bombermoon/iStock via Getty Images

Protean Small Cap returned 7.5% in April. The benchmark index rose 3.6%. Since launching in June 2023, the fund has gained 67.6%. The Carnegie Nordic Small Cap Index is up 26.5% in the same period.

The hedge fund Protean Select returned 1.7% in April. It now manages 994m SEK. When the fund reaches 1bn SEK, we will announce closure for additional subscriptions.

Protean Aktiesparfond Norden returned 3.9%. The benchmark index rose 5.4% Since inception, a little over a year ago, the fund is up 22.9%, and in the same period the VINX Nordic Cap index is up 18.9%. The fund now manages 1.9bn SEK.

All figures are net of fees.

This month's letter elaborates on the Rashomon effect: the concept made famous in Kurosawa's movie, how it's possible to view the same story from different viewpoints and come to opposing conclusions, and both (or all four, as is the case in the movie) be right. A quick mention of a new book. Some new additions and deletions from the funds. Plus, as always, commentary on the month's various winners and losers.

Thank you for being an investor!

// Team Protean

April 2026 • Written by Pontus Dackmo

If there's a single position that embodies the Rashomon effect this month, it's Vend ((previously known as Schibsted)). Regular readers may recall our short case in the same stock from the October letter: network effects growing fragile, revenue growth dependent on ARPA hikes rather than volumes ((which presumed a behavioural stability we doubted)), management's dismissive tone towards AI disruption, and a stock at NOK 340 that priced in a potentially eroding durability.

The stock fell 30%+ over the following months. Our witness was right. Case closed?

Not so fast. In Kurosawa's film, the twist is that the same events genuinely look different depending on where you stand. And where we stand has evolved. Both we and the market have had time to digest the AI-impact, and our thinking has evolved from: can Vend sustain its premium? to a more relevant question when the stock was trading sub 240 NOK: is the market now pricing too much disruption?

Stress-testing the AI threat, we've started to think it is limited, at least in the short to medium term. Marketplaces own their inventory, which means LLMs cannot legally scrape or replicate it. It is notable that OpenAI is building partnerships with incumbents rather than attempting to build competing platforms. There is a scenario where the disruptors need the platforms more than the platforms need them. Sure, the long-term risk remains as entire business models are in flux and progress is linear if not exponential, but the timeline has surely been pushed out.

At the same time, Vend continues to simplify and is delivering reasonably on both cost initiatives and shareholder friendliness. There is a lot of fear baked into the valuation when the stock trades at a material discount to peers with free cash flow yield in the double digits. Add to the mix that M&A has returned to the classifieds space with none other than memestock hero Gamestop (GME) bidding for Ebay (EBAY) ((!)), and that Vend has initiated a substantial buyback programme with potential to keep going for quite a while.

During April, we initiated a long position.

We have no qualms about changing our mind when the price changes. It reflects evolving expectations and flexibility, not inconsistency. The bandit, the wife, the samurai, and the woodcutter all saw the same sword fight in the movie. They all told the truth from different angles. In our case the angle has simply changed: 30% of the equity value gone, a potentially better understanding of the AI timeline, and a management team that is doing the right things with its excess capital.

A brief personal detour: I've written a book that will be published towards the end of May. It's called Börssjävel, which doesn't translate well, but you can replace it with the word in any language you mutter to yourself when the stock you just bought went straight down, or the one you sold went straight up.

The book covers the Protean origin story, is occasionally personal, and tries to explain how I and we think about investing. It also contains a reasonable chunk of industry criticism, and how our little project attempts to navigate some of the potholes of the business.

Why write it? Partly because I think the Swedish equity market deserves a book that doesn't read like a textbook on "how to get rich" or a LinkedIn post. Partly because the process of putting twenty-odd years of pattern recognition into words forced me to confront which of my beliefs are actually real. That exercise alone was worth it. Whether it's worth 259 kronor to you is another matter entirely.

Why write about it here? Because the regular reader will recognise many of the ideas that we have written about in these Partner Letters (we have published >50 Partner Letters since inception, they're all available on our website). But this time without the brevity constraint, and with a professional editor on top.

If you read it, I hope you like it. If you don't, I'll borrow Charlie Munger's line about the book Poor Charlie's Almanack : "If you find you don't like it, you can always give it to a more intelligent friend."

April 2026 • Written by Pontus Dackmo

Protean Select returned +1.7% in April. A satisfactory result given the carried over cautious positioning that enabled us to have a positive return in March, where markets were down significantly. Protect the downside, participate reasonably in the upside – if we can keep doing that, we will be ok.

