Rasi Bhadramani/iStock via Getty Images

AI is certainly changing the investment landscape, and I'm increasingly bullish on its uses in financial research and white collar work more generally. There is a huge amount of interest in anything AI-related and the portfolio has been frustratingly devoid of any notable beneficiaries, and recent purchases have felt more like catching a falling knife with no end in sight. There is so much capital chasing the AI capex boom that it feels like otherwise strong companies are being sold to fund the grand ambitions of the AI supercycle. There is absolutely merit in what AI is doing, fundamentally changing how white collar work gets done. There is however a difference between the impact an innovation has on society and the durability of the earnings that flow to its market participants and suppliers. There is a long list of examples, but I'll just mention a few. The railroad boom of mid 1800's changed the US permanently by connecting the country coast-to-coast and creating a truly national market for goods to be traded within. That did not prevent nearly a century of capital destruction that was only arrested by significant consolidation and government regulation. The automobile in the early 1900's changed the world, creating a consumer economy and allowing consumers further freedom to travel and for supply chains to get even more granular. However, there were hundreds of car companies that eventually went bust or merged together (General Motors (GM) being the most prominent consolidator) and car companies today stil struggle to earn adequate returns on capital. The airplane was again revolutionary in the ability to move people and goods much faster than previously possible, but airlines and even airplane manufacturers have struggled to make adequate returns without significant government support over time. Finally, and most recently, the dotcom bust also witnessed significant fiber-optic buildouts, which were used and generated decent returns on capital. . .15 years after installation. The most challenging aspect of these capex booms is matching ultimate supply with demand. There is no doubt that many hundreds of millions, if not billions of people will eventually use AI to help with work and personal tasks. However it is challenging to know the capital intensity of the large language models that become most commonly commercialized. The large players are highly incentivized to to improve the quality and cost-effectiveness of their models, and the fast-moving nature of the latest models is challenging to square with 12+ month permitting processes to put actual shovels in the ground, and I have a hard time seeing supply and demand getting matched evenly at all points in time. Companies benefiting from the demand from AI are benefiting from both volume and pricing increases, as this buildout has probably been faster and larger than any capex boom in history. There are real bottlenecks emerging, and companies are taking advantage of pricing opportunities, which is great on the way up, but could prove to be very damaging to earnings if (when? ) supply catches up faster than participants expect. This is why it is seductive to think the market is cheap because the P/E is not that high, but it's important to understand that the "E" in P/E may be elevated/exaggerrated in CapEx booms like this one. It is challenging to stay disciplined in markets like this one, as oxygen flows in ways that may be short-term rational but long-term irrational.

Trim: ALNT, W, CELH

Sell: DAVA, HOV, DFH, GDDY, KOF

Add: TOITF, FSV, CDW, FND

I engaged in a lot of portfolio shaping during the quarter to shift capital from more fully-valued ideas to more attractive opportunities while also exiting investments whose fundamental outlook I no longer believed in. I trimmed Allient (ALNT) as a function of the stock running significantly from a purchase price below $20 in late 2024 to a price in the $50's. As the price has continued to run into the mid-$70's per share after quarter-end, I have continued to trim. I trimmed Wayfair (W) and Celsius Holdings (CELH) both on a valuation basis after significant returns in approximately one year. I still like these businesses and subsequent price declines after these trims makes them candidates for adding back to the position. I exited Endava (DAVA) during the quarter. As noted in my last letter, the position was among my most fluid. I have "seen the light" on AI, and I need to step back and re-assess this position for longer than a quarter. There are significant disruptions happening to this business and I have to acknowledge that my visibility into their prospects 2-3 years from now is very fuzzy.

I sold Hovnanian Enterprises (HOV) and Dream Finders Homes (DFH) during the quarter. While I like the direction HOV and DFH are headed in terms of asset-light homebuilding, the macro backdrop for these companies has only gotten worse in the last several months, and I prefer to assess these businesses for a better re-entry point from the sidelines.

I exited GoDaddy (GDDY), which was only a small position in a few accounts I've managed for a long time. The business is clearly being impacted by AI and the ability to generate websites very easily. It was a small position and I want to concentrate capital into my best ideas.

I sold Coca-Cola FEMSA (KOF) in the accounts where it was held to shift funds into its corporate cousin, FEMSA (FMX). I purchased FMX a little while ago with a plan to sell KOF in the income-oriented accounts where I owned it, but wanted to wait until after year-end to realize the capital gains. I still like FMX's exposure to Coca-Cola and I like the convenience store flywheel between new store growth and further Coca-Cola sales in Mexico.

