Picture two families living four miles apart in the same mid-sized American city. Both earn about $85,000 a year. Both have two kids in elementary school. On paper, they are demographic twins.

The first family lives in a neighborhood where the zoned public school has mediocre ratings and a reputation that keeps most of their neighbors up at night. They send their two kids to a private school at roughly $7,800 per child. The mother works a second job on weekends to cover it. Ask her what she would cut if money got tight and she doesn’t even blink. Tuition is the last line she would touch. Private school, for her, is absolutely essential.

The second family earns the same income, lives in the same metro area, and has the same number of kids. Three years ago, they moved specifically because the suburb they targeted has one of the top-rated public-school districts in the state. Their kids walk to a public school that sends graduates to top universities every year. Ask this mother whether private school is essential and the question doesn’t even register. Private school, for her, is irrelevant.

Same line item. Same income. Same city. One household treats it as non-negotiable. The other doesn’t even think about it.

The Tomato-Tomahto of the Household Budget

This is the heart of what new PYMNTS Intelligence data shows.

What makes something feel non-negotiable is almost never about what it costs in absolute dollars. Essential isn’t a characteristic of the expense. It’s the characteristic of the person spending the money on it.

A PYMNTS Intelligence survey of more than 3,400 consumers put the same 22 line items in front of everyone and asked them to classify each one as absolutely essential, necessary but a choice or purely discretionary. The results don’t line up by income. They line up by life stage, family structure and the commitments each household has locked in over the years.

Take private school. It’s rated absolutely essential by 17%, necessary but a choice by 23%, and purely discretionary by 60%. Family financial support splits 26/34/40.

Then there’s grocery delivery. Half of consumers earning less than $50,000 say it’s essential or necessary, versus 42% of those earning $150,000 or more. For a household earning $45,000, getting groceries delivered might be a logistics requirement rather than a premium convenience if the consumer doesn’t own a car or works irregular hours or multiple jobs and can’t easily get to a store.

Compare all of that to insurance, rated essential by 65% of consumers with only 11% calling it discretionary.

Nobody really disagrees about insurance. The items where consumers are closer together than apart are universal, structural necessities. The items where consumers split are the ones where essential means whatever the specific household at the specific life stage decides it means.

