Alexey_Arz/iStock via Getty Images

The Simplify Interest Rate Hedge ETF (PFIX) was launched on May 10, 2021, with the objective to offer protection against rising long-term interest rates and to benefit from market stress when fixed income volatility increases. PFIX is an actively managed ETF with a 30-day SEC yield of 2.73%, a trailing 12-month yield of 10.76%, and an expense ratio of 0.50%. Distributions are paid monthly. It is a small but quite liquid ETF, with $202 million of AUM (assets under management) and an average daily dollar volume of $32 million. The sponsor, Simplify, is an asset management company founded in 2020 with about 40 ETFs and $13.7 billion of total assets under management.

The fund invests in derivatives and income debt instruments. As described by Simplify, the targeted derivatives include swaptions, interest rate options, and Treasury futures. A swaption (swap option) gives the right, but not the obligation, to enter into an interest rate swap on a specified date at a specified rate. The fund’s long and short positions in swaptions and options aim to gain primarily from rising rates and secondarily from increasing rate volatility. Derivatives are rebalanced after large rate movements or when their rate sensitivity has declined. The fund keeps a maximum net exposure of 25% in any over-the-counter derivative issuer to mitigate counterparty risk.

The fund may also invest in Treasuries, ETFs holding Treasuries, and investment-grade bonds for income and as collateral for derivatives.

As an example from April 24, 2026, PFIX has 58.4% of asset value in Treasury bills, 31.5% in a Treasury bill ETF (SBIL), and 10.4% net in swaptions (14.1% long and 3.7% short). With this portfolio, the fund boasts a negative duration of -36.95 years. It means the portfolio's asset value would change by approximately 37% for every 1% change in interest rates, in the same direction. The portfolio’s composition and duration may change over time.

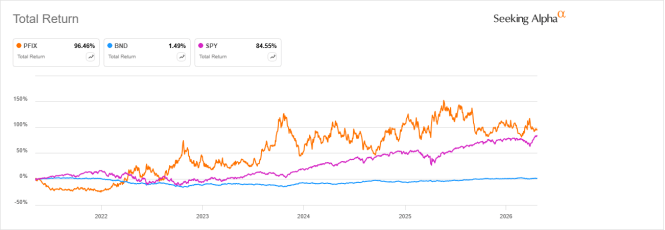

PFIX has a total return of over 96% from inception to present, outperforming a total bond market benchmark (BND) and, more surprisingly, an equity benchmark (SPY).

PFIX versus BND and SPY (Seeking Alpha)

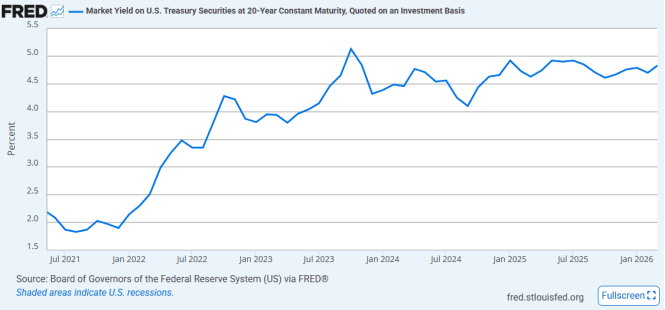

This is not representative of future returns: PFIX was launched a few months before the largest hike in interest rates since the 1980s. This period was extremely favorable to the fund’s strategy: the 20-year Treasury yield surged from 1.90% in December 2021 to 5.13% in October 2023, then went sideways between 4.5% and 5% through March 2026.

20 year Treasury yield (St Louis FED)

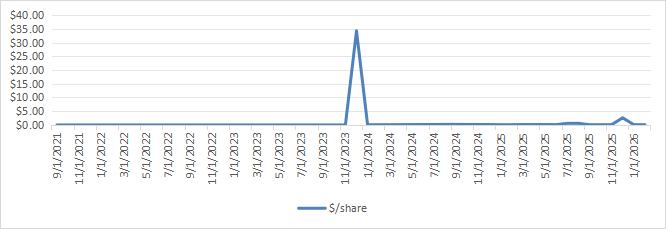

However, the share price has lost 7.8% since inception: it surged, then fell back and went sideways.

PFIX price return (Seeking Alpha)

In fact, the drop on December 26, 2023 (-46%), was due to a special one-time dividend of $34.267.

PFIX distribution history (Chart: author; data: Simplify ETFs.)