I significantly added to Topicus. com (TOITF), which is now a top-10 holding. The company is a Constellation Software (CNSWF) spinoff, long considered one of the better M&A-based investments of all time. While I am very cognizant of the impacts that AI is having on software companies, and I could see some pressure on Topicus's business over time, I think Topicus' European exposure, which is historically sleepier and more balkanized, plus its commitment to M&A to lean in during this period of disruption, give me confidence in their path to value creation long-term.

I also added meaningfully to FirstService Corp (FSV). I have a great deal of respect for Jay Hennick, the largest shareholder and founder of FirstService. FirstService manages ~6% of the HOA/managed units in the US, and is the largest player in this space by a significant margin. There is a multi-decade consolidation opportunity in this market, and I believe Hennick's partnership-based compensation model for acquired businesses is unique and likely to drive outsized performance of the base and acquired businesses over a long arc of time. The company was historically valued as a high-flyer justified by mid-teens growth, and now the valuation is approximately 20x FCF. I think the current price offers a very good entry point for long-term mid-teens returns. I added to CDW Corp (CDW). CDW is the best-in-class value-added reseller of IT products, and recent product mix shifts towards more hardware (because of demand for AI) has driven margins lower and has highlighted potential for reduced software spend over time, where margins are much higher. CDW has a reputation for serving all sizes of customers as well as education and government customers, all constituencies which are slow to adopt new technology. I think at 11x FCF CDW is well-positioned to generate significant current return through a 2.5% dividend yield and significant share repurchases that could reduce shares outstanding by 20% in only a few years. CDW generally does not require significant capital to grow, so I think the assumption of meaningful capital return is relatively safe, assuming management does not engage in value-destroying acquisitions. Finally, I added to Floor & Decor (FND). FND is really interesting to me because it's been a stock market darling during COVID where it was assumed that they would get to their mature footprint of 500 stores (up from 270 at YE 2025) sooner than expected and achieve better store-level sales and profit margins sooner as well. Of course, the high home sales activity during COVID has receded significantly, many of the company's new stores appear ill-advised based on early sales results, and the achievability of the company's long-term sales and EBIT margins seem in doubt. I could not disagree more. The company still continues to take share from legacy flooring providers and while the Home Depots and Lowe's (LOW) of the world have made competitive responses in flooring, they will never come close to the breadth and selection FND provides. I think it's entirely possible the company generates $14B in sales a decade from now (up from $4.7B in 2025) and $1.4B net income (up from $209MM today). While the company has 108MM shares outstanding today, the company will begin to generate excess cash in the next few years, allowing for meaningful share repurchases, and while almost impossible to forecast avg. share prices over a decade, some reasonable math suggests shares outstanding could be ~85MM in a decade's time if all excess cash is used on share repurchases. It's not extremely difficult to see prices at multiples of today's prices in a few years time, and with a slightly better macro environment.

Bought: COF, POOL

Capital One Financial (COF) recently executed a transformative transaction, merging with Discover Financial Services (DFS). For those unfamiliar with the credit card industry, most credit card transaction have 4 parties (merchant, merchant's processor, credit card user, and the card user's bank), known as the open-loop model. American Express (AXP) and Discover historically were the only closed-loop credit card networks, which consolidates the merchant processor and card user's bank, thus a three party model. This enables additional quality to eliminate fraud, provide better benefits, and more. Capital One has historically been viewed as a subprime lender in credit cards and auto loans, but this transaction has the ability to structurally improve Capital One's historical margins as they transition away from Visa (V)/Mastercard (MA) and increasingly move to the legacy Discover network. Capital One has some work to do on the Discover network technologically and by improving acceptance (the % of merchants who accept the card), but I love the potential for fundamental margin improvement, which could lead to a valuation uplift over time. Starting from a 9x P/E multiple, and potentially a 8x multiple on 2027 margins vs. American Express at 17x, I am confident COF can perform very well over time.