Read More: The Three Blind Spots in How Consumer Sentiment Is Measured

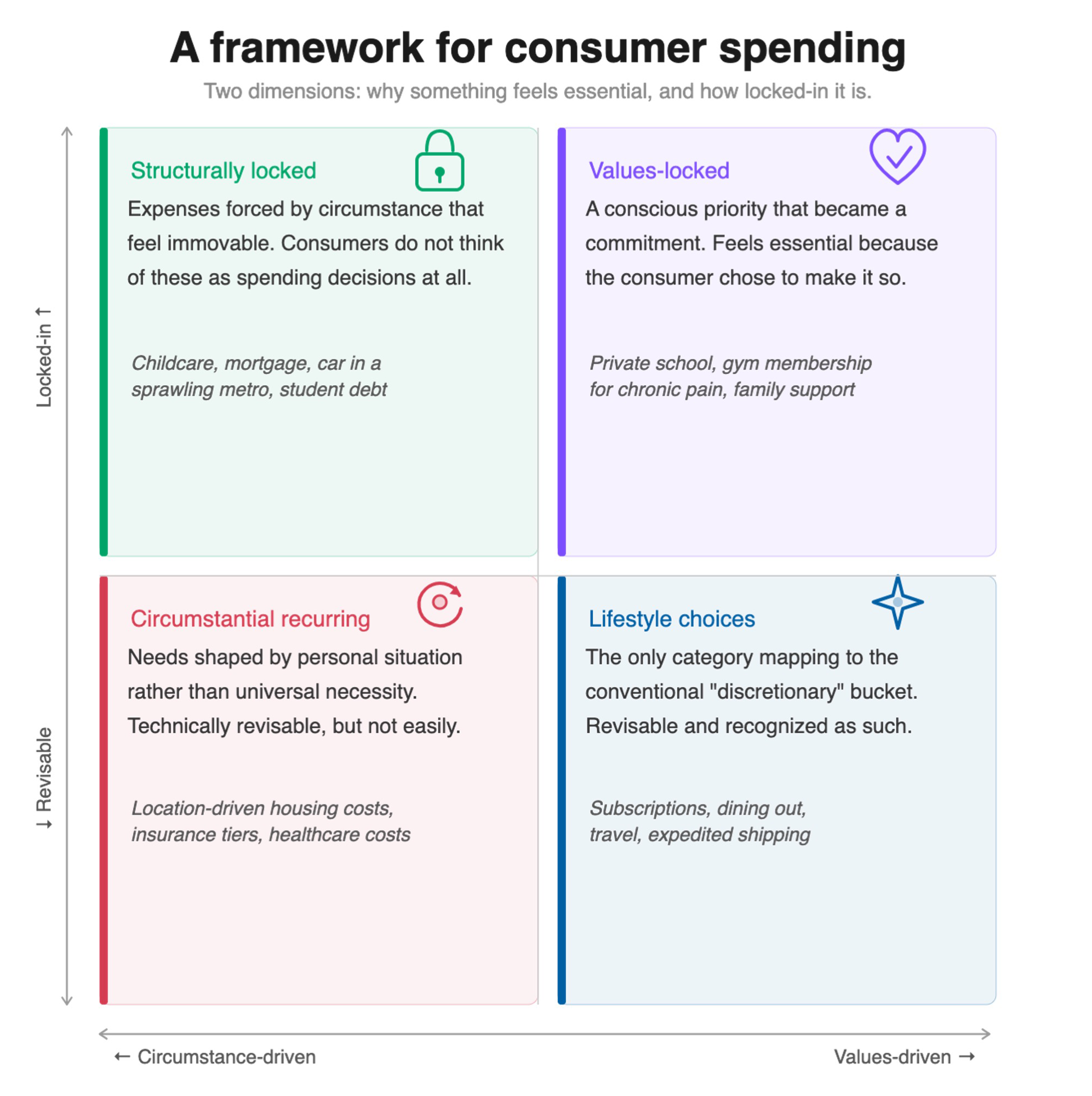

A Better Way to Think About Essential

Source: PYMNTS Intelligence framework, New Reality Check: The Paycheck-to-Paycheck Report, January 2026.

The traditional way finance professionals sort spending is into fixed, variable and discretionary buckets. The flaw with that classification is that it isn’t always correlated with how consumers manage their money.

A better frame has two dimensions:

- Why the expense feels essential

- How locked in it is

Structurally-Locked expenses are forced by circumstances that feel immovable. Childcare for a working parent. A mortgage. A car in a sprawling metro area. Student debt from a decision made a decade ago. PYMNTS Intelligence data finds that more than half (54%) of the full sample rates mortgage/housing absolutely essential, half rate car ownership essential, and 37% of married parents rate childcare essential.

Values-Locked expenses are conscious priorities that have hardened into a financial commitment. Private school tuition. A gym for pain management. Monthly support to an aging parent. The households rating these as essential aren’t wealthier than the ones that don’t. They’re different because of what they’ve decided matters, and is therefore essential.

Circumstantial Recurring expenses are related to needs shaped by a personal situation rather than universal necessity. They can be changed or eliminated, but not easily and not without other potential financial consequences. Accordingly, 65% of consumers rate insurance as essential and 58% of consumers rate healthcare as essential; these expenses dominate this quadrant and the overall rankings.

Lifestyle Choices are the only expenses that map cleanly to the conventional discretionary bucket. Subscriptions (14% of consumers say they’re essential), travel (13%), entertainment (10%) and expedited shipping (10%) are nice-to-haves but could be dialed back or eliminated, depending.

When expenses are put into this framework, the same items land in different buckets. A gym membership lives in Lifestyle Choices for one household and in Values-Locked for another. Childcare is Structurally-Locked for a 34-year-old working parent and irrelevant to a 68-year-old retiree. Essential becomes a subjective call, not an objective one.

How Life Stage Rewrites the Priority List

The clearest way to see the many sides of “essential” at work is to walk through the U.S. consumer base segment by segment. Each one tells a different story about what gets pulled into the non-negotiable tier and why.

Let’s start with millennials, the generation living through the years when earlier commitments show up as non-negotiable monthly line items. Nearly seven in ten, 69%, say they live paycheck to paycheck. Half point to long-term life decisions as the reason, a rate 19 points higher than boomers and the steepest of any generation.

Read More: 38% of Millennials Pay Out of Pocket for Healthcare

Their non-negotiable tier reads like a structural inventory. Insurance, healthcare, the car, the mortgage, outside family support. What sets millennials apart is the tier just below.

More than a third (37%) cite childcare as essential. Grocery delivery at 31%, because when both parents work and a toddler is in the car seat in the back, the friction associated with a trip to the grocery store gets real. Student loans at 27%. Where they live at 23%. None of those come across as lifestyle preferences. They’re commitments made years ago that can’t easily be unwound. That explains why only 54% of millennials feel in control of their financial situation even as they stay stuck inside it.

Married parents are the most obvious case of how Structural Lock-in operates. Sixty-seven percent live paycheck to paycheck. Sixty percent say they could change their situation with effort. Their budget says otherwise.

