term rates and the resulting change in the dividend. However, it still offers investors a fairly compelling yield with moderate upside. In conclusion, I think AGNCP is a reasonable value today. It's not absolutely amazing, but the combination of the stripped yield and the upside is good enough to be appealing.

I think AGNCP is a good pick here. I think the recent weakness made shares more attractive. It gives investors a modestly higher yield, and it creates materially more upside to call value. I'm not expecting that a call is going to happen, but I'm recognizing that AGNCP has historically traded between about $25.00 and $25.40. The floating-rate aspect is more attractive today than it was over the last year because the market forecast for future changes in SOFR is more attractive. Further, the disparity in valuation between the AGNC preferred shares demonstrates that the market is not discounting the other AGNC preferred shares as harshly as AGNCP. If the market is right about the other shares, then it's modestly undervaluing AGNCP.

For investors in an alternative share like AGNCN:

Swapping to AGNCP would generally be a wise move if the investor can execute the swap with a highly favorable spread:

At the time of publishing this to subscribers of The REIT Forum:

That spread of $1.14 is the highest we’ve seen since 1/30/2025. For reference, AGNCP was a fixed-to-floating share. It did not start floating until 4/15/2025. So investors who were getting a slightly larger spread back on 1/30/2025 still had to absorb a smaller dividend rate for the next payment.