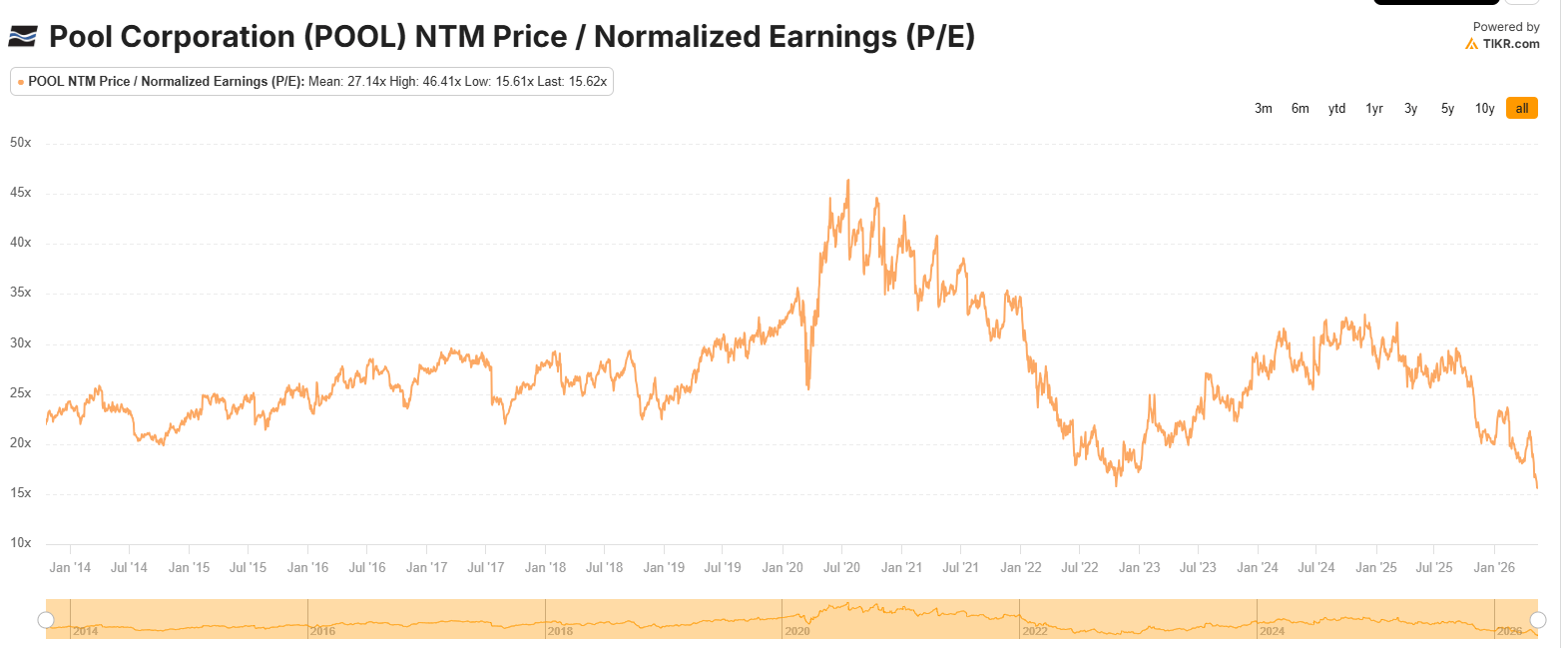

Pool Corporation (POOL) is the dominant wholesale distributor of swimming pool and related outdoor living products, with 35-40% market share and 456 branches nationwide; the next closest competitor has 8-10% share, but was recently acquired by Home Depot (HD) as part of the SRS Distribution transaction. The company has been in a long-term slump post-COVID due to the unwind of shortage-driven chlorine pricing and the surge in pool building during the pandemic. 60% of the company's sales are non-discretionary service-based purchases, and the company has historically generated ROICs in the 25-30% range, very strong relative to almost any physical product-based business. The company now sells for 15.5x forward earnings, which seems entirely too low for a high quality market leader with strong ROICs and normally mid-single digit organic growth and future consolidation optionality. The company is at all-time low valuations and based on the trend could be headed lower short-term. This suggests the external environment has changed in ways disadvantageous to POOL. The main risks here are 1) macro softness around continued pool construction headwinds, somewhat similar to FND's issues, and 2) the alleged aggressiveness of Heritage Pool Supply in being a formidable competitor to POOL with the support of Home Depot's capital. With Brad Jacob's launch of QXO (QXO), focused on building products distributors, as his latest iteration of an industry roll-up, after massive success in waste management (United Waste Systems), equipment rental (United Rental (URI)), and logistics (XPO (XPO)). I believe Home Depot has seen this new entrant, as well as the success of specialty retailers like FND, as shots across the bow, and is making aggressive competitive responses, purchasing SRS Distribution at almost the exact time QXO launched in mid-2024. Home Depot appears to be moving to build out its specialty distribution portfolio if for no other reason to defend its turf against QXO, and I believe the fear is this may have some downstream impact on POOL given Heritage Pool Supply is now owned by HD.

I am working hard, as hard as I have in some time given the opportunities I see, to make the right investment decisions for long-term success. Sometimes that may mean I'm out of step with the market, but I do recall many great investors being out of step in the late 1990's. While I'm open-minded to the possibility I'm missing generational wealth creation opportunities with AI, I remain concerned about becoming too aggressive or extrapolating current supply/demand conditions in the AI-affected market too far into the future. Best,Mike Loeb

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

此内容由惯性聚合(RSS阅读器)自动聚合整理,仅供阅读参考。 原文来自 — 版权归原作者所有。