Nordic indices gyrated during the month and closed off the best levels but still up by around 4%. The average beta-adjusted net exposure of the fund was a mere 12% on average.

Biggest contributors were Acast (ACASF), Mycronic (MICLF) and Cint (bid).

Biggest detractors were short index futures, a short position in Nokia (NOK) ((yeah that was dumb)) and a position in which reported so-so figures during what hopefully is a transition phase.

We enter May at 19% net exposure. Gross is now at 128%, as we have continued to nudge it upwards, moving gradually back towards our historical average of around 135%.

We said going into the year that we wanted to earn the right to take more risk. April was another step in that direction. Let's see what May has to say about it.

Once we reach above 1bn SEK we will announce the closing of Protean Select for additional subscriptions. Entering May we are at 994m SEK. As the rules are constructed, once we announce the closing, there will be one more subscription period before actual close.

We have started to build a position in Yubico. The stock is down roughly 85% from its 2024 highs ((!)), which is either an opportunity or a stark warning. At SEK 42, the market cap is SEK 3.7bn. The company has SEK

856m in net cash and SEK 716m in inventories (which at a 77% gross margin carry a sales value north of SEK 3bn). The market barely assigns any value to future operations, and we should be honest: there are reasons for that. Not least two consecutive profit warnings and a shareholder roster with more burned fingers than a pyromaniac convention.

Large enterprise rollouts (orders >1m USD) have fallen sharply as organisations hesitate in a volatile geopolitical environment. In USD terms, R12m orders are down 2% year-on-year while OPEX is up 8%. The company invested to meet demand that hasn't shown up ((yet?)). Margins have compressed accordingly. A cost savings programme is underway and prices have been raised, but these are reactive measures, put in place by a violently reshuffled management team that has seen significant change since the SPAC/IPO late 2023. We estimate/hope/think 2026 is a trough year, and on reset sell-side estimates the stock trades at around 7x EBIT for 2028. That's cheap, but cheap alone has never been sufficient reason to own something.

Where we think there might be an emerging lifeline is in how artificial intelligence is radically changing the threat landscape around cybersecurity. Anthropic recently launched Mythos, a frontier AI model built for offensive cybersecurity. The implication is a world where AI finds software vulnerabilities faster than humans can patch them. If your second factor of authentication is a software token on the same device an AI agent can control, the security boundary becomes targetable through phishing, session hijacking, and token theft, at scale, without fatigue, around the clock. Our conversations with the company have strengthened our view that the gap between hardware-bound and software-only credentials is widening materially. This is, to put it mildly, contrary to the current narrative in the stock. Whether the market will come to appreciate this distinction, and on what timeline, we obviously don't know. But we do know we have started the process to implement YubiKeys ourselves at Protean, even before initiating the position, in light of the ever-increasing number of sophisticated phishing attacks we are subject to.

Last week, OpenAI announced a partnership with Yubico to offer co-branded YubiKeys to ChatGPT users. We also found out in an interview that OpenAI already uses YubiKeys internally. The revenue impact is most likely negligible, but it's a useful data point: the world's most prominent AI company chose hardware-backed authentication not only for itself, but for its high-value accounts. Yubico has also started positioning for agentic AI: the Role Delegation Token framework would require a physical key tap to authorise autonomous AI agent actions. This is early, speculative, and may amount to nothing. But if the concept gains traction, it would meaningfully expand what a YubiKey is for.

The bear case is straightforward: free software passkeys from Apple (AAPL), Google (GOOGL) and Microsoft (MSFT) are good enough for most organisations, and Yubico's addressable market narrows rather than expands. We could be both early and wrong here, but the risk/reward given the early encouraging signs and rock-solid balance sheet looks attractive. We're watching the OpenAI June 1st compliance deadline for adoption data, cost programme execution, and whether further AI-platform partnerships follow. Things are moving fast in AI-space right now.

April 2026 • Written by Carl Gustafsson

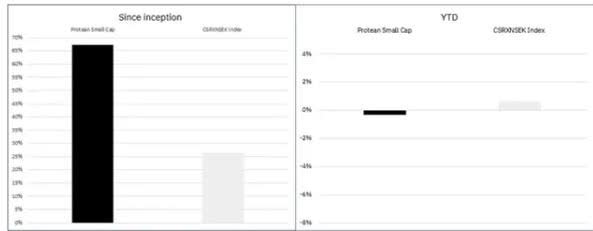

Protean Small Cap returned 7.5% in April. Our benchmark, CSRXN (SEK), gained 3.6% during the month. Hence, the fund outperformed the index by 3.9%. Since inception in June 2023, the fund has outperformed the index by 40.8%. Total performance since inception is 67.3% net of fees.