Married parents cite long-term life decisions as the reason for their financial situation at 59%, the highest rate of any household segment in the survey. Their top essentials look like everyone else’s: insurance, healthcare, mortgage. The difference shows up in the next tier.

Childcare and clothing at 37%. Grocery delivery at 30%. Private school at 29%, nearly double the 17% full-sample rate. Where they live at 25%. Every one of those categories runs at least eight points above the full sample, and none of them are stated preferences. They’re what it takes to run a household with kids. A second car to cover two drop-off routes. A neighborhood chosen for its middle school. Groceries delivered because nobody has time to shop on the way home. That’s why the married-parent budget is the most locked-in profile in this study.

Single parents show what happens when the same financial scaffolding has to stand on one income. More than eight in ten (82%) live paycheck to paycheck, the highest rate of any segment profiled. Only three in ten report any flexibility to cut. Clothing jumps to 40% essential, eleven points above the full sample, because a single income is feeding and clothing kids who outgrow their shoes every four months. Grocery delivery hits 34%, twelve points above the full sample. Family financial support, 39%. Private school, 28%. Childcare, 30%.

The most telling insight isn’t any single line item. It’s the pattern across the three reasons people give for their financial situation. Day-to-day spending, long-term decisions and unexpected events all rank within five points of each other. For most households, one of those three clearly dominates. For single parents, all three hit at once. There is no single lever to pull when things get tight because the budget is pressured from every direction.

The paycheck-to-paycheck struggling household closes the segment story in a way that looks paradoxical at first. Nearly half (48%) report little or no perceived control over their finances. Forty-three percent say spending changes alone can’t fix it. What drives their budget isn’t a pattern of everyday choices but shocks they didn’t plan for. Sixty-one percent point to unexpected events as the reason for their financial circumstances, compared with 31% of non-paycheck-to-paycheck consumers.

But here’s the counterintuitive part. Their essential ratings are lower across the board than other segments. Insurance at 55%. Healthcare at 50%. Mortgage at 46%. Car at 44%. This isn’t because they care less. It’s because they’ve already cut everything that could be cut. What remains is non-negotiable, and there’s nothing more left to trim.

Read More: How 30 Million Workers Borrow from Tomorrow to Pay for Today

Generation layers on top of all this. The sharpest divide between age groups isn’t on insurance or housing, where consensus about essentials is broad. It’s on the small daily line items that older generations treat as obviously discretionary.

Gen Z and millennials are up to ten times more likely than boomers to classify coffee, lunch out, food delivery, subscriptions and gym memberships as essential. For a 24-year-old with a two-hour commute, a food delivery subscription is about logistics and convenience. For a 72-year-old retiree with a fully stocked pantry, it’s an obvious waste. Neither is wrong. They’re describing different lives with different priorities.

Read More: Healthcare on Hold: Why 1 in 4 Gen Z Consumers Skip the Doctor

Parenthood is the single variable that reshapes the priority list more than any other. Married and single parents rate childcare, private school, family support, grocery delivery, food delivery, clothing and meal kits dramatically higher than adults without children. Childcare is obvious. The less obvious ones tell the real story. Meal kits, food delivery, grocery delivery. For parents, these aren’t indulgences. They’re how the household runs.

Read More: How Time Became the Next Great Asset Class

Grocery delivery sits at 22% essential in the full sample, 30% for married parents, 34% for single parents. Food delivery shows the same logic from a different angle. Thirty-four percent of households earning under $50,000 rate it essential or necessary, compared with 31% of households earning over $150,000. A worker juggling two hourly jobs treats the $12 delivery fee as the cost of eating the meal that has to happen between shifts. For a higher earner with a predictable schedule, the same line item is convenience.

The clearest signal in the entire dataset is clothing for single parents. Forty percent call it essential and another 46% call it necessary, putting 86% at or above necessary. Only 14% call clothing purely discretionary. For most consumers, clothing is lifestyle. For a single parent with growing children, it is regarded more like the utility bill.

Financial lifestyle adds a final twist to the picture. Nearly a quarter of paycheck-to-paycheck consumers (23%) earn $100,000 or more. Not because they spend carelessly, but because of commitments already locked in. The mortgage on a house in a good school district. Childcare for two kids. Student loans still running a decade after graduation. A six-figure salary doesn’t unwind any of that.

Read More: Who Is the Paycheck-to-Paycheck Consumer in America?

Consumers who aren’t paycheck to paycheck actually rate structural items like insurance, healthcare and mortgage as more essential than consumers who are struggling. You would expect the opposite. The reason shows up in what each group blames. Two-thirds (66%) of non paycheck-to-paycheck consumers point to day-to-day spending as the main driver of their financial situation. They frame it that way when the structural bills feel handled. For these households, their control levers live in the daily choices, not the locked-in commitments.