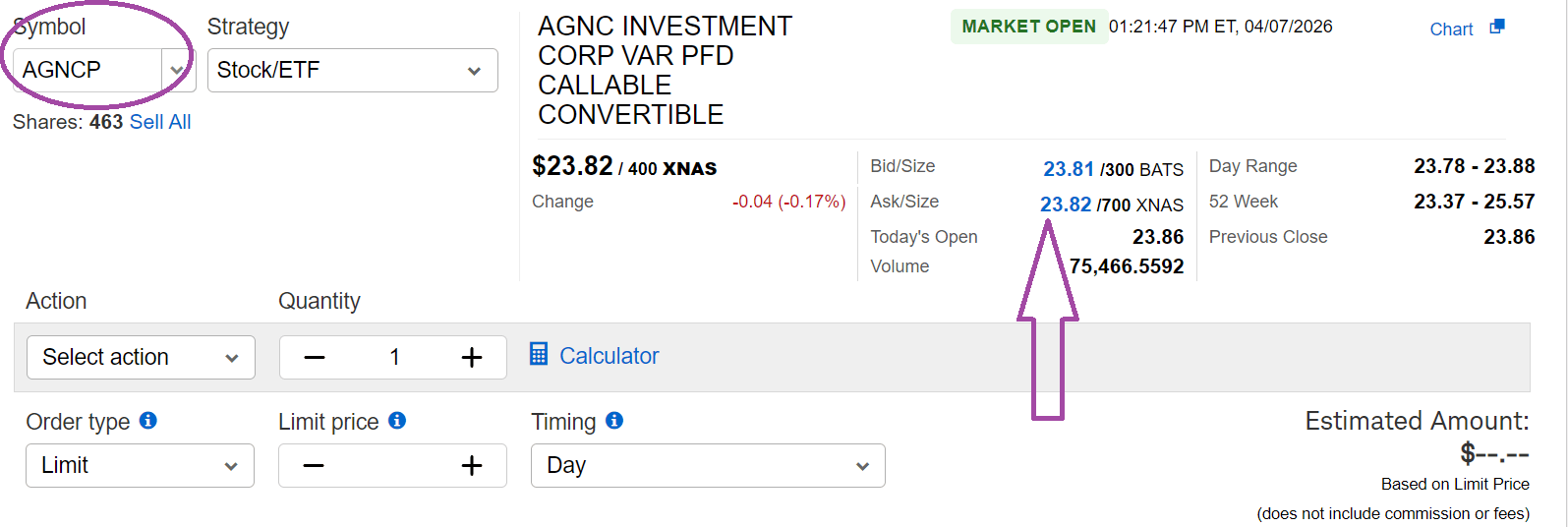

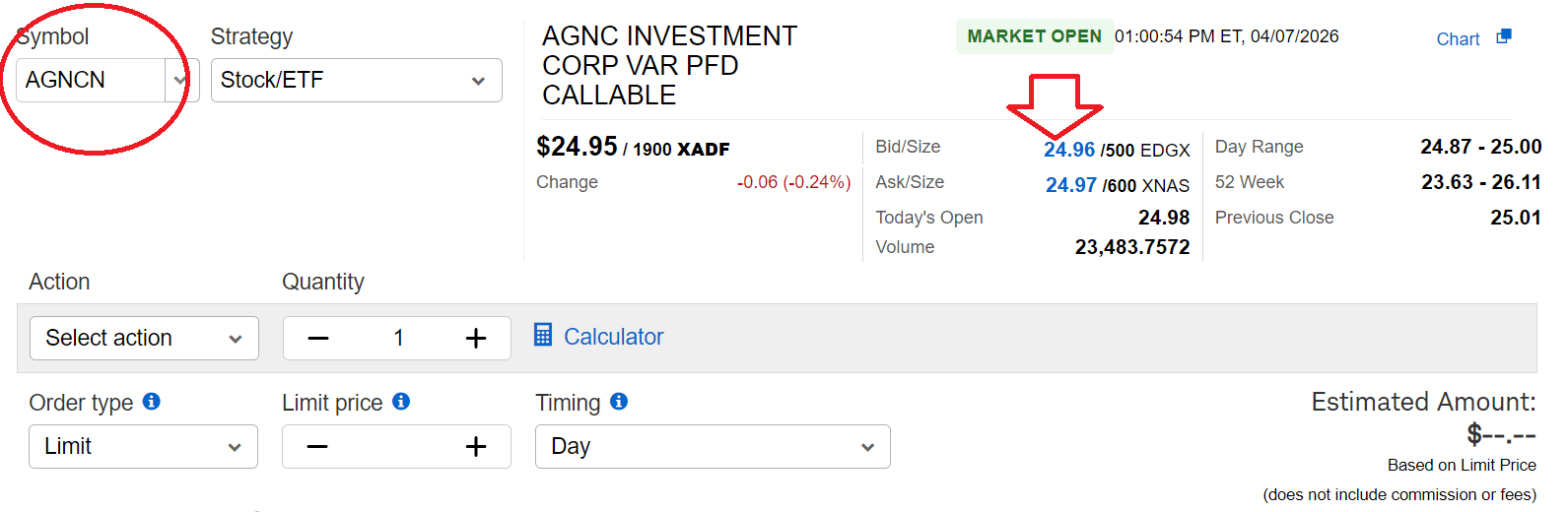

I’ll include screenshots from my account pulling up both shares in the trade ticket so investors can see that these prices are actually available in the market:

Charles Schwab and The REIT Forum

Charles Schwab and The REIT Forum

Happy trading!

Sometimes income investors think these ideas on how to swap won't be relevant for them. Yet the ideas are relevant because they enable the investor to grow their position. Swapping when the spread is favorable is how an investor can increase their share count without reinvesting the dividend. It's a way for an investor in AGNCN to temporarily switch to AGNCP, then switch back to AGNCN when the valuation favors that. The investor ends up with more shares after the round trip because they are taking advantage of a mistake in market valuations.

Beware of liquidity. Prices may move after the alert. AGNC has some of the more liquid preferred shares. Prices usually won't move as much and may return to around their prior levels given a little time. Investors should never use market orders on preferred shares. I'm very deliberately including the sample spreads from $.90 to $1.10 to make it easier for investors to evaluate in real time. If the spread plunges, then the appeal of swapping between shares would disappear.

Since we initially published that note to subscribers, we have a few changes:

Here are the last prices for each of those shares:

AGNCP should trade at a higher price than AGNCM because the difference between the shares is that AGNCP gets about $.09 more in dividends per year. Same ex-dividend date. AGNCP simply has a slightly larger spread.

AGNCP rallied out of our target price range, so I'm marking the article as neutral. However, I still think the valuation is a bit more favorable than peers. In particular, AGNCP stacks up favorably relative to AGNCM since the shares are extremely similar other than AGNCP getting a higher dividend rate and trading at a slightly lower price.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。