The fund now manages c. SEK 1,055m, following continued inflows. Thank you for your trust.

Contributors included CINT, Acast, MTG, Devyser (DVYSF) and Coffee Stain, with honorable mentions to NCAB (NCABF), Autostore (AUTSF) and Sdiptech (SDTHF). We also benefited from strong quarterly reports from companies such as Vimian (VIMGF), Autoliv (ALV) and AAK (ARHUF).

The main detractors were Ossdsign (OSSDF), Afry (AFXXF) and Lindex. Ossdsign has become one of our largest detractors, as its growth trajectory has stalled amid significant turnover in its sales force.

CINT became our largest contributor for the month following a bid from a consortium formed by the main owner Bolero, the private equity firm Triton, and CINT's CEO and COO. As we wrote in the March letter, we increased our position following the strong Q4 report in February. The Q1 report ((pre-released in conjunction with the bid)) further underscored that CINT has resolved many of the issues that led to the horrendous Q3 report in October. Despite a rebound in the share price so far this year, and even including the bid premium, the share still trades below the levels seen prior to this pause in operational performance.

Several of the positions we added in February contributed to performance in April, including Coffee Stain and MTG. Coffee Stain appears to be in the process of re-establishing its footing following the spin-off from Embracer. While the share has rebounded approximately 25% from its lows, the valuation remains attractive, particularly compared to its main peer, Paradox. Upcoming releases could act as further catalysts. MTG announced its intention to list parts of its Indian subsidiary

Playsimple at a valuation far above MTG's current mid-single-digit EBIT multiple, and later in the month reported strong quarterly results.

We have added two new positions that we would like to highlight:Absolent and Luotea (LASKF).

Absolent develops products for cleaning process air in manufacturing and commercial kitchens. It is a Swedish company with revenue of approximately EUR 130m, but with global reach through partners. Having long been a favourite in the Swedish small-cap community, the share has endured a multi-year drawdown and now trades at levels last seen in 2018. This decline is partly due to a gradual erosion of margins, which fell from a high of 20% to 12% last year, as well as a slowdown in organic growth. While there are several explanations for this development, it appears that Absolent now has turned a corner, with two consecutive quarters of organic growth combined with margin expansion. A new product platform has likely supported the return to organic growth despite limited market tailwinds. 2025 appears to mark the trough in operational performance, and the shares still trade at a 10-year low.

Luotea is a Finnish provider of facility services, a peer to Coor ((which has been a holding of ours historically)). Luotea remains below the radar of most investors, having recently been separated from Lassila & Tikanoja. Operationally, the company has successfully turned around its Finnish operations over the past few years and is now applying the same toolbox to its Swedish operations, which have had a weak track record. Exiting loss-making contracts should support margin recovery. The shares already appear inexpensive despite Sweden being loss-making. If the Swedish operations were to reach break-even, Luotea would be valued at a mid-single-digit EBITA multiple. It is also worth noting that despite being a pan-Nordic facilities manager, Coor has struggled to establish a meaningful presence in Finland, remaining subscale despite many years of operations. A potential tie-up between Coor and Luotea could address this.

To make room for these additions, NCAB has exited the portfolio following very strong year-to-date performance. While we remain positive on the business model, we are concerned that a boom-bust pattern may be emerging in customer demand.

Our top ten positions as we enter May are as follows:

Rank Holding % of portfolio Rank Holding % of portfolio 1 Acast 4.5% 6 Vimian 2.9% 2 Cint 3.9% 7 Coffee Stain 2.8% 3 Devyser 3.4% 8 Storytel (STRYF) 2.7% 4 Storskogen 3.2% 9 Bavarian Nordic (BVNKF) 2.6% 5 BTS 3.2% 10 Arctic Falls 2.4%

April 2026 • Written by Richard Bråse

Aktiesparfonden is a Nordic long-only fund aiming to generate above-market returns over the long term by active investing in value-creating companies and charging a low fee. A fee that is reduced further as the fund grows, sharing the scale advantages with investors.

Aktiesparfonden has, since inception a little over one year ago, delivered a 22.8% return, in the same period the VINX Nordic Cap index is up 18.9%. The fund now manages 1.9bn SEK.

Our communication for Aktiesparfonden is currently only in Swedish, and updates can be found at Protean Aktiesparfond Norden by clicking the headline “Anslagstavla”.

Thank you for your long-term perspective and trust in our process.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。