Struggling consumers tell a different story. They’re twice as likely as non-paycheck to paycheck consumers to cite unexpected events as the cause of their financial situation (61% versus 31%). Forty percent report low or no flexibility to cut expenses, compared with 18% of non-paycheck-to-paycheck consumers. That 22-point flexibility gap is the single widest in the dataset, and it is structural that becomes behavioral.

Read More: Meet the 27 Million Americans Who Drive 8% of Consumer Spend but Struggle to Pay Their Bills

Pulling It All Together

The picture that emerges across these segments is that essential is a characteristic of the person spending, not of the expense itself.

What actually predicts how a household will behave under financial pressure is the combination of life stage, family structure and financial history. Millennials cite long-term decisions at 50%. Married parents at 59%. Boomers at 31%. That 28-point spread between younger or parenting households and boomers is about which commitments are actively running through the budget. And how willing those households are to protect the priorities behind them.

Segmenting customers by income decile or FICO band captures none of that. Segmenting by priority profile captures all of it.

The Priority Behind the Payment

Every payments company, credit issuer and bank has built its data stack around two questions. What did the consumer buy, and how much did they spend? The PYMNTS Intelligence data in this report says those questions answer less than half of what matters.

What a consumer buys is visible in the transaction record. Why they bought it, whether it is a conscious priority or a forced one, and whether they would fight to protect it under financial pressure, isn’t.

The next competitive edge in payments and financial services isn’t more behavioral data. It’s priority data.

Consider two $7,800 annual tuition payments sitting in two different customer profiles. Same category, same frequency, same payment amount. In the transaction record, they’re indistinguishable. In reality, they’re three different customers. For the 17% of households that rate private school absolutely essential, that $7,800 is sacred. Those consumers will go into debt to protect it. For the 23% who call it necessary but a choice, it’s up for review the minute cash flow tightens. For the 60% who call it discretionary, and who happen to be paying the tuition because a grandmom is paying, it’s the first thing to go. Transaction data alone can’t tell them apart.

Read More: Why the Offers Economy Is Broken

Priority data gives a view of who the customer is, what they have committed to and what they will trade off to protect those commitments. It predicts the next move in a way the transaction record can’t. The implications play out differently for different parts of the ecosystem.

For credit issuers, priority data answers the single most valuable question in the business. If this consumer’s cash flow tightens, which bills get paid and which may not? Forty-three percent of paycheck-to-paycheck consumers who are struggling say spending changes alone cannot fix their situation. They’ll miss a payment on something.

Priority data tells the issuer which something.

Read More: Your Business Has Its Payments Data. Now What?

For merchants, the lesson is that product category isn’t destiny. The same subscription service splits 14% essential, 32% necessary, and 54% discretionary across the full sample, but 17% essential and 43% necessary among single parents. That’s one product and two completely different retention fights.

The Values-Locked customer will swallow a price increase. The Lifestyle Choice customer will cancel the moment a competitor runs a promotion. The same treatment for both leaks revenue at both ends. Dynamic pricing, loyalty programs and churn prevention all need to follow where the category sits in the customer’s priority stack, not the category code.

For Buy, Now Pay Later and installment lenders, priority data points to an opportunity much larger than discretionary retail. Thirty-seven percent of married parents call childcare absolutely essential. Twenty-nine percent call private school essential. Forty-one percent call family financial support essential. These are the recurring, high-ticket, Values-Locked line items that households currently put on credit cards, take from savings, or borrow from family to cover. Pay later products built for those priorities capture a segment the retail-focused BNPL players aren’t actively addressing. The underwriting case is stronger, too, because households don’t default on what they’ve decided matters most.

For banks and personal financial management tools, the implication is that sorting spending by category is a map drawn against how consumers actually think. A single parent’s clothing spend isn’t lifestyle. A millennial’s food delivery isn’t dining out when it functions as a logistics and convenience tool for a working household. A gym membership isn’t fitness when the user joined for chronic pain.

Money management tools that let consumers tag their own priorities, or that infer priorities from which categories survive the next income shock, stop being transactional logs and start being the household’s priority dashboard. That’s a stickier relationship, and one of the few defensible positions left as transaction-data parity among competitors continues to erode.

Read More: The Next Battle in Credit Won’t Be for Top of Wallet

Across all of those use cases, the strategic insight is the same. The successful payments, credit and banking players over the next decade won’t always be the ones with more transaction data. They’ll be the ones who know who their customer is underneath the transaction.

Two consumers with identical demographics and identical purchase histories can have radically different priorities, and those priorities decide how they behave under pressure.

The question everyone should be asking is whether their data strategy reflects that. Or whether it is still bucketing customers simply by what they bought last month.

Until NEXT time.

Join the 21,000 subscribers who’ve already said yes to what’s NEXT.