FolioBeyond Alternative Income and Interest Rate Hedge ETF (RISR) is an interest rate hedge ETF based on mortgage-backed securities interest-only strips (“MBS IOs”). Additionally, inverse leveraged long-term bond ETFs can be used for hedging interest rate risk, in particular:

The next table compares these funds’ characteristics:

PFIX RISR TBT TTT Inception 05/10/2021 09/30/2021 04/29/2008 03/27/2012 Expense Ratio 0.50% 1.04% 0.93% 0.95% AUM $202.39M $225.42M $274.70M $18.29M Avg Daily Volume $31.99M $2.06M $16.41M $566.93K Total Return* 103.24% 88.70% 90.49% 100.06% Annual Return* 15.45% 13.73% 13.94% 15.08% Drawdown* -36.17% -14.31% -33.83% -49.69% Sharpe ratio* 0.5 0.99 0.5 0.48 Volatility* 35.81% 10.12% 29.61% 44.51%

* Calculated with Portfolio123 from 05/17/2021 to 4/24/2026.

All of them have been effective at hedging interest rate risk, providing outsized returns while interest rates surged in 2022 and 2023. PFIX has the lowest expense ratio, largest dollar trading volumes, and highest total return since May 2021, but RISR leads by far in risk-adjusted performance (Sharpe ratio). RISR looks like the best long-term hedge, while PFIX is a more speculative instrument. In fact, almost 16% of PFIX’s assets under management change hands every day on average, pointing to popularity among short-term traders. TBT has the same Sharpe ratio as PFIX, with higher fees and lower volumes.

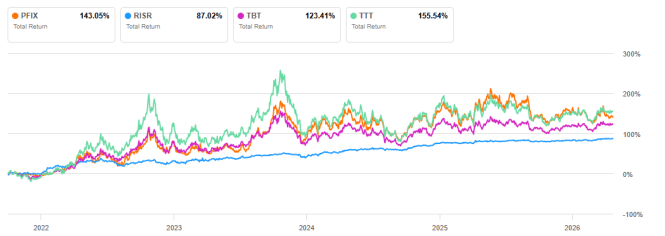

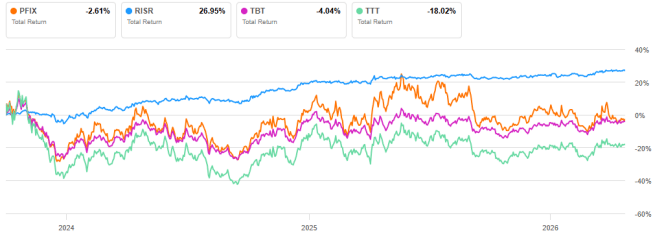

As plotted on the next chart, PFIX has greatly outperformed RISR in total return since the latter’s inception, with deep drawdowns and high volatility. RISR’s smoother path definitely looks best suited for long-term hedging.

PFIX vs competitors, from 10/1/2021 to 4/24/2026 (Seeking Alpha)

Additionally, unlike PFIX and TBT, RISR has continued its uptrend, although at a slower pace, since interest rates stopped rising. The chart below is more typical of a normal market, while the 2021-2023 period was exceptional for rates.

PFIX vs competitors, from 10/1/2023 to 4/24/2026 (Seeking Alpha)

In summary, PFIX may be better for trading and tactical allocation, while RISR is a safer long-term hedge. In fact, a hedging strategy blending RISR as core and PFIX as satellite would make sense.

Both have systemic risks: PFIX has the swaption’s counterparty risk of large banks, while RISR depends on overall solvency in the MBS market.

A number of ETFs have an embedded inflation hedge or are designed to hedge a portfolio against inflation. The best known are inflation-protected bond ETFs (VTIP, SCHP, TIP, STIP, etc.). They protect their own holdings, but their efficiency in hedging a larger income portfolio is limited.

All equity ETFs related to hard assets (in particular in real estate, metals & mining…) can profit from an inflationary environment. However, they are also strongly affected by sector-specific factors and are not recession-proof. The same thing goes for commodity ETFs, which additionally have a contango risk when they are based on futures.

Some equity ETFs are specifically designed for inflation: Horizon Kinetics Inflation Beneficiaries ETF (INFL), Fidelity Dividend ETF For Rising Rates (FDRR), and Fidelity Stocks for Inflation ETF (FCPI).

A few inflation-focused ETFs are multi-asset, such as the AXS Astoria Inflation Sensitive ETF (PPI) and the VanEck Inflation Allocation ETF (RAAX). Additionally, the Quadratic Interest Rate Volatility & Inflation Hedge ETF (IVOL) has an option strategy.

The Simplify Interest Rate Hedge ETF is designed for investors seeking to hedge a rate-sensitive portfolio of fixed income instruments and/or real estate equities. PFIX has been very effective since its inception in 2021, but with very high volatility. Compared to its competitor RISR, PFIX is a superior trading and tactical instrument, while RISR is a better long-term hedge, providing a smoother and more resilient uptrend. PFIX and RISR may be blended in a comprehensive hedging strategy.

This article answers these three main questions about PFIX:

Editor's note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF. Editor